Research: SharpSpring

Marketing Automation

- marketing automation is really about driving leads and sales and revenue for our customers

- enables them to drive more leads and sales at a time when converting every lead possible into a sale

- help along the entire sales funnel

- With regard to the value of marketing automation, marketing automation is really about driving leads and sales and revenue for our customers.

- Even in a pandemic situation, SharpSpring enables them to drive more leads and sales at a time when converting every lead possible into a sale matters more than ever.

- enables them to optimize their entire marketing and sales process, enabling them to understand what’s working and what isn’t and eliminate the things that aren’t working and double down on the things that do.

- the TAM, the total addressable market, is massive when it comes to marketing automation

- estimated to grow by folks like Gartner and the rest to $14 billion by the end of 2014 — or excuse me, ’24

Legacy Alternative

- just beginning to see the adoption as people get frustrated with managing all of these point solutions that were never designed to work together, that don’t include the automation or any of the tracking

- at the beginning of the industry’s — or the world’s adoption of marketing automation

- A CRM system, a landing page builder, a forum builder, a social media management platform, an analytics package, an e-mail package, all of these things don’t work together well and create a very brittle marketing technology stack.

- Marketing automation solves that by incorporating all those technologies into an integrated solution that is wrapped around a core technology

Product

- we had a very weak product

- We launched in 2014

- we launched with a hugely disruptive price point

- offer our services for as little as 1/10 the cost of a comparable solution

- core technology is an integrated database

- and a core tracking technology that today will track literally billions of clicks from our agency — or excuse me, from our customers, every one of our customers’ websites, every visitor to every one of our customers’ websites and every click on an e-mail or landing page or website runs through our rules engine

- rules engine is the core technology of a marketing automation platform

- Form builders, landing page builders, e-mail marketing, social media management, chat bots and the list goes on – wrapped around this core tracking technology

- the rules engine that makes all of marketing automation possible is really the stuff of computer science textbooks

- pulling off a marketing automation solution is incredibly hard. It’s really 20 products at this point rolled into 1

- any click could tick off an automated event such as increasing a person’s lead score, a lead score, sending an e-mail or Drift campaign to that lead, notifying a salesperson that a lead has changed status and is now worth working on

- top-rated platform by every major software review site that’s out there, G2 Crowd, Software Advice, Capterra

- Nearly all of our revenues are SaaS business.

- 7:1 LTV to CAC ratio

- lifetime value, we believe, is — for an agency partner is north of $50,000

- During the COVID time period, we’ve been acquiring customers for south of 10,000 rather than 7,400 as represented here

- are acquiring customers that we think are actually now worth just north of $50,000

Customers

- SharpSpring competes is in the SMB and mid market

- 85% of our revenues flow through digital marketing agencies

- have about 2,000 agencies that we think of as our customer, but they act a lot like resellers

- agencies serve essentially as augmenting an internal marketing department or is a completely outsourced digital marketing department for the SMBs that hire them

- these agencies typically have between 5 and 50 employees and have many clients – between 10 and 100 clients

- No single client represents more than 1% of revenues and the vast majority of clients represent less than 0.1% of revenues.

- have thousands of clients

- their low price point – have not found ourselves on the menu when companies look to cut back in an effort to save costs.

Revenue

- revenue model, there’s really 4 parts to it

- First and foremost, we want to land new customers – means landing new agencies

- that leads to our expansion potential within each agency

- core mission is to expand within the agency, to get the agency to move from 1 client to 2, 3, 4 on up to 5, 10, 15. Our largest agency has over 100 clients

- fourth is pricing power

- are, far and away, the low-cost leader in the space

- ability to increase our prices significantly over time without fear that agencies would — or excuse me, clients would move in a different direction

- are literally 1/10 the cost of most of these solutions, but for a product that is every bit the equivalent of what they offer

- in order for competition to come down to compete with us, they would cannibalize themselves

- first 3 categories are what it’s all about for us, expanding the number of clients within each agency and giving them more products and providing value that way

- Beyond that, we can cross-sell and we can up-sell

- one of the things that people don’t understand about our business, we have high logo attrition

- see the heaviest attrition taking place in year 1 and are focusing on executing within that year time frame to become a more sticky platform

- can sign up on a monthly agreement and pay a very small onboarding fee to get started with SharpSpring

- no clear way for us to tell which agency is going to take off and add 15 or 20 of their clients to the platform and which agency is going to fizzle out after 6 months in a trip

- reported a 99% year-over-year net revenue retention number prior to COVID

- this last quarter, we reported roughly 92% revenue retention

- backdrop of 3% logo attrition on a monthly basis, so very high comparatively logo attrition

- only ever lose low-value agencies

- those characteristics, including the higher logo attrition, is built into our lifetime value calculation, which is north of $50,000

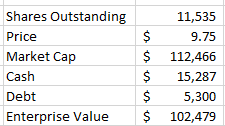

Recent Financials

- latest guidance, which is around $30 million of revenue

- We are continuing to grow healthily despite the pandemic conditions and have really never been more stable as a business than we are today.

- I need to — this slide does not gel with our latest guidance, which is around $30 million of revenue.

- We’ve also increased our cash position and are at around $15 million of cash on the balance sheet as of this point and made significant strides this last quarter towards both cash and EBITDA breakeven.

Competition

- competition is same as its been for years

- we compete with exactly the same companies that were on my business plan from 2011 before I started our company: HubSpot, Marketo, Salesforce, Act-On and Pardot

- Adobe just purchased Marketo last year, I believe, for $4.5 billion

- compete and win every day versus HubSpot, Act-On, Pardot, which is now part of Salesforce

- compete with Marketo on occasion

- we aren’t up at the enterprise space, which is mainly where Marketo exists

- smaller companies better served by companies like Mailchimp and Constant Contact

- they are leader in agencies – HubSpot has long since stopped reporting on their agency count – last number we’ve ever heard from them at 3,000 agencies

- other companies were the first movers in the space. They certainly have much, much higher price points and that serves them well

- competition has built up cost structures around those price points, have field representatives

- HubSpot does an inbound conference every year that, I believe, costs them something like $20 million

- if you go to any one of these software review sites, which are effectively the analyst for SMBS, right? SMBs don’t really go to Gartner. But they do go to Capterra, which is a Gartner site and look for reviews. And our ratings there and the number of ratings and the brand awareness is really started to pick up a little bit and we’re included in more bake offs, and we’re attracting a little bit larger agency, which is sort of exciting for us

Perfect Audience

- acquired in Q4 of 2020

- acquired substantially all the assets and assumed certain liabilities of the Perfect Audience business unit from Marin Software Incorporated, a Delaware corporation for cash consideration of $4.6 million

- Perfect Audience platform employs a usage-based revenue model

- Perfect Audience platform acquired in November of 2019 generated an additional $0.62 million of new revenue for the three months ended March 31, 2020

- retargeting and digital ad platform and we can bring those types of products to customers – basically an advertising platform

- allows a business to put all of their ads in one platform and yet advertise across dozens of digital ad networks including Google’s digital ad network, Facebook; Instagram; Smaato; OpenX; Rubicon, which is now, I believe, Xander — no, excuse me, the Rubicon Project, different company; Yahoo; AppNexus

- Perfect Audience experiences a much quicker cash turn than our core SharpSpring business. Processing higher volume, lower fee transactions

- estimate that the lifetime value of a Perfect Audience customer could be around $1,500

- believe we’re acquiring customers for about $475

- payback period on those dollars is just a couple of months, which allows us to recycle those invested dollars at very high velocity

- been steadily building this product into SharpSpring and believe it will offer us some real cross-selling and upselling potential

- Sharpspring integration focus has really been about making significant changes in the customer acquisition process and working to increase lifetime value by helping customers better spend our budget through look-alike audiences

- use it to drive quality leads into the top of the funnel

- June was the single highest revenue month since the acquisition

Q2 20 CC

- 276 new customer wins we secured during the period represent approximately $2.2 million in annual recurring revenue

- approximately 2,000 agency customers and over 500 direct customers and over 8,500 total businesses

- CAC up due to COVID: cost to acquire customer was approximately $10,900, which was a sequential increase from $9,800 recorded during the first quarter of 2020

- this quarter’s CAC calculation artificially reflected pre-COVID-19 sales and marketing spend as a numerator and COVID-19 adjusted new deal closing as a denominator

- our marketing spend is down considerably in Q2, but we’re still expecting to see similar sales levels going forward, which should lead to significantly lower CAC next quarter and beyond

- Q2 2020 net revenue retention was 91.6%. On a monthly basis, second quarter 2020 average net revenue retention was 97.6%

- firmly believe that we will see a point in our relatively near future where we hit a 100% revenue retention

- reduced expenses due to COVID: deliberately reduced our expense budget based by nearly 20%, which is expected to create significant cost savings for the remainder of 2020, and should also allow us to meet our target cash usage for the year of approximately $4.8 million

- put some austerity measures for lack of a better term in place as the pandemic hit

- Most of the changes that we put in place, we believe, to be permanent changes

- did do a salary reduction

- asked people to take a 10% reduction in salary

- During the first half of the year, we spent approximately $3.5 million of our $4.8 million 2020 full year projection

- expects total revenues between $29.5 million and $30.5 million, which would represent an increase of approximately 32% compared to the prior year – some of this growth is from Perfect Audience though

- range of total revenue is driven in large part by our Perfect Audience revenue through the second half of the year

- recorded a 38% increase in the number of paid advertisers compared to the first quarter of 2020

- actually sold, I want to say the number is 2 or 3 more agency partners than we did last year

- 80% of the businesses that we sold in Q2 were agencies and then that, of course, is where the 10 packs came from.

- seen agency client expansion slow down

- not seeing agency clients leave agencies very much at all

- many other players in the space are experiencing major drops in the advertising revenue

- as the economic conditions improve, we’ll see greater acceleration of the business

- as the low-cost provider in the space, we are also insulated from companies seeking to lower cost by switching to more cost-effective solutions.

- introduced a new pricing option for larger agencies that allows new customers to buy more licenses upfront at a nominal discount in exchange for an annual commitment

- saw strong interest in this new option from larger agencies and sold a total of 10 bundled, $1,500, 10 pack licenses, one of which was actually a 40 pack.

- in addition to signing up at a much higher initial MRR point from, typically what is a $600 sign up starting out at $1,500, in addition to that, they are on an annual contract. So these are customers that are not only paying us more MRR, but are more stable customers and more committed to putting a lot of clients on the platform

- these larger clients that takes a 10 pack and you’re getting the $1,500 kind of as it is

- would then be charging for expansion licenses I believe it’s $275 million for an additional license after the 10 pack

- these are larger customers that believe that their 10 pack is just the start

- new agency customers were actually up year-over-year for the second quarter.

- larger deals resulted in a 10% increase in ARR from $2 million in Q2 of 2019, to $2.2 million in Q2 of 2020

- Chip House would be joining SharpSpring as our new Chief Marketing Officer

- credentials at high-growth SaaS operations

- was the first marketing executive at Exact target and early SaaS pioneer

- also led marketing efforts for e-commerce provider, Digital River

Springboard

- our new engagement platform, which we’re calling SpringBoard

- products have become so powerful that most customers only use 20% or 25% of the entire tool set

- proactively building an in-app engagement tool called SpringBoard that is designed to provide a customized plan to a user, enabling an agency or their client to know precisely what to do? Why to do it? And when to do it?

- SpringBoard’s unique value proposition is that it doesn’t just teach a user how to use the platform, but acts as a business’ own strategy consultant advising you on how to extract the most value from the platform.

- customized stats to show a promise land

- concrete tailored guidance on how to get there

- gamified the process to track progress and unlock certification and merchandise rewards

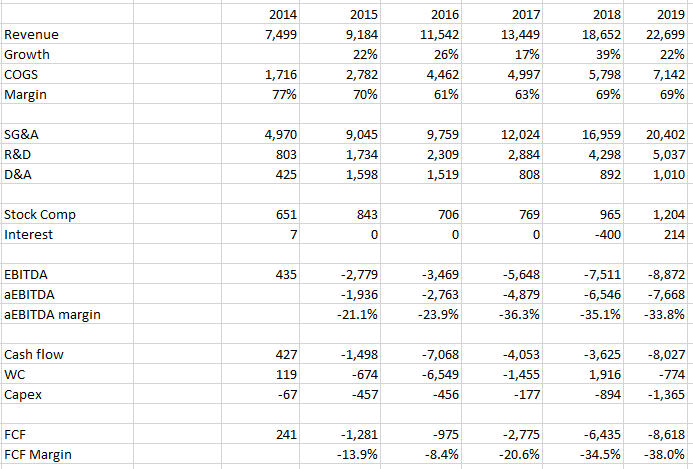

Longer-term Financials:

Recent Financials

Recent Financials

No comments yet