Update: Flip Flopping but Still Cautious

I couldn’t stay out of the IMO 2020 trade for very long. I said last week that I sold out of my tankers and refiners (other than Vertex Energy – more on that in a minute) but that lasted a whole of 3 days before I was sucked back in.

On Thursday, after news came out that Robert Bugbee of Scorpio Tankers had made a huge option bet on the company, my fear-of-missing-out (FOMO) kicked in and I piled back in. I missed the bottom with my panic, but you can’t win them all.

This time I am more circumspect about my shipping and refining bets. I have kept my positions in Ardmore and Scorpio relatively small. I have similar small positions in PBF Energy and Valero. While I am holding DHT Holdings and Diamond S Shipping on the crude tanker side, I am not at all convinced that a move up in the crude tankers will prove to be sustainable.

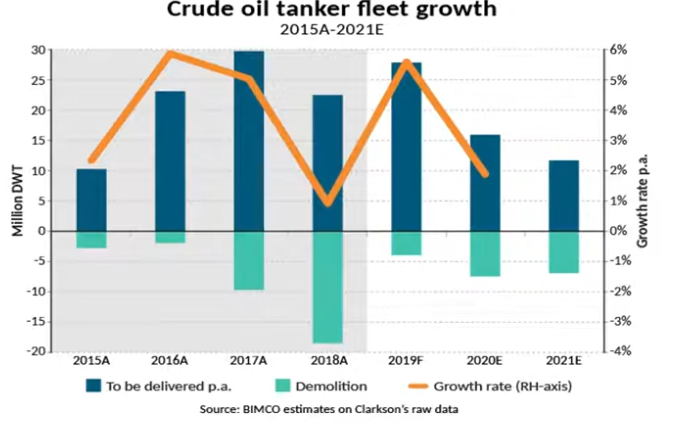

There was a good update put out from Bimco (h/t @Fbuschek for sharing it with me). They are not all that bullish on any of the shipping sectors, but are particularly sanguine about the crude tankers.

BIMCO points out that fleet growth in VLCCs has been significant this year and that this is likely to keep rates down next year.

It was uncomfortable to learn that new VLCC’s (so the largest crude oil tankers) were even being used to ship crude products during the summer months. This means that A. the VLCCs had no where else to go and B. they were crowding out the product tankers for their own commodity.

No wonder product tanker rates were so low!

At one point over the weekend I was about to turn an about-face and sell-out of the tankers again. But I have thought better of it – for now.

First, crude tanker rates are showing signs of strength. Today VLCC rates spiked above $60,000 on Monday, so no more will they be trying to take share from the product tankers.

Second, the second half of the fourth quarter is always strong for tanker rates. My expectation is that tankers will rally like they usually do in the fourth quarter because its the fourth quarter if for no other reason.

This seasonal move should be exaggerated this year by A. scrubber retrofits taking tankers off the market and B. a shortened refinery maintenance season.

The strength of that rally may get confused or misinterpreted as a secular move brought on by IMO 2020. Who knows, maybe it will actually be a secular move. Its not impossible, but I’m not planning to bet on that. Whether it is or is not, I think the point where these names pop will be the optimal time to sell.

Vertex Energy

I mentioned that even as I have hemmed and hawed over what to do about tankers and refiners, I have stayed steadfast in my holding of Vertex Energy.

This is because the one aspect of IMO 2020 that I have some confidence in is that high sulphur fuel oil (HSFO) prices are going to fall.

The CME Futures are saying as much. This screen capture was taken last Thursday when the September contract was still trading. The backwardation in HSFO between September and January was close to $18/bbl!

Since that time January HSFO futures have slid further. They closed yesterday at a hair above $30 per bbl.

Vertex makes their money on the spread between HSFO – which is what their used-motor-oil feedstock is priced off – and the products they sell, which are a combination of base oils and low-sulphur fuel oils.

The company commonly uses Gulf coast Unl 87 Gasoline as a benchmark for their fuel oil pricing.

With that in mind consider the following:

- In the second quarter the average Gulf coast Unl benchmark was $78.86 per bbl. The average benchmark HSFO was $61.15 per bbl. Thus, the spread was $17.50 per bbl.

- Looking forward to the January 2020 spread, based on last Thursday’s numbers the difference between Gulf coast Unl and HSFO was $34.51 per bbl ($67.24 per bbl -$32.73 per bbl)

Looking forward to next year Vertex should have double (or more) the margins they had in the second quarter of this year. As best I can tell, those margins are at least $10 per bbl better than even their best quarter in the past.

Meanwhile the company has restructured itself with the recent partnership announcement with Tensile Capital. Assuming a successful pilot program is completed by year-end, Vertex will have removed its debt from the balance sheet and secured the capital for future growth.

But nobody cares. Maybe I’m missing something – but I don’t know what.

The Swine Flu Crisis Intensifies

The best follow for the swine flu epidemic has been @winsteadscap on Twitter. He/she has been providing excellent information on the expanding crisis that is unfolding. This morning, they put the following out:

I have gotten longer of BRF SA and am tempted to do the same with Seaboard Corp. It seems like the news just keeps getting worse for pork consumers.

Sells

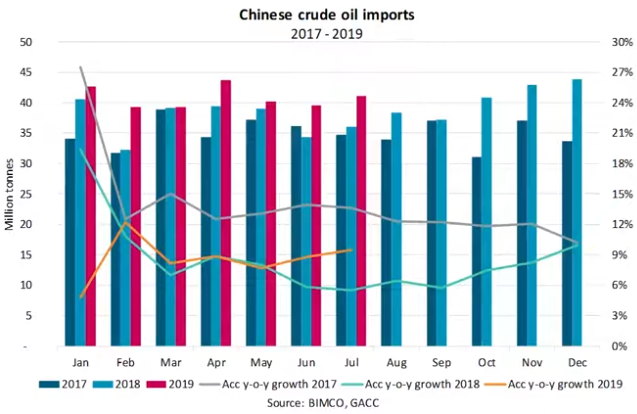

I sold out of my Canadian oil stocks yesterday. It looks like I was wrong about Saudi Arabia having trouble getting oil back online. Either that or they have done a better than expected job of fooling the market through disinformation and inventory management.

Whatever the case, it does not appear that the oil market is undersupplied right now. In fact, this chart from BIMCO spooked me a bit.

Chinese crude imports this year have been especially strong. This even as the Chinese economy has, by all accounts, been relatively weak. What gives?

It makes me wonder if the bears are onto something – that we truly are awash in oil still. While the summer has been good for draws in the United States and builds so far have been modest (ex-hurricanes), maybe there is too much oil and it is just going elsewhere.

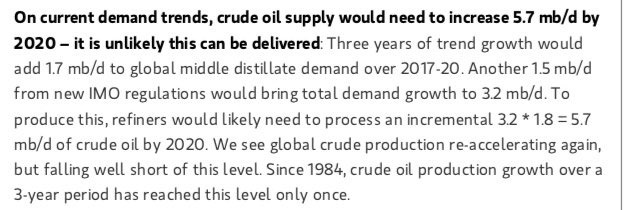

The only thing that really gives me pause with oil right now is what IMO 2020 does for demand. I was reminded this week that incremental distillate demand from ships switching to low-sulphur fuel could mean a big increase in oil demand.

If that comes to pass then oil is going higher.

It is still what I said a couple weeks ago – clear as mud. But given that this is the case, I need to at least step back and think this through with a clear head. I exited, I’ll step back, re-evaluate, maybe get back in. I would rather not lose money in this environment and miss out on making it.

Slowdown

Overall, I’m still positioned very cautiously. In addition to the oil positions I sold yesterday I also sold out of my small position in CUI Global (which was unfortunately timed to be just before today’s positive news release) and HyreCar (which was, sigh, unfortunately timed to be just before today’s pop).

I reduced a couple of my gold stocks a little yesterday, just in case I am wrong and this is not just a normal correction. But I also increased my position in Wesdome, which had a very good resource report for their Kiena Mine Complex last week and which I think is a good deal under $6 per share. So overall in gold I think I am about flat on positioning size.

My caution on the overall market is twofold. I still wonder about dollar liquidity, which seems to have taken a back seat for the moment. But in its place, we are seeing some pretty rough looking economic numbers.

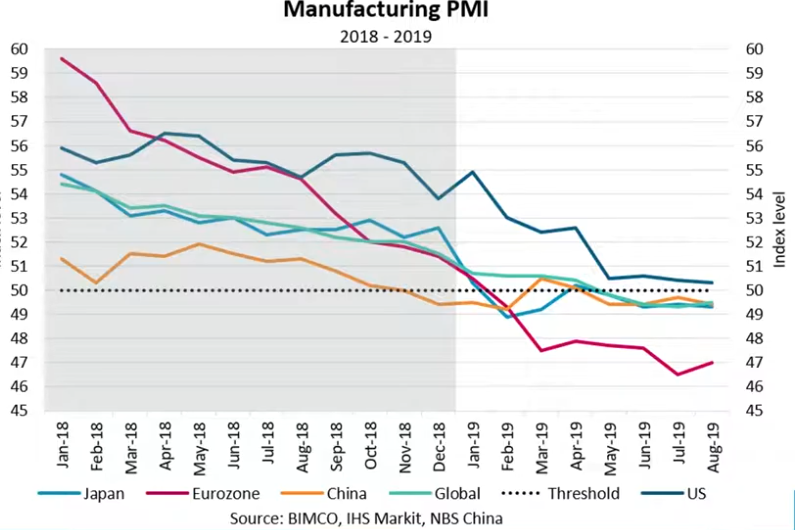

Below are a number of key manufacturing PMI’s heading into September. The weakness is evident.

These numbers have been followed up by further weakness in September. A few days ago September data from China showed a still weak number, the German manufacturing PMI was characterized by some as being in “free-fall”, and there was a weak PMI in the United States.

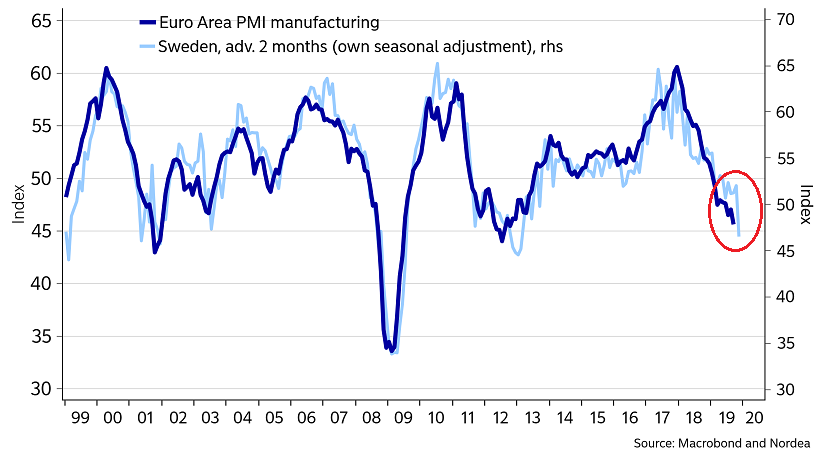

The weak number in the US that came out today overshadowed another number from Sweden. Their PMI plunged below 50.

Sweden is apparently a useful canary. I’ve read that Sweden is one of the most export-oriented economies, it is extremely open to trade flows, and therefore when Sweden starts to go south it is usually indicative of trade slowing.

So overall, I am cautious, with large positions in reverse index ETFs and also some shorts in individual names. I decided to go short on a couple of Canadian cannabis names last week as I came across numbers on (over) capacity that seemed a disaster in the making. I have also been short a few of the high-flying SaaS names that have begun to sputter, a couple of solar names, a couple of biotechs and a couple of US shale producers. These are all very small positions, and my main hedges are the inverse ETFs, which let me sleep soundly while I wait to see if my long positions play out as I expect.