Research: Alcanna

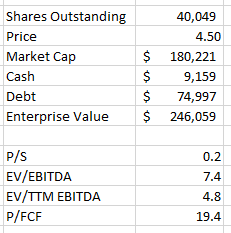

- ~$180mm market cap

- have a fair bit of net debt – $9.1mm of cash and, debt of $75mm

- largest retailer of alcohol in Canada

- top 3 in NA

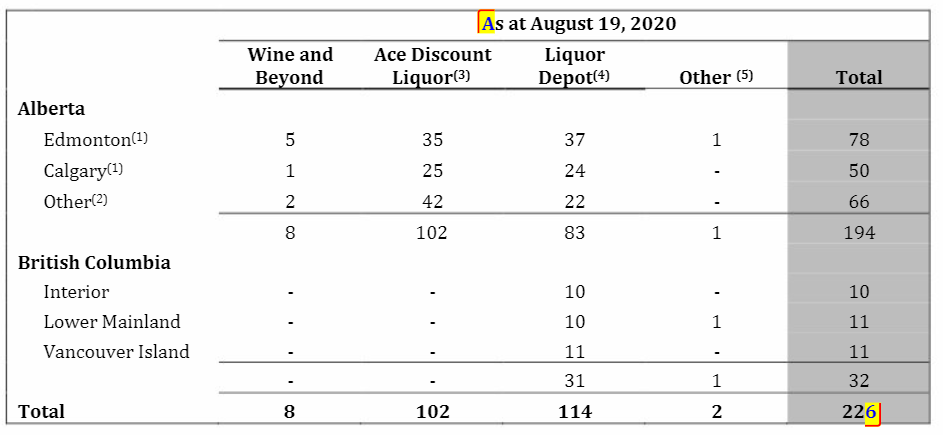

- operates 226 stores in AB, BC

- these are their brands:

- brands are: Wine & Beyond, Liquor Depot, Brown Jug

- they are mostly on the discount side

- operate in big box stores and from what I see next to groceries a lot of the time

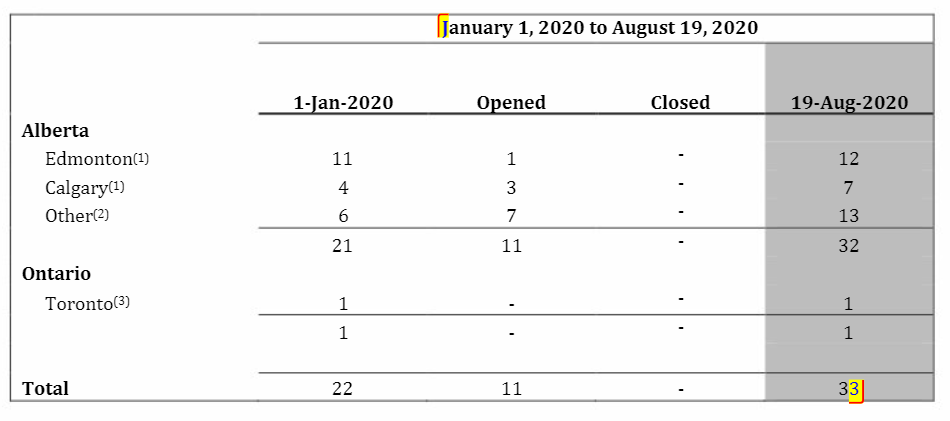

- operate Nova Cannabis business (retail cannabis)

- here are cannabis stores:

- was 25% owned by Aurora Cannabis – I think they may have sold their stake though

- on June 24, Aurora sold 9.2mm shares at $3

- that was all of Aurora’s shares according to the MD&A

Sale of Alaska business

- sold for $27.2mm

- using proceeds to reduce debt

Q220 results

- SSS were up 13.4% yoy

- gross margins were up to 22.7% from 22.1% yoy

- frequency of visits was down but avg basket size up substantially

- cannabis retail sales inline with expectations

- total cannabis sales up 64% – from $8.8mm to $14.4mm

- GMs in cannabis were $4.9mm – that is 34%

- plan to open 2-4 new Nova stores in AB

- opening 6-7 stores in Ont

Q2 CC

- our results since May and right through till sitting here today have not changed

- Anecdotally, we’ve heard that even people who do go to restaurants are not staying. They’re eating fast, staying — in and out, stay for an hour, and — which the restaurants are encouraging to try to get some business in their limited-capacity footprints now. Not ordering the second bottle of wine. Not having the predinner drinks or the cocktails or the after dinner, and — all of which, I think, is playing into our belief — our strong belief that this is not just a onetime blip, it’s a trend and societal and consumer behavior trend that will be in place for the foreseeable future.

- Our company has shifted, quite dramatically, its focus, and we’re essentially, for the most part, a discount liquor company now

- our Ace banner has 102 stores, whatever it is, and Liquor Depot is 79 now. So — and Wine and Beyond, which is our large-format store, which does have luxury products but it’s not a luxury store, its margins are more or less the same as Ace

- on cannabis margins: That’s pretty much standard for the industry, as I understand, reading some other people. And we just — we obviously go comparison shop our other retailers. Most people are — started getting around 34%, 35% margin right now.

- more on cannabis: Our stores have been extremely stable on a sales-per-week basis because we’re in good locations. But ones who are in terrible locations, which is the vast majority of them, are just having more and more stores sharing tinier and tinier pieces of their part of the pie. And the only competitive response people in that situation can do over time, if you look at any retail 101, is drop prices

- we don’t anticipate margins staying in the competitive environment at this level for too much longer in Alberta – sounds like AB cannabis retail market is saturated but so is wholesale so prices just overall will come down

- But it’s 35%. 35% is just not sustainable for a long time in any retail. It’s just there’s too much — you do very well at 35% in a retail environment

- on liquor side they can’t keep inventory: The other place that we’ve increased inventories is just we have some stores that are just doing gangbuster numbers, and we needed to put more inventory in there to support those increased sales. And then the third place, as you pointed out, is there’s been some great deals on some LTOs from the vendors, and so we’ve stocked up to keep our margins healthy and remain competitive in the marketplace.

- step up in inventory buying in Q220 was deliberate: We made a deliberate — we sat down with our operating team, and they asked, and they had a well-thought-out plan for — wanted as much as — at the high point, as much as $10 million to $12 million extra dollars to invest in inventory because of the LTOs they saw coming and the conversations they’ve been having with vendors as to what might be possible. So it was a very deliberate thing we did. And you’ll see the benefits of that on the income statement over the next quarters because it’s purchased now, but the pricing is — it will have the impact on — positive impact on margins going forward. So yes, it was strategic. It was carefully done

- more on store sales: some of the stores, especially the Wine and Beyonds, we just literally couldn’t keep — the shelves are running out every single weekend. Those stores are doing Christmas-like numbers week after week after week, and we just couldn’t literally keep it on the shelf.

- in strong position for lease renewals: like 10%, give or take, whatever, of leases every year come due. So yes, no, absolutely. I think we can say with almost certainty there’s not going to be any rent increases, for sure. And it’s situational, case by case. If you’ve got some of our great Liquor Depots in — which have restrictive covenants in a grocery-anchored mall, which do very well, and we wouldn’t have the same leverage you might think we’d have with the landlord because we — if you say no, they get somebody else.

- more on leases: other situations, we do have tremendous leverage. Obviously, one of the very few retailers right now who is not only able to pay the rents but very comfortably able to pay the rents. So we’re a very desired tenant. Always have been, but even more so now

- if we’re patient, to get some extremely attractive real estate for very extremely attractive rents to build Wine and Beyonds, especially, in places where so far we’ve had trouble, namely Calgary and British Columbia

Insiders

- been buying a lot of shares

- bought around 100k shares in Aug/Sept at around current price

- Before that, in June-July had bought about 175k shares at a little over $3

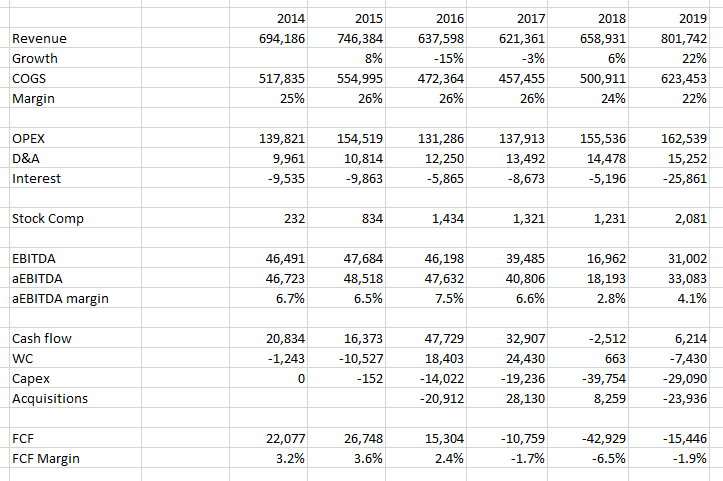

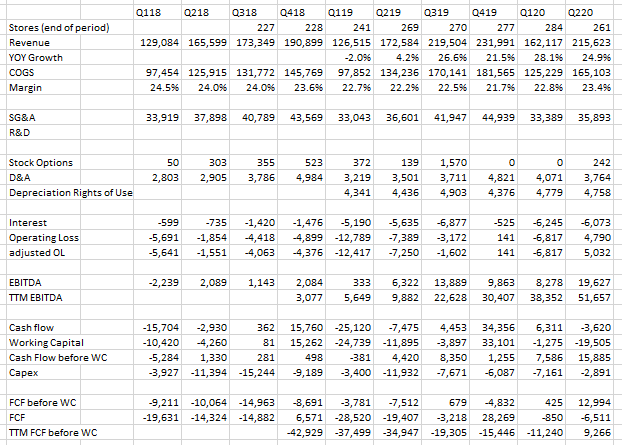

Financials

- Long term:

- Short term:

- business really accelerated last quarter – no surprise

- FCF last quarter was negative b/c they built inventory – before WC FCF was $13mm

- I kinda like this one – seems to me that cases in BC and AB are going up not down, BC just shut down their bars and clubs, AB maybe not but who is going out right now – tailwinds for a few more quarters at least and this stock isn’t pricing in that like other pandemic stocks

No comments yet