I bought it, but I didn’t believe it

Jimmy cracked corn and I don’t care

It is a Constanza market. Everything you might want to do – do the opposite.

If you think a stock is overvalued – buy it.

If you think it might go bust (or already has) – go all in long.

If something looks overbought – it’s not. If it looks oversold, it’s not.

But most of all – remember the #1 rule of fight club – every event is good for SaaS.

I’m kidding of course. Kind of. In a market like this there is just no point in looking too hard at companies. Analysis is out the window. You just shoot first on both ends of the trade and don’t think to much about the long-term.

To take but one example: what is the point of a deep dive into Air Canada’s social distanced load factors and where their breakeven profitability might be? All you needed to know was that the company raised cash and wasn’t going bankrupt. And then after that 30% move in a week, that the market was getting pretty extended. None of this has anything to do with the business.

I could go on with other examples of silliness. But that is the past because I am off that train.

I played it as best as I could, but it had to end – for me at least. We might be at that point more generally – I see the indexes are down again today but clawing back up so who really knows. But last Thursday was the end of the speculation for me.

I started selling some things as early as a couple of weeks ago but I still got caught by Thursday’s sell-off. It wasn’t too painful, but it was the omen I needed – I had made myself a deal – when we get our first big correction, I’ll step away again.

My earlier sells were my earliest purchases – the mortgage names, some gold names and some one-off plays that have moved significantly (like DLH Holdings and Sonoma Pharmaceuticals – which was a bit of a fluke).

But I did a bit of buying too and it more than offset the sales: a few small regional banks – Bank7 Corp, Sound Financial and Parke Bancorp. A few new names like Digital Turbine, Intellicheck, CRH Medical, Protech Home Medical and a very small position in Intermap. Increased position sizes in existing positions like Rada and Schmitt. And the biotech basket I mentioned in the previous post (which I have since re-formed into positions in Dare, Eiger, Enlivex and Obseva). Most speculatively, I had taken on some “economy” names – like Air Canada and American Axle.

My net exposure was going up. I was monitoring that exposure but with the market rising I was allowing it to stay a bit elevated. I should have known I was getting a little too offside when I had a big up day (for me) last Tuesday – more than 1%.

Of course, this was followed by the opposite on Thursday, to the downside this time – 2%.

That may not sound too bad, after all the market was down 5%, but I’ve really tried to create a portfolio that doesn’t go up or down more than 1% on any day no matter what the market does.

So last week was a wake-up call that I had strayed from that. I was compelled to correct that imbalance. I sold the longs I was least comfortable with (which was anything economically sensitive), reduced some others to lower weights, and most importantly, added to my index hedges.

I’m not short now, but I’m (hopefully at least) not too far net long any more. My basic objective remains the same as what I articulared in February – I want to do well when my individual names do well (like when Schmitt buys an ice cream business for a million bucks) and not get creamed (pun-intended) if the market does.

Looking back

What strikes me most about the last few months is how closely they mirrored the 2008 playbook. The big difference this time around was that about 2 to 3 years worth of rotations were fast forwarded into the last 3 months.

First you had the golds move, right at the bottom of the market. Then you had the growth names. Then the mortgage names. Then the banks and value.

It was interesting to me how it was basically the same song all over, only performed by the chipmunks.

But now? I’m not so sure.

Other than from perma-bears, I don’t see too many predicting a second wave, or even thinking about what a second wave actually is. Instead all I see are justifications for the rise in cases. Mostly, that it is just testing.

Okay. That could be. I know from our experience in Alberta that this logic was on display in early April: its just testing…we don’t have to worry… the numbers lie. I said it myself.

Then we found out there were two super-spreader events and that the testing explanation was a red herring. It was bullshit. The real indicator was that percent positives were 3-4%. In states with so-called elevated testing we are rarely even down to that level from what I can see.

So I am skeptical of this hypothesis. I’m also not sure whether the same can be said for what is going on globally.

I also see a lot of finger pointing to data that is improving. I don’t find that argument all that compelling either – not with the market at 3,000+. If it is the economy that the market is going to rise on – what matters from here would be the last 5%, and there is no indication yet of when we get that back.

The most compelling argument to me by far is that you simply do not fight the Fed. Or in this instance, every central bank in the world.

I think it is best to be honest: this is really the single leg of the bull case from here. Its not really about earnings or economic growth or green shoots or things getting better faster than some bogus projection that no one really could have guessed at any way. Its just about liquidity – and how maybe we have triggered a massive bubble in stocks where higher prices beget higher prices regardless of what the economy does.

Don’t get me wrong, I’m not saying this derisively. I am 100% onboard with this possibility. I don’t think anyone really knows how high a market can go on liquidity alone, and the possibility exists that the answer is much higher.

But I think you gotta be honest and admit that this is the single reason, albeit a very big reason, to bet on the upside. That’s the bet.

Meanwhile, I am uncomfortable with all the speculation I see. Every time we see some guy like this barstool dude become an investing guru overnight, you gotta raise an eyebrow. When have we ever seen something like that and looked back in 2 years and said, yup that was the start of a real run? Or when have we seen the start of a bull market coincide with the rise of retail investor speculation, or with crazy moves in stocks in bankruptcy that have no business going up?

So even as I realize that this is possibly the exception to the rule, possibly the next 1999 (which I don’t think you can brush off – this could be the next 1999 given the liquidity), it seems more likely that this is evidence of excesses that needs to be worked off first. I am choosing to be cautious, for now at least.

Anyway, like I’ve written a few times, I don’t have to be right. I just have to be not wrong. To see my portfolio continue to creep up slowly in fits and starts. And by balancing back out my exposure I should be able to do that.

Onto some specifics

First, the other big thing I am still waffling about – gold.

I’m really unsure about gold. The employment report a couple of Friday’s ago gave me a big pause. As did the rise in the stock market.

But at the same time, I am reluctant to cut my exposure too much. The central bank positioning is ideal for gold right now. It seems likely further stimulus will be passed. It seems possible that rates go even more negative.

What’s more, the movement of gold since the employment report has been surprising to me. Honestly, when I saw that number I thought it was done for gold. It seemed like a disaster. And on that Friday, it was.

But since then, well I have to admit – it hasn’t cracked. It keeps getting whacked, like it did today, but each time it gets whacked it comes back. And each whack is a little less exuberant then the last one. So I don’t know…

That unemployment report should have been a knock-out blow that sent gold reeling. It should have been months to recover. Yet here we are. Still above $1,700.

As well, the gold stocks, the one’s that I own at least, seem to be very reasonably priced.

Roxgold trades at 3.5x trailing EBITDA, Gran Colombia trades under 2x trailing EBITDA, Teranga Gold (which I recently added) trades at under 4x next years EBITDA once the acquisition is integrated, Wesdome is more expensive, at 12x EBITDA, but will look much cheaper once Kiena gets into production. And yes I know, EBITDA is not the right metric to sue, but its right there on my screen whereas I’d have to dig into each name to get cash flow, so this is what you get.

Similarly, the bucket of developers I own are barely higher than they were pre-pandemic.

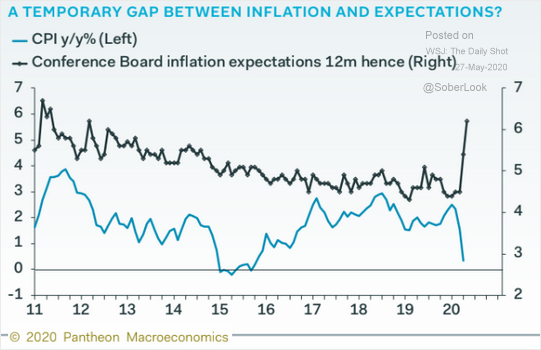

It is also interesting that inflation expectations have spiked.

Hugh Hendry

Two of the most influential interviews for me over the last couple of months involved Hugh Hendry. Both were on RealVision.

RealVision gets a lot of hate and I think it is misplaced. I get a lot out of it. Their interview with Emad Mostaque, which I watched during the first week of February, was a game-changer for me – Mostaque outlined a very coherent view of what was likely to happen with the coronavirus. That interview alone saved and made me way more money than I will ever pay in subscription fees. I feel like investors like to rail on the service because they or their guests are often “wrong”. Who cares. You subscribe for divergent views and you make your own decision. Its not about trying to find someone to tell you what to do.

Anyway, back to Hendry. I didn’t really know much about the guy, and I still don’t, but he said some stuff that really resonated with me.

In the first interview, he was interviewed by Raoul Pal. In the second, Hendry interviewed the author of the Princes of the Yen author Richard Werner. The Princes of the Yen interview was particularly insightful. It gave Werner’s views on the workings of central banks, and many of the insights were things that I hadn’t considered before.

But I’ll keep the talk to Hendry for now. Hendry thinks this environment is likely good for gold – but that gold, as I am so painfully aware, will do everything in its power to buck you off before going to its rightful place.

And Hendry makes another very good point – that you may want to be long gold here, but don’t believe in it.

The idea is this. Gold doesn’t just go up just because of money printing. It goes up because of the belief that money printing will lead to inflation.

For example, gold tanked in 2012-2013 when investors started to clue-in that all the money printing was not leading to an increase in the velocity of money. There was no transmission to the economy.

This time around? Well, Hendry is again skeptical that there will be transmission. Count me in on that.

But in the short-term, that likely “truth” is irrelevant. What matters is whether investors think there will be transmission. They have so far, and most likely will continue to. So gold should go up on that expectation.

You can act on that, but you don’t want to believe it. Hold through the rally, but don’t trust that it will last. Because the better probability is that money velocity won’t pick up and gold will eventually tumble back down.

Hendry also seems to be cautiously uber-bullish on equities. If that sounds like a paradox, it probably is, but that is where we are at right now. His perspective, again like what I’ve been thinking, is that the middle of the road is not very likely right now.

I get the impression that Hendry would not be surprised to see 4,000 or 2,000 on the S&P – and maybe both. That’s basically how I feel. Things are that messed up right now.

He’s not the only one. @Volslinger, who is a fintwit follow I always look for (though I wish he said a bit more) summed it up well on Friday.

My take is this: I don’t feel like this is a good time to pretend you know what is going to happen. You may end up a hero, but you also may end up getting punched in the face.

It is anything goes time. Maybe if your goal is seeking publicity for your barstool media business its the perfect time to be all in one way or another. But if you are actually managing money for your family and your future prosperity depends on these decisions – well, I don’t think that this is the right time to be taking a big risk.

Anyway, the bottom line on all of this is that I am back to hedged. I’m not net-short like I was in February (After all, the Fed), but my portfolio should not go down much if the market continues to swoon. In fact, if at the same time the Canadian dollar falls back down down after this ridiculous rally (which my god, it has to, right?), I suspect I could go up a bit. I took off all my CAD hedges last week.

Today when the market fell 2% at the open, I was flat, even with gold down $25. That’s what I like to see.

I think I will leave it at that for now. I was going to talk about individual stocks in this post, in particular Schmitt, but this is getting long so I will write something separate up later this week.

Hey Sigurd, a long time reader and big fan of your blog

Im curious if you have had a chance to look at Mako Mining before? (MKO.V) This is a name that my trusted friend has been harping on for a while. Would love to know your thoughts on the name

Druckenmiller has always said that liquidity trumps earnings and so I think that’s really the name of the game here.

I recently read a book recommended by @SqueezeMetrics on Twitter and it gave me a new perspective on how to think about the modern markets.

I think you should take a look, maybe everything we thought we knew about the market is wrong, just maybe

Lately I noticed a few brokers pushing out “fractional share” offering supposedly for people with limited money to buy stocks. I have a suspicion that we are only in the very early innings of a stock bubble

I’ll take a look. Like I said in my post i think its quite possible liquidity does trump economics so are you saying that book says the opposite?

Oh no I think the book lays out a pretty good case why liquidity is the main driver of the market

Never mind my previous comment – i read the summary of the book, I understand what you’re saying now. I’ll read it.

I find Ray Dalio instructive when it comes to Macro (not predictions though, just to get a fundamental understanding). His argument is that money printing did not cause inflation because the money supply went down as bad debt was written off and households delevered after 2008. Plus banks beefed up their reserves. So the printing merely prevented a deflationary spiral.

This time though, household debt to GDP in the US is at around 2003-2004 levels? Most banks are better capitalized than ever, and on top of that the government is injecting trillions directly into the economy. And we are not dealing with an event where the economy has to return to a new lower normal like after 2008 (as some sort of cure of the virus will probably be available relatively soon). There is not a huge hole in the money supply that has to be filled up this time around.

I wouldn’t know about timing though. Every single major pandemic has had a second wave so far. And mask wearing is not going into style soon probably. So a second wave in winter does seem likely as immunity % is still <10% in most places. So significant inflation might only show up in 2021 or 22.