Schmitt Buys an Ice Cream Shop

Schmitt was one of the companies that I was comfortable adding to during the pandemic induced sell-off in March.

At its lows, the stock traded into the $2.40s. I added mostly in the $2.50s and got some at close to the lows as well. I added fairly significantly, for me at least, increasing my position by about one-third.

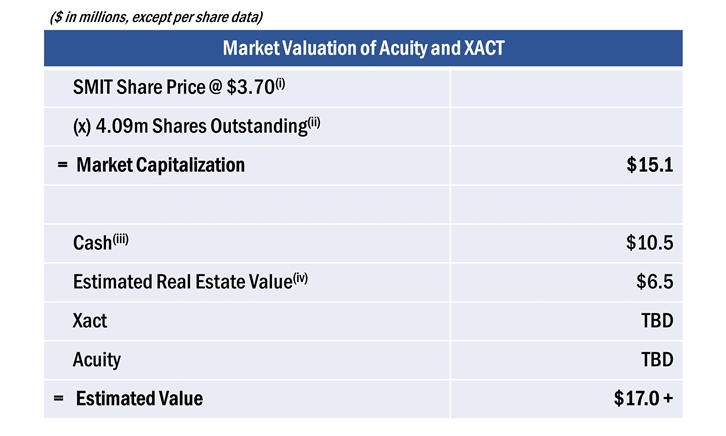

The reason I was so willing to add, even though I wasn’t a very aggressive buyer of stocks at the bottom of the market in general (I never seem to be good at this) is because at that price Schmitt was trading at ~20% below its net cash position.

This gave me some confidence that I wasn’t going to lose my shirt.

When you added to that the value of the company’s Portland real estate, which Schmitt valued at $6.5 million at the annual meeting last year, and the value of the two remaining businesses (Xact and Acuity), it seemed like one of the safer bets out there.

At the time the stock was falling Schmitt was exploring a shareholder opportunity that kept them from buying back stock. Without the company’s support of its shares the general illiquidity of the market (not to mention the upcoming delisting of shares) there was plenty of room for the stock to fall on fear of the unknown.

I was hopeful that the shareholder opportunity would be a game-changer for the company. I have some confidence in the decision making of Michael Zapata and his team. So, I crossed my fingers for some sort of accretive use of their $10+ million cash balance.

Unfortunately that didn’t happen. We never even found out what the opportunity was.

Schmitt announced at the beginning of June that they had ceased discussions on the opportunity. They also announced a Dutch auction giving shareholders the ability to sell their shares back to the company at between $3-$3.25, depending on demand.

I have to admit that I was considering participating in the Dutch auction. Not to sell my entire position, but I toyed with the idea of selling a few shares at a price was a nice, quick return.

But then, on June 11th, Schmitt announced that they had been the successful bankruptcy bidder for the assets of Ample Hills Holdings.

Talk about out of left field. It has taken me a while to wrap my head around this deal. It is a total change in the thesis. But I’m actually really liking the move, though I recognize the risks have went up a notch or two.

Ample Hills Holdings

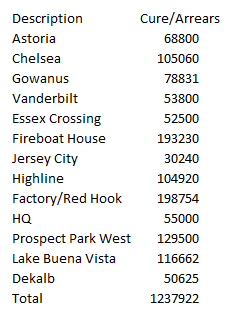

The first thing to understand is what Schmitt is paying for Ample Hills. The bid they made was $1 million dollars. In addition they are assuming the cure amounts associated with the assets. According to Schmitt’s 8-K they have to assume at least 7 of the 10 active leases. They may assume all 10.

So what are the cure amounts? Well, there are more than 10 leases listed in the bankruptcy documents, all listed below. I believe that the last 3 in the list below wouldn’t be part of the 10. Prospect Park West and Dekalb are not yet open. The Lake Buena Vista location is on Disney’s boardwalk, which I don’t believe they operate it themselves – they just supply ice cream to it (though I don’t really understand why it is mentioned then?). Finally, Factory/Red Hook and HQ are all considered one location I think. The cure amounts for all the leases are:

If Schmitt assumed all 10 remaining lease locations including the headquarters, that would be total cure amounts of ~$925,000.

Add it up and Schmitt is taking Ample Hills Creamery for about $2 million.

Now I’ve read/skimmed through every single one of the bankruptcy filings (ie. I’ve read through all the one’s that are relevant and not just reiterating an objection, listing creditors or introducing a lawyer).

My conclusion is – $2 million bucks doesn’t seem like a lot for this business.

The first thing is, Ample Hills is not just your regular local ice cream shop. This is not just some no-name local mom and pop shop.

This is a real brand – with notoriety and a following.

Consider these comments from the bankruptcy filings:

From their Instagram account:

I have a friend whose company has built an app that, among other things, analyzes, compares, and ranks the footprints of businesses on social media. Before either of us knew about the celebrity of the company, he screened it on his app. He was scratching his head why this dinky little ice cream shop was punching so far above its weight on the social media scale. Clearly, now we know.

Honestly, there are a lot of things to worry about with this business acquisition, and I will get to them all, but my over-arching thought is this – how can the Ample Hills brand be worth only a couple million bucks?

The Ample Hills History

The history of what happened to the Ample Hills business is described in this declaration by Brian Smith.

It is worth reading in full. These are the Coles notes.

Smith and his wife Jackie Cuscuna founded Ample Hills in 2010. They sold ice cream out of a cart. They opened a shop in Prospect Park (Brooklyn) in 2011. In 2012 they opened another, in 2013 another. All in Brooklyn.

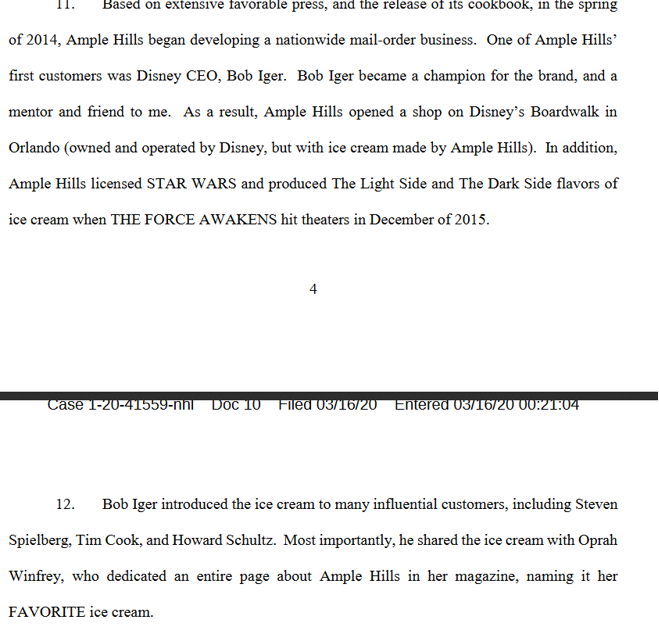

In 2014 they started a nation-wide mail order ice cream business. Bob Iger became a customer and liked the ice cream so much that he made a deal to open a shop on Disney’s boardwalk.

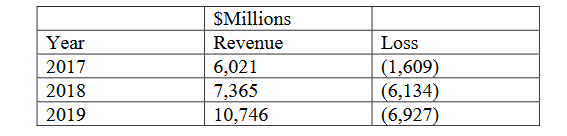

They expanded even more quickly – raising $4 million in 2015 and taking out an SBA loan at Flushing bank. They added more locations and – here is where it all went wrong – they built a factory (called the Factory) in Brooklyn in 2017.

The Factory was a cash incinerator. It cost $6.7 million to build – $2.7 million more than it was supposed to. It took 18 months longer to build than it was supposed to. It was supposed to run at full capacity, supporting the wholesale business and new shops, but the shop openings were delayed.

The Factory ran at an annual rate of 200,000 gallons last year versus a capacity of 500,000 gallons. In the filings Ample Hills says the Factory has resulted in dis-economies of scale.

According to the filings, Ample Hills “began to lose money as they started construction of the Factory”. Here are how those losses evolved beginning in 2017:

But at the same time, at the store level, Ample Hills was actually doing quite well. In 2019 “on average” the shops generated 15% EBITDA margins. The combined entity loss of $6.9 million was a result of “depreciation, amortization, interest expense, payroll and other operating costs associated with supporting the Factory” (my underline).

What Schmitt is Buying

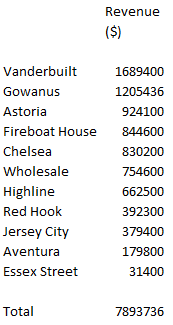

So the short answer is – we don’t know for sure. My guess is that Schmitt will take on the leases of the most profitable stores. Here are the revenue figures for the remaining 10 leases from last year:

The Essex Crossing location was only open for a short time in 2019. It looks like a promising location (it’s a farmers market in the Lower-East Side) and they did $55,000 of revenue in the first two months of 2020.

Schmitt appears to be trying to negotiate leases for some of these stores. After the auction there have been 3 objections, from the Chelsea, Esses and Astoria lease holders, complaining that Schmitt has engaged them to try to sign a new lease rather than just paying the cure costs and taking on the existing lease (it looks like these objections were overruled).

So there is a lot of uncertainty about which leases Schmitt ends up with. Assuming Schmitt ends up taking the top-7 revenue leases and Essex Street, they probably are looking at $8 million in revenue annually.

Ample Hills did about 7% of its revenue from wholesale and another 3% from e-commerce last year – so there is another $1 million all-in from this side of the business.

That is $9 million dollars of revenue from the existing locations.

But will it be profitable?

One problem, and maybe a reason that Schmitt was the only bidder, is that Ample Hills doesn’t appear to have provided corporate financial statements from the last few years.

I don’t have a lot of experience with bankruptcies, but I kinda thought this would be a requirement. But I have gone through every document and unless I fell asleep skimming through (which is possible), I don’t think last years financials are there.

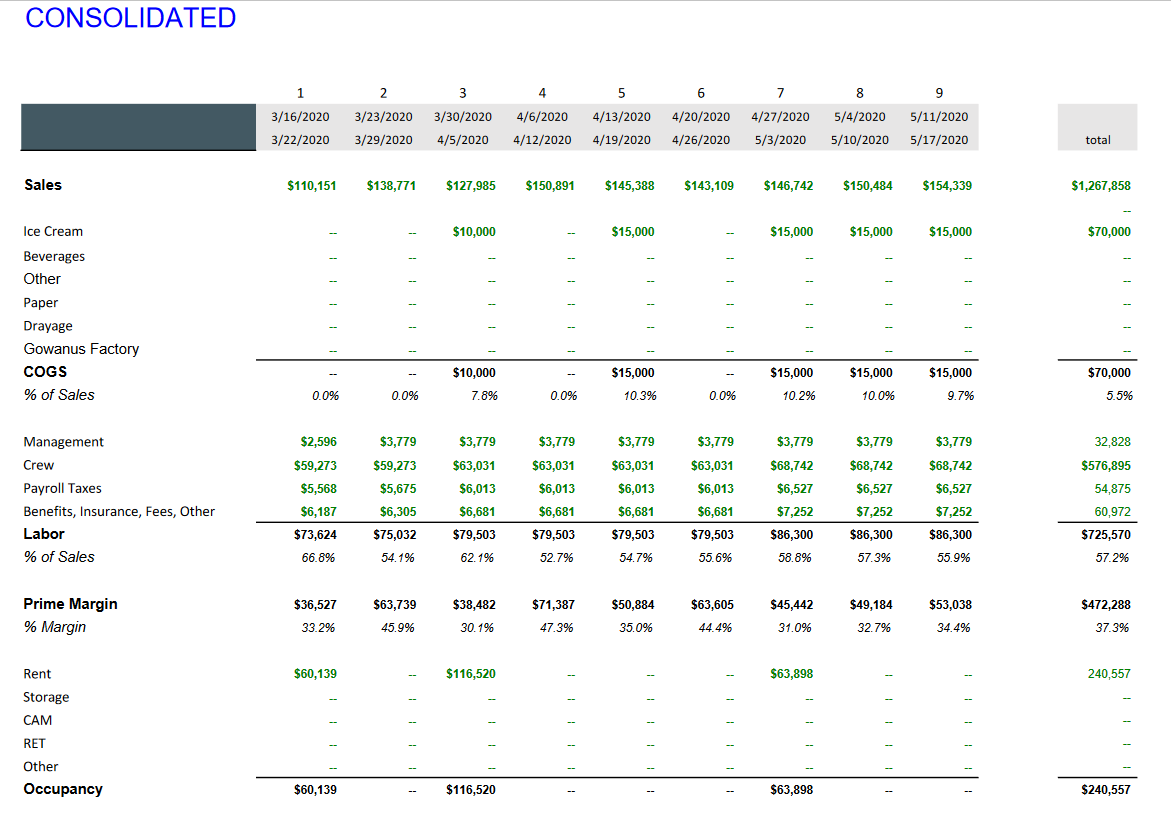

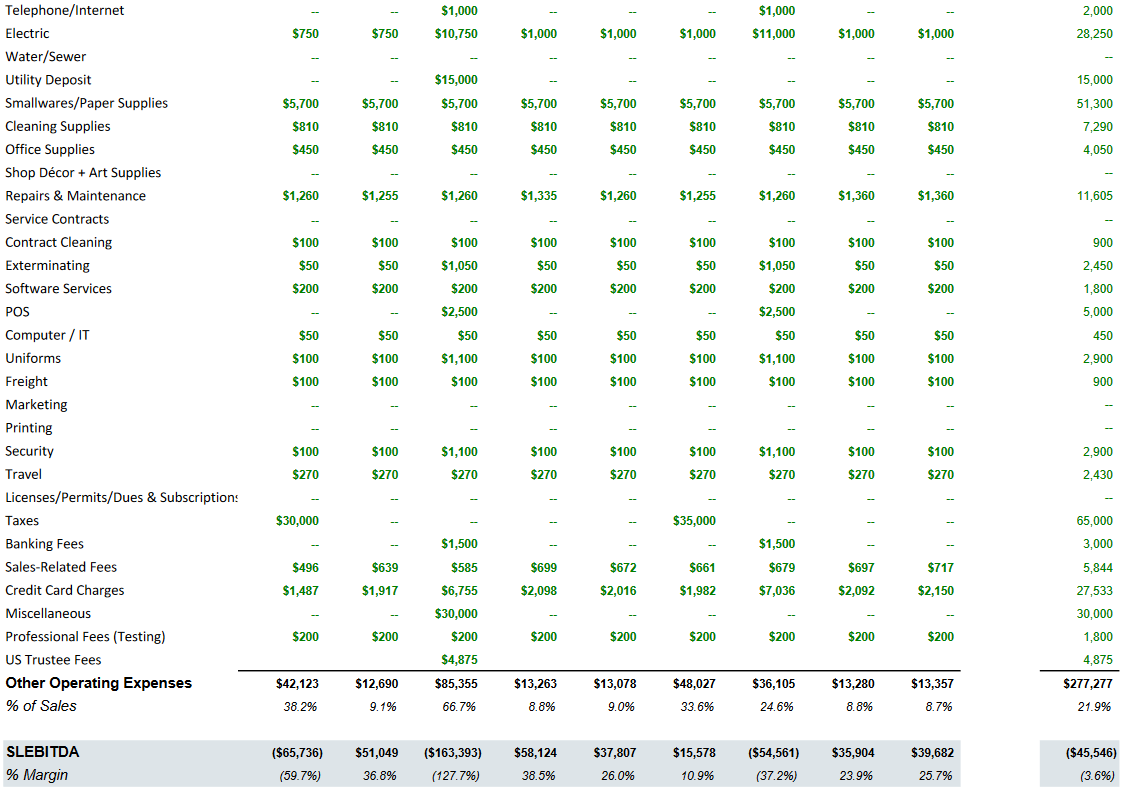

So, all we really have to go on are A. the numbers I have already presented and B. The Ample Hills post-petition forecast. This was before COVID-19, at least before the lockdown, so I am assuming its roughly the run rate of the business.

They expected to be slightly EBITDA negative. Given that this is a very seasonal business – for example Ample Hills said that their labor costs are roughly double in the summer of what they are the rest of the year, that they are close to EBITDA breakeven from March to May seems pretty decent.

The other thing I could do is add up all the cost disclosures from Ample Hills and see what that sums up to. As part of the filings Ample Hills has provided utility costs, lease costs, labor costs usually at a granular lease by lease basis (including phone, internet, gas, electric – its pretty detailed). They’ve probably covered a lot of the operating costs. I haven’t gone through this exercise yet, but I have it on my list of things to do. It is going to be time consuming though.

The biggest issue I think is how does Schmitt either A. get this Factory up to its utilization rate or B. reduce the Factory costs to a point where it is not such a big drag on the business.

So there is a lot that is unclear here. We don’t know

- What Ample Hills looks like post-bankruptcy

- What assets Schmitt is taking on

- What they are planning to do with the Factory

On top of this there is also this whole pandemic thing, which it kind of goes without saying is a bit of a fly in the ointment (though maybe the worst is over for New York?).

Nevertheless, I can’t help but think that a couple million bucks for a business with this kind of social media presence, a strong following in one of the trendiest cities and a history (pre-Factory) of doing pretty well on a store basis, is a pretty cheap price.

As an aside I talked with Zapata literally the morning of the same day (June 9th) that the bankruptcy court awarded them the business. I talked to him because I wanted to better understand the go-ahead plan before deciding on what to do with the Dutch auction.

He did not so much as hint at Ample Hills. Like not even a vague comment about good things being in the works.

I really respect that. He is very forthright that he will only disclose to you what he has disclosed for everyone. I think that is a very good sign.

Schmitt has the cash to turn this business around. To wait out the pandemic. It is going to eat into the “value” story, but it also adds a whole other layer of upside.

Of course, it is also total thesis creep. But we always figured they would do something with their money. We knew they were going to burn some of it trying to right the Xact and Acuity business.

Schmitt can now focus their attention on a well-established ice cream business – that seems preferable to me. It is probably riskier than it was when this was just a cash and asset play. But I think the upside has grown quite a bit as well.

Great write up. Can you point me to the docket?

Sure – https://cases.stretto.com/amplehills/court-docket/#search

I’m in Brooklyn and can report that Ample Hills has a large and robust following here, and that people are buying a lot of ice cream there.

That said, the business is so brutal. They have proved their mettle by surviving for some time, but getting growth in that category kills a lot of brands. If you want distribution you have endless competition (there are multiple NYC-based brands looking to go regional/beyond, not to mention all the regional and national brands fighting for freezer) and if you just sell it out of your own locations you’re saddled with a whole host of costs.

Maybe it’s Haagen Dazs 2.0, or maybe it’s Jeremy’s Microbatch. TBD!

Thanks. Yeah it seems like a tough business in many ways. In my two discussions with Zapata one thing he mentioned more than once was that they plan to be super careful with capital allocation. So with Acuity and Xact it was like – we’ll invest a little over the next year and if it doesn’t work we are done with it. I am hoping that’s the strategy here too – they spent a couple million to acquire it, maybe they invest another million (I’m guessing?) and see if they can turn it around and if it doesn’t go they walk away. I can only guess that’s the strategy (I didn’t want to bother called again so soon after talking) but it would be consistent if it was.

My other consideration is that at $2mm it doesn’t take a lot to get a good return on the investment. Even if they don’t become Haagan Daz 2.0, if they can become Ample Hills circa 2016, its probably worth more than $2mm.

Agree 100%. The main risk I see is that they go pot committed. That’s what the founders did with the Factory (which includes a museum!), and why they’re here today. Growth and scale-building are so tempting in this, but as the above numbers show that can very easily burn through all of Schmitt’s cash. I think the best case scenario is that they approach this as bridge financing: keep the brand image intact while generating modest cash flow, and flip to someone with ice cream dreams (I think keeping and growing modestly is sub-optimal just because it’s a restaurant biz, and thus terrible). $2MM is a super-undemanding valuation to make a profit from (so long as they don’t plough that much more into it). The good thing is that they have a game plan and are not as emotionally invested as sellers (and, one can dream, eventual buyers).

So, yeah, as long as you have faith in Zapata, et al. approaching this the right way–and you do, so I do–it seems like your thinking is spot on.

Looks like they agreed to a lease amendment for the Factory. That’s a positive step: https://cases.stretto.com/public/X055/10131/PLEADINGS/1013106272080000000015.pdf

Looks like an entity called RoseCliff Ventures is trying to object and say they will bid $1.3mm. No idea how this plays out but it will be decided tomorrow I believe: https://cases.stretto.com/public/X055/10131/PLEADINGS/1013106292080000000098.pdf

Overruled. Looks like a done deal.