Week 471: Siding with Carry

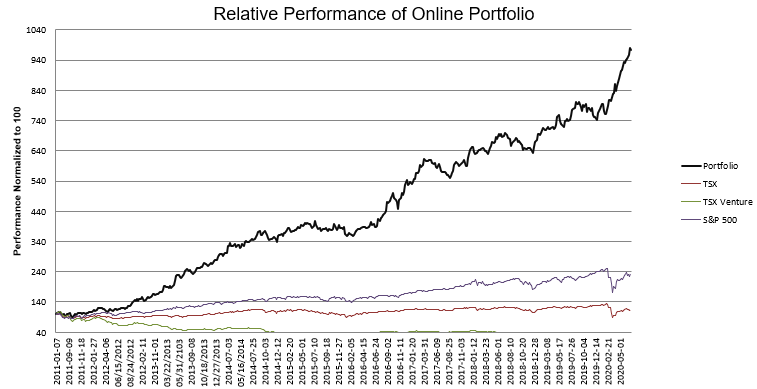

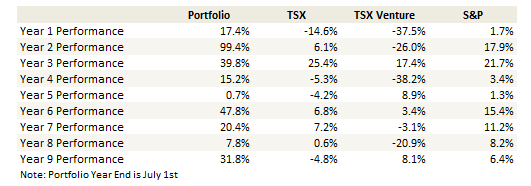

Portfolio Performance

Thoughts and Review

I finished reading the book The Rise of Carry. It was recommended in a comment a couple of weeks ago. I thought it was a really good book. It made sense of some things that were already floating around in my head and that I’ve written about lately but where there were details and mechanics that I didn’t really understand. I’m actually reading the book for a second time right now because there is still a lot of it that I’m fuzzy on, but I’m going to write about what it has made clear to me.

The book’s big picture idea is really simple. The authors believe that markets are now being driven by carry trades, that this is the main mover of financial markets (more so than the economy) and that one carry trade in particular, the S&P volatility carry trade, has become so ubiquitous that it is driving all markets together.

So what are carry trades? Carry trades are financial transactions that make money when nothing happens. The authors describe them as the financial equivalent of selling insurance. They are usually leveraged. They add liquidity to the market. They tend to follow a pattern of long periods of stable returns followed by sharp, sudden draw downs.

Another way of saying this is to say that carry trades sell volatility. Volatility is a measure of how much a market goes up and down. How volatile it is. “Selling volatility” means that you are making a bet that the market won’t change by very much, or at least that changes will be gradual.

The pattern of these trades follow the patterns we are seeing more and more in markets. Long periods where basically nothing happens (stocks go up slowly), followed by sharp collapses like what happened at the end of 2018 or what happened in February and March of this year.

The argument made by the authors is that these patterns are being caused not by economic considerations (the market isn’t going up and down on hopes of an economic boom or fear of a recession)

Carry trades are a natural part of the financial market. Most of the time they act as a way to help capital get allocated to where it is needed. What makes the current period unique is that central banks have greased the wheels of carry-trades. The unlimited liquidity that they have provided has created a “put” (a put is something that limits losses if markets start to fall) that has allowed the carry trade to morph into something with a much larger influence on markets and the economy than has ever been the case in the past.

Carry trades started out as a currency phenomenon – in the 1990s and early 2000s most carry trades centered around currencies. They took advantage of interest rates spreads between countries to sell one currency (usually the yen or dollar), to buy another (such as the currency of Australia or an emerging market). They would then use that currency to buy high yielding debt instruments from that country.

More recently carry trades have moved into the stock market. This change occurred after the Great Financial Crisis of 2008. Today the biggest carry trade out there is to short volatility on the S&P.

Through the book they argue, and use data to back it up, that carry trades – ie. selling volatility and specifically selling S&P volatility, as a source of leverage – has become the driving force of markets. Its influence has gotten to a point where carry-trade induced draw downs of the stock market drive economic events, rather than vice versa.

This is a really important conclusion. If its true, then everything we know about why markets go up and down is wrong. It explains why the markets seem to be indifferent to what is actually going on in the economy right now.

If the view is true markets will follow a typical carry-trade like pattern: we are likely to have long periods of slowly rising markets followed by steep, short squeeze induced, crashes.

We just saw one of those crashes. The book makes clear that every crash must be followed up by a doubling down on the “put” by central banks. If not, the entire carry-trade centric regime risks deflating for good (the consequences of this would not be good for anyone). In this crash, like all the others in the last 25 years, central banks rose to the occasion, once again came to the rescue, supplying massive liquidity to get the carry-trade back on its feet.

Another important point relevant to the present moment is that the central banks just doubled down again. It seems unlikely to me that we will have another crash so soon after this. The carry trade bubble needs to inflate again, and then, once liquidity is tapered off, another crash will come.

Each successive reflation of the carry-trade makes it bigger. The authors describe it to be analogous to a Ponzi scheme. Each time a Ponzi scheme is on the verge of collapse, it must get even bigger if it is going to survive (it needs enough new capital to pay out the existing holders). The carry-trade regime that we are in has many similarities to a Ponzi scheme and this is one of them.

A lot of what the book says is what I have already suspected but haven’t had the tools to put my finger on. It is very worthwhile to read for that reason. It reinforces my thought from the last couple of posts – that A. Portnoy is right and B. you don’t want to try to short this market. It also reinforces my resolve that at some point this will not end well.

We may be at ridiculous valuations and speculation may be rampant, but given that the carry-trade is back in full swing – ie. that central banks have provided the liquidity to give it another lap around the track – I’m not sure if the market can fall far from here. We could get another 10% drop like we saw a few weeks ago, but if the authors are right (and what they are saying feels right to me) that dip would be bought. Until there is a liquidity event that will “shock” the S&P volatility carry-trade (and to be clear, I am saying a liquidity event, not an economic event or even, I suspect, a rising hospitalizations event), it is all systems go for the market – economy be damned.

My gut tells me that the smart decision would be to lighten up on shorts and let the longs ride. That would be the path to greatest returns. What I’ve read in this book only enhances that intuition. Like I said in my last post – I suspect that Portney is right – stocks really should only go up right now. And not because of the economy, not because of valuation and not because it makes any kind of historical sense, but simply because the carry trade is alive and well again, that volatility selling is self-reinforcing until it is not, and that all this engenders a rising S&P, which floats all boats.

So that is what I probably should do. If this was 2011 and I was where I was then, I probably would do that. But I’m in a little different spot now. I’m more willing to let some gains get away in return for a little less stress and a little more piece of mind.

I have to follow my process. So while I may lighten up on my index shorts on the next correction, relying on my suspicion that we can’t fall too far with the central bank put in place (which, after reading this book, is truly aptly named), I’m not going to go all in.

If my gut is right this will mean that I will continue to lose money on the index shorts and that will be a headwind to my performance. That puts more pressure on my stock picking, which is fine. My shorts are my own put on the put. The book points out in its somewhat depressing conclusion that the eventual conclusion to all of this is not all that rosy. It is likely that each successive resurrection of the S&P carry trade will lead to successively larger collapses until eventually the whole system is put into question – ie. that we question the legitimacy of the central bank put itself.

We are probably a long way from that point, but I will sleep better knowing that I have my own put against it anyway, even if it comes at the cost of some return.

In the mean time, what this means is that the Robinhooders are probably right. There is no sense in looking for value, deep analysis of businesses or weighing the economy as elements in stock selection. Or at least, those considerations are secondary to the question that really matters – what is most likely to go up?

That statement may sound superfluous at first glance, but I don’t think it is. What it is saying is that instead of picking a stock that might seem undervalued and waiting for the market to see that value, you are better off (in this market) to look for the stocks that others are likely to buy, before they buy them, and don’t pay too much attention to what it “should” be worth.

I suspect that this may be exaggerated even more than it might have been because of the unique environment caused by the pandemic. Like I wrote about in my post about the bi-furcated economy, some indsutries are basically knee-capped by the pandemic, which means that even more money must flow into the sectors that remain viable.

I am trying to take advantage of this idea with a few small purchases. I don’t have the stomach or the tools to gear my portfolio to this on a larger scale, but I’ll wade in where I can. I stepped into this a little with a purchase of Graf Industrial a couple of weeks ago.

I actually bought the stock for totally the wrong reason. I liked the potential acquisition of a plastics recycling technology firm that they said they were going to buy. While not named in the press release, seemed almost assured to be a company called PureCycle. PureCycle has a very cool technology that lets you turn a plastic container back into virgin resin. This allows you to take a #5 yogurt container and recycle it into another #5 yogurt container. In the world of plastic recycling this is a real game changer.

Like all SPACs I did not know what Graf was paying for PureCycle, nor did I know anything about PureCycle’s financials apart from a few tidbits I could gleen from their website. But, as the previously mentioned axiom implies, who cares! It is not the valuation but the likelihood that it will go up that matters right now.

Of course what ended up happening is that instead of buying PureCycle Graf decided to buy Velodyne LiDAR. LiDAR is autonomous driving and next-gen driving technology is even hipper than recycling right now. The stock shot up.

I wasn’t smart enough to hold on for the entire ride, but I caught a few points before I sold out. Ironically, I sold way too soon (at around $15-$16 instead of $20+) because (in my opinion) I knew too much. I have followed Foresight Autonomous for a while, and while the technology is different and the applications not entirely the same, there was enough overlap, and I’ve seen Foresight struggle for long enough, that I was skeptical of the eventual ability of the business to generate growth.

It is only in a market like this where experience, and therefore skepticism, is a handicap.

I have 3 other plays that I would characterize as being along the say line as Graf Industrial. I’m not sure what the right word is for these ideas, momentum or greater fool or just stocks that I think have a good chance of going up regardless of whether I think they should or not.

The first is AYRO, which was a Rev Shark stock of the week pick on Sunday. I looked at the stock on Monday and at first I wasn’t very interested. It popped hard on Monday morning, maybe because of the Rev Shark recommendation but more likely because of news that they had completed a factory expansion which, from what I could tell, was just a recycling of what was already in their filings.

But after the company announced a registered direct offering for $4.75, I changed my tune.

There is a lot I don’t like about this stock – again these are trades to try to take advantage of the market we seem to be in, not investments where I have confidence they can stand on their own merit. AYRO produces low-speed vehicles – these are kind of like golf carts with flat beds, pickups or boxes. They only do the final assembly – there is a Chinese company that manufactures and holds patents on the products. AYRO only has rights for sale in the US and Canada. They sell their vehicles through another third party – Club Cart, which is the golf cart maker owned by Ingersoll Rand. I have to wonder – why doesn’t Ingersoll Rand just build their own?

But who cares. My thesis here is simple. Someone was willing to do a deal at $4.75 yesterday for $15 million. This comes two weeks after a deal was done at $2.50 for $5 million. Something doesn’t add up about that unless whoever did the deal yesterday believed they needed to be in the stock regardless of what they paid.

I have no idea why they would pay so much. The only thing I have been able to dig up is that Ingersoll Rand Industrial was bought by a company called Gardner Denver and the Club Cart business does not really fit with the rest of the portfolio (which is indutrial valves and compression fluids and such). Barclays said a couple of months ago that they think Club Cart is going to be divested. This is something, but I’m not sure what, and the links to any positive move in AYRO are tenuous I admit. But AYRO has a market cap of $85 million or so – in the land of EV’s where no valuation is too high right now, this is a pretty low base to start from.

My second purchase was Envision Solar. This is a stock that @IPHawk has been talking about on twitter for a while. Envision makes solar powered electrical charging stations. The thesis here shares a few traits with AYRO – first, the market capitalization of Envision Solar is $70 million – so there is plenty of room to run on speculation. Second, like Ayro, Envision raised a bunch of money ($10 million) and the stock went higher after it did. Third – its EV’s and solar. In this market, that’s enough for me.

My third purchase is a bit of a different take on things. I bought YRC Worldwide. I realize the company is pretty dismal, and that the trucking industry is not exactly one of those pandemic-proof businesses that I have tried to steer myself to, but on the other hand YRCW just got $700 million of low-interest debt. Apart from their pension liabilities, this is basically 100% of their existing outstanding debt. That doesn’t mean that they will pay back their debt with this debt or anything like that, but it gives them a whole lot of runway to do something. Anything. Another restructuring, buy some new trucks, maybe add technology to improve efficiencies. Will they be successful? Probably not. Will the stock go to $5 before that turns out to be the case? In this market, and given that the market capitalization is only around $100 million, I think that is a reasonable possibility.

I talked about most of my other stocks in my last post so I won’t go through those details again. I sold Overstock yesterday, which looks to have been a mistake, seeing that the stock is up another 15% today. I also bought a bunch more Slack Technologies, which may see another pop if the virus escalation continues (this is part of my thesis that stocks will go up and that the money chasing them will have to go into companies like Slack that are doing well, regardless of their valuation). The only other names I considered mentioning here were the small basket of biotechs that I have been holding. These have done pretty well on whole, but yesterday I was whacked very hard by the Phase 2 results from Obseva – the stock fell 50% and today it is falling again. Anyway, this tempers my enthusiasm because, and I have said this before with respect to biotechs, what the hell do I know? Not much.

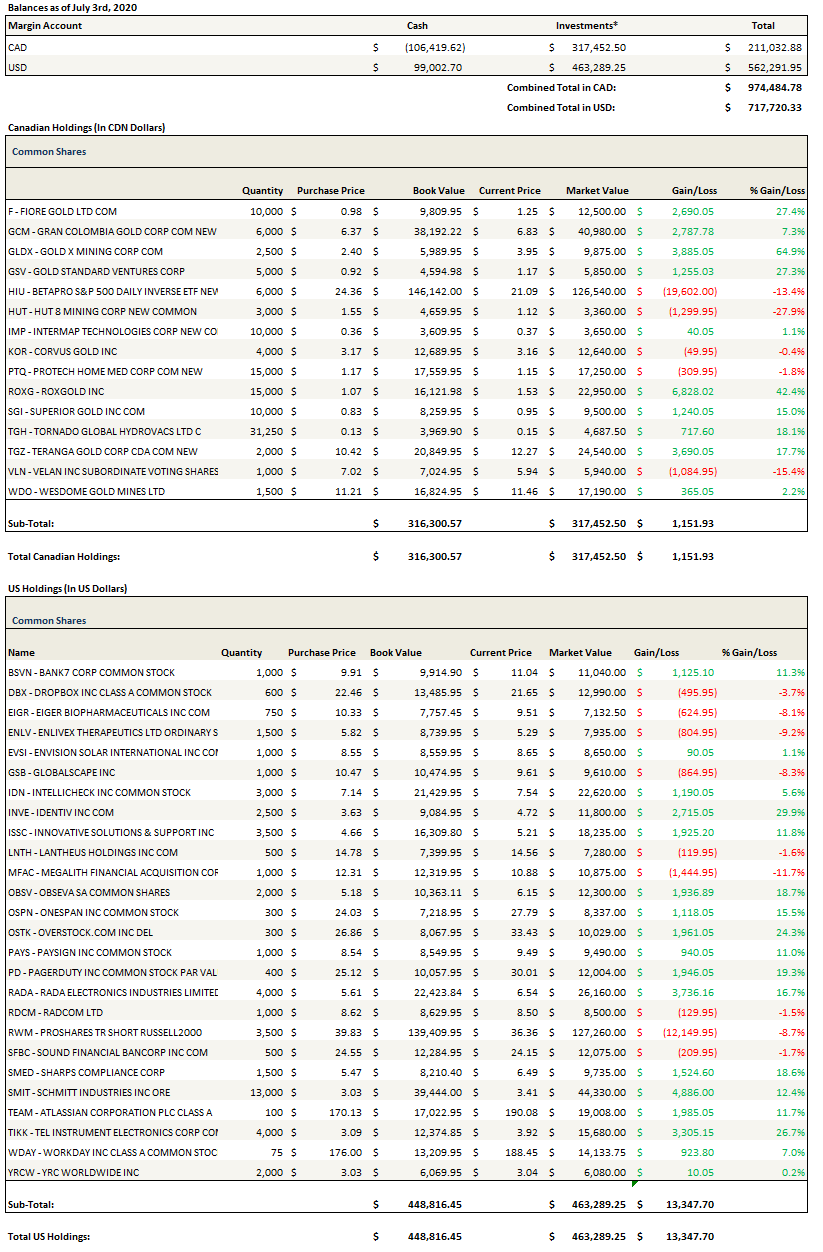

Portfolio Composition

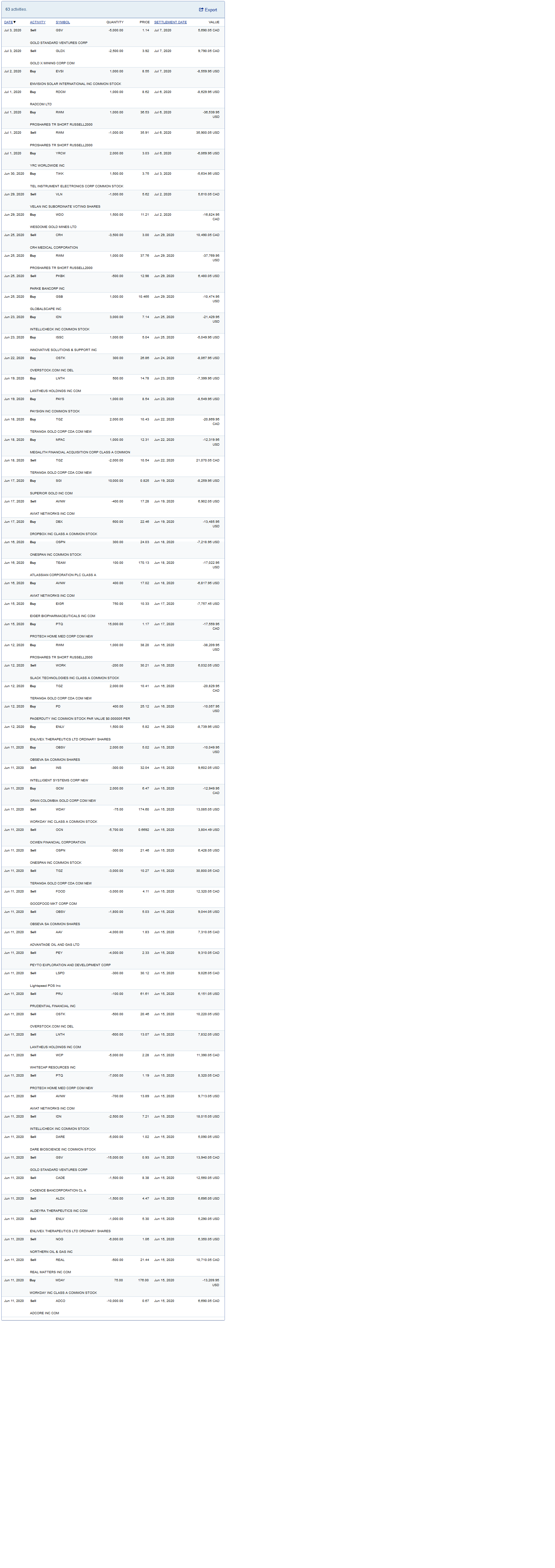

Click here, here and here for the last nine weeks of trades.

{kind=link}

{kind=link}

{kind=link}

Lane

I suggest you look into the work of Mike Green about the role of passive investing.

https://ttmygh.podbean.com/e/teg_0003/

https://www.logicafunds.com/blog-research

Congrats to your performance

That’s interesting thanks. He said the same thing I just did in my earlier comment:

For those of us who lived through the United States mortgage crisis, either directly or through the vivid descriptions of Michael Lewis’ The Big Short, this should not be a surprise. It’s the same story all over again.

Yeah.

On the other hand…is it? If Mike Green is correct, what follows is not a crash but a steady march upward.

It is also hard to see real major bubbles for me. Sure in select stocks like Zoom, Tesla, lots of SAAS, IPOs, etc

But overall the big winners seem expensive but not totally nuts.

Yeah the way I’m thinking about the analogy to mortgages, right now*, is that we are early, this is 2004 (maybe?) meaning we just hit the gas pedal with the virus response and its eventually going to end really badly but we have a crazy period ahead of us in the mean time before that happens. But a lot depends on just how big and influential the short vol trade is (and maybe this whole passive move is though I’m not sure I totally understand that side of it yet?). With mortgages I think the derivatives were ~20x the market before it blew up. I wonder where we are with this?

Hm. I guess the passive move is very long term. Not 1 or 2 years but rather decade(s).

Isn’t short vol very established? I mean it is certainly nothing that came up just recently. Japanese life insurers have done it for a long time for example.

And does it have to lead to a total disaster crash? Like worse than ever?

I haven’t read the book of course.

But I just read this https://squeezemetrics.com/download/The_Implied_Order_Book.pdf

“The Implied Order Book:”

Describes how options generally affect S&P liquidity and why really hard crashes are facilitated, while mere pull backs are bought.

Again I haven’t read the book, but to me there are many factors, one of which is the carry trade, that affect today’s market.

And as you mention mortgages, wasn’t the issue that CDOs were manufactured *in order* to blow up? Like individually they looked fine, but taken together they were extremely vulnerable to minimal house price corrections.

This goes into some detail on

https://nathantankus.substack.com/p/is-there-really-a-looming-bank-collapse

I’m personally not saying there will be a total disaster crash. In fact, I’m actually trying to say exactly the opposite.

However, the nature of carry, according to the book, is that each reflation must necessarily be bigger than the last. And the nature of carry is long periods of stable returns followed by big draw downs. So you can extrapolate those two characteristics and what they suggest. But whether that extrapolation is accurate depends on a lot of assumptions I’m sure.

Big picture to me is strategies coming to more dominate flows act independently of valuation. Traditional active discounting is dying in favor of these strategies.

That is probably correct. At least for the major ETF holdings, large caps, etc

I would say.

I think there is still lots of hunting ground in small and micro caps though, as well as abroad.

Ah, funny about Graf. I went down the same path, looked at Purecycle, concluded that it was a cool technology but that Graf would be almost certainly be massively overpaying (how much for a warehouse and a few employees?), and passed. Wrong move!

Even without the Lidar, hypothetical valuation shouldn’t have been an impediment (I was looking at the warrants–in for a penny…). The market is rewarding deals, and I was too dogmatic.

On a similar note, am still trying to figure out what to do with Megalith Financial (MFAC). They have a letter of intent and it looks like they may be buying Bankmobile from CUBI in an extremely related-party deal. It could just be that Jay Sidhu is founder of both the SPAC and CUBI, which owns Bankmobile, but the SPAC’s target is described in identical language in the letter of intent PR. And in CUBI’s most recent earnings call, management said Bankmobile WILL be sold this year (they tried to unload Bankmobile in the past, and after a year-long process gave up, mostly, I think, because of regulatory approval).

On the other hand, the SPAC has had a lot of its funds redeemed when the deal extension was approved, and in terms of market attention, banking ain’t online gambling. Plus the LOI was signed two months ago, so who knows what snags have been hit? I am long a few MFAC warrants (sold most when they sharply appreciated, along with all other warrants) and have some CUBI calls, on the “logic” that any deal will excite everyone, even investors in a bank currently trading at half tangible book value (unless they really got walloped by impairments).

Just FYI, not that anyone was asking!

Funny again – MFAC is another I bought a tiny piece of. Same reason, saw same stuff on the CUBI call, same Sidhu relationships – he put his daughter in charge of BankMobile recently, though his son is no longer CEO of MFAC which is maybe a negative on a deal? Anyway seems likely its BankMobile and they look like a good platform and growing. But I can’t figure out how its going to work with the redemptions either, they have like $35mm or so left I think, so I’m just kinda waiting on something to happen. But the redemptions are funny too because if you look at the bigger holders that had to report, they didn’t fully redeem. – In fact biggest holder Glazer capital reduced by exact amount of total reduction – 76%. Another large holder Millennium reduced but still holds 9% position. So whats the deal? I don’t get it.

Yeah, same. The only think I could think of was that bigger holders wanted the cash back in their pockets rather than waiting for a deal (it was May, so the market worst was over, but I can still see that line of thinking re: liquidity), with an understanding that they’d have the opportunity to buy back in if/when a definitive deal was struck (unless Sidhu has other backers lined up? Or is paying for it himself?). Makes sense too if the deal runs into more roadblocks. But honestly, just guessing. It’s weird.

Bankmobile is cool because it’s a real business and one that seems like it can be break-even and grow, though also far from exciting and you could argue that their target demo is even more stressed than usual now. But I’m holding on for now, and as usual kicking myself for not buying more warrants all around a few weeks ago.

I’m glad that you like the book! It really helped me crystalize a lot of the things I was suspecting when I first read it.

As a follow up to that, I thought the recent interview with Charlie McElligot on Macrovoices podcast was very interesting. As well as Michael Green’s interviews & podcasts on passive ETF flows dynamic influencing the markets. Hope you will find them helpful!

Sure I will. The more I think about the book, and read it again (and soon again I imagine) the more I think it is pretty important. This rhymes like 2005-2008 to me – but instead of mortgages its the S&P and instead of CDOs its vol. The asset can become unhinged with underlying reality because the players driving the asset are making money on side bets and those side bets are for a while at least just juicing the underlying market. So fun times – until at some point not. But honestly, and tell me what you think, but I can’t quite wrap my head around the end games they describe.

I’ll have to get back to you on the end game part as I’ve only read it once.

Everything is interchangeably linked and correlated and thats what makes this market so insanely dangerous on so many levels. Subdued vol drives up leverage in trend following strategies and cash secured put selling (something you see in many structured retail products these days – equity linked notes that pays ~7-10% dividend).

I truly believe we have passed the point of no return and that we’ll see a boom and bust cycle happen in markets every 1-2 years

I don’t have the same skills at picking small caps like you do, so I’ve changed my method mainly focusing on spotting the technical signals near turns. Would recommend you to take a look at:

Thanks for the recommendation. This is one of the most important books I have ever read.