Research – Supremex

Supremex

- market cap of $31mm at $1.12

- they have $100mm of net debt

- in Q220 had earnings of 7c, EBITDA of $6.9mm, revenue of $47.7mm

- revenue was flat yoy, envelope revenue was down 3.5%

- net cash flow from ops was $10.7mm, up from $5mm yoy

- they get $22mm of revenue from Canadian envelope segment, $10.6mm from US envelope segment

- EBITDA was $14.6mm from H1 – so that is $30mm of EBITDA on a $130mm EV

- leading manufacturer of envelopes and paper packaging

- operate 13 facilities across 6 provinces in Canada, 3 facilities in US

- manufactures stock and custom envelopes

- corrugated boxes, folding carton packaging, e-comm fulfillment solutions

- also these products: Conformer Products®1, polyethylene bags for courier applications, bubble mailers, Enviro-logiX®2and Tyvek®3and other related products such as RFID protective envelopes, X-ray envelopes, medical and file folders, repositionable notes, membership cards as well as labelling products

- Q220 results

- they have been developing new e-comm relationships

- extracting synergies from Royal Envelope acquisition

- they bought Royal Envelope for $27mm – had $30mm of revenue

- margins roughly the same as SXP – from Q120 call

- if I assume Royal had 15% EBITDA margins like SXP they would have bought it at 6x EBITDA – not exactly a steal if this is the case

- they are planning to use Royal capacity to expand US business

- said they can increase production 10-15% now without any more bodies

- their envelope segment revenue is declining

- down 4.7% yoy in Canada

- down 1% yoy in US

- revenue from packaging and specialty products has been up – 8.9% yoy

- 54% of revenue came from packaging in Q220

- I’m guessing that the stock tanked because of comments like this, though it seems like they’ve righted the ship and the stock is still down:

We announced with Q1 results that in April, we were experiencing a revenue decline of approximately 20% on the legacy business and 6%, including Royal Envelope. Fortunately, between the combination of continued onboarding of e-commerce wins and a general improvement in market conditions starting in mid-May and into June, we were able to finish the quarter at essentially flat for the corresponding quarter in 2019.

- it lines up with the chart – stock was doing pretty well until May 14 when it tanked on earnings and then kept going

- when you go back and look at last 10 years, it doesn’t really look like a melting icecube as a whole though the envelope side obviously is

- they have been using acquisitions to grow/maintain the top line, so there’s that

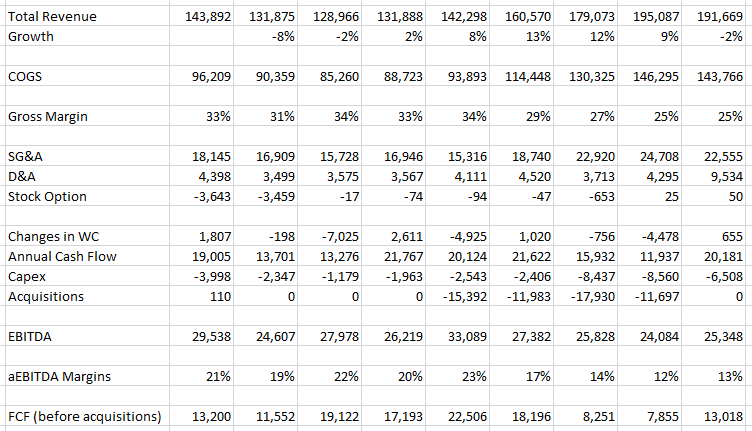

- even with the underlying envelope business shrinking, the fcf is still reasonably strong and this year’s FCF before WC is setting up to be $20mm+

- EBITDA seems to have stabilized and it looks on track to be higher yoy even with the pnademic

- so again, it may not be a growth business, but it isn’t a disaster and it generates a lot of cash

- there has been a couple of insider buys around the current stock level – $1.27ish

- I don’t really get why this stock is as cheap as it is TBH, the bad news from Q1 didn’t really come to pass but the stock never recovered from it

- 1.5-2x 2020e FCF (I’m not including acquisition capex) seems a little low

I bought some of this one last week. Not expecting the world but do think it can get back to $2.

2 Comments

Post a comment

Funny to see this; I went through the same exercise with Supremex last week, and came to the same conclusion.

I think the current price is in large part a result of: 1) The generally cursed state of value investing 2) The (temporary?) cessation of the dividend chasing away some of the shareholder base, without many eager replacements became of 1).

Dividend reduction/elimination is one of my favorite starting points, if there’s a reasonable line of sight to resumption/increase. EPM (next year) and some of the MREITs come to mind, and tehre are plenty of others.

If this was at least near debt free I would like it. Envelopes is 75% of EBITDA and average FCF the last 5 years not counting acquisitions was $13m. And Counting acquisitions only $2m. With steady declines in volume and compensating rise in prices (which I am not sure is sustainable). While EBITDA declined. I don’t think you can count acquisitions out of it, given that they nearly spent $60m (Nearly $90m counting the one in 2020) to basically earn the same as they did in 2015.

Also a weaker USD vs the CAD is a risk as it lower their US revenue.

Plus a pension liability of $100m, that is almost fully funded with 50% equity exposure.

So ended up passing on it.