Research: HubSpot

I primarily started looking at HubSpot to compare them to SharpSpring. I spent a bunch of time going over youtube demos of their product. Its fine, it looks clean and easy to use. It doesn’t blow me away to be honest. Its like a lot of these SaaS products. I read the WallStreet research and you’d think these companies are changing the world. Then I step through the demos and its like ehh, ok. I mean I worked in software 10 years, this stuff isn’t rocket science. But whatevs.

The bigger, more interesting thing I found is at the end of the post. I bolded it. I’ll do another post later because after noticing this with HubSpot I dug into a bunch of other SaaS names and drew the same conclusion. But just as a teaser to that, since HubSpot is where I really clued into what seems to be going on, check out the chart at the end of the post showing how HubSpot stock has moved and just how much analyst estimates have changed since the beginning of the year. Its crazy. We’re told how these software businesses are booming. Are they? Or are the stocks booming and the software businesses are doing fine, but nothing really any better than they were when the stocks were 50% lower. There are exceptions like Zoom or Shopify but most are not.

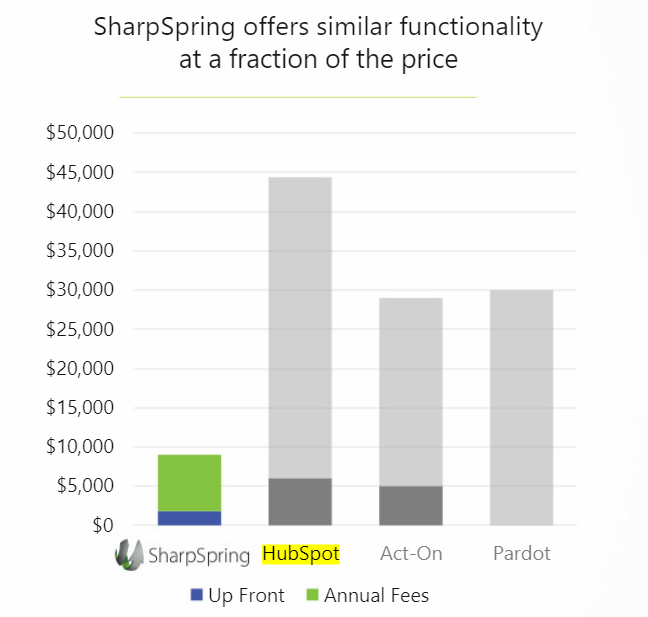

Just as a short conclusion: I’d say the HubSpot product looks better than the SharpSpring one. You watch the SharpSpring demos against the HubSpot demos and its not quite as clean, things are labeled a little clunky here and there, not as much functionality, and you can see how the workflow isn’t as slick. But on the other hand, SharpSpring is like 1/5th the price. From what I can tell its not 1/5 of the package. I can see why SharpSpring has a easier time getting the agency business. These are customers that I imagine already know what they are doing. They know marketing. They do this for a living. So they know what they want and SharpSpring delivers that functionality at a fraction of the price. Maybe if you don’t know what you are doing and you need some hand holding or want specific customization to your business then HubSpot is going to be better – I mean it really seems like a more intuitive, better package. But again, its not that much better. At least from what I can tell.

General

General

- $12.5b market cap – stock is at $284 right now

- $1.13b of cash

- $467mm of debt

- trades at 14x P/S

- grew 25% yoy in Q220

- ranked #1 company to work for on Glassdoor

- their annual event that SharpSpring mentions is called Inbound – 26k registrants in 2019

Customers

- leader in smaller businesses

- focus has been small business (organizations less than 2,000 people)

- could cause elevated churn though

- have 25k customers that are 2-20 employees – this segment grew 150% yoy

- enterprise with 200-2000+ employees has 8k customers

- 25k customers that have multi-products

- total of about 68k customers

- because they are targeting small busines, their TAM is 100s of millions of businesses)

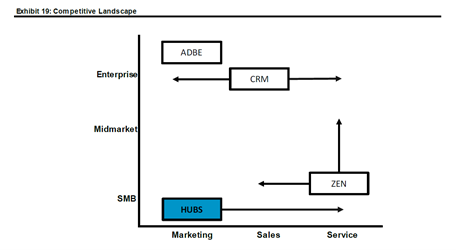

Competition

- they have avoided competition by focusing on smaller end of midmarket

- they don’t even mention SHSP as competition:

Product

- began as an app, becoming a platform

- Marketing Hub is oldest product

- Marketing Hub puts all of the marketing activities/campaigns in one spot, accessible to sales and marketing depts

- CRM – contacts tab

- contacts page, list contacts, filter contacts

- conversations

- support emails

- chat logs

- creating email/conversation templates

- marketing

- this is a good video explaining the product https://www.youtube.com/watch?v=sxOibuTUGjQ

- ads – can connect google/facebook ads, track engagement

- email – create marketing emails, set up, automate and schedule marketing emails, analyze success of email campaigns based on open rates, click rates

- social – link all social media accounts in one spot, schedule SM posts, monitor activity

- website – create static websites in your domain (home page, contact), landing pages for inbound marketing – to download content, fill forms, blog pages – has things like templates for landing pages, web pages, its actually a little web page creation tool, geared to creating CTA pages

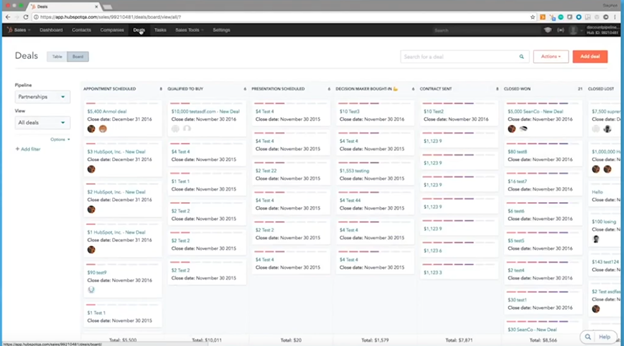

- sales – this is in large part their CRM platform

- deals – set up a deal flow, appts, proposals stored, who decision makers are

- tasks – lists of sales tasks assigned to you

- documents – hub for finding documents, also shows stats around document usage/views

- meetings – set up your sales meetings, connect to Google or Office 365 calendar

- here is what the deals page looks like:

- service:

- tickets are listed

- service hub dropdowns

- automated:

- workflows – automated workflows for your organization, example I watched of an email nurturing sequence, sending sequence of emails of a contact that has shown interest via some form they filled out – fill out triggers of the automation, the emails you want sent out, timing of those emails, etc

- sequences – stuff like send an email, call two days later, sequence of followup events

- this was a good video describing: https://www.youtube.com/watch?v=sIEnM0YyM5M&t=444s

- reports:

- see traffic analytics

- performance of ad campaigns

- CRM

- I’m not sure if HubSpot integrates with other CRMs or if you have to use their CRM

- tracks contact management

- deal and task management

- interactions with social and email to track leads

- good video demo: https://www.youtube.com/watch?v=zv2QXavTvH0

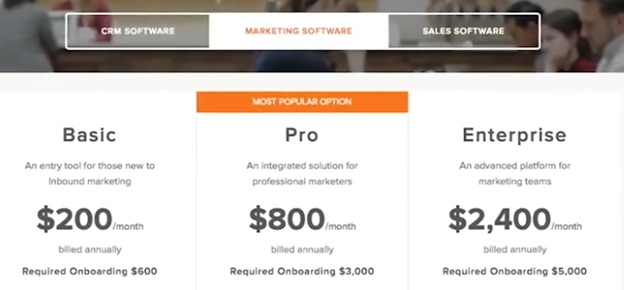

- pricing:

- the CRM software is free

- was originally a tool for SMB – a simple platform to track marketing campaigns

- originally built around inbound marketing – also called content marketing

- offer a free CRM product, cheap starter for marketing, sales, service hub:

- between the three hubs:

- Marketing hub – $530mm of ARR, growing low-mid 20%s yoy

- Sales Hub – $100mm ARR, growing 100% yoy

- Service Hub – $14mm ARR, up 5x from ~$2m a year ago

Growth

- a few years ago they changed go-to-market by embracing free CRM

- their growth has been primary a function of customer count

- ARPC has been declining

- ARPC metric is a bit deceptive – enterprise spend per customer is increasing, starter products are bringing down overall spend per customer

- Marketing Hub growing at 5% yoy if you exclude the starter product

- Sales Hub growing at 31% yoy

- international revenue has expanded faster – 60% CAGR over last 5 years

- fcf margins are ~10% and growing:

- more evidence that their growth is based on sub adds. Their retention rates are not that high, hovering around 100%

- revenue in the US is slowing a little – was 26% in Q319

- core marketing ARR is in low-mid 20s

- these were the Wells Fargo numbers heading into Q419:

- whats interesting is that the FY20 average estimates are essentially the same as that, actually a little less on EPS:

Q2 Results

- had set a low bar

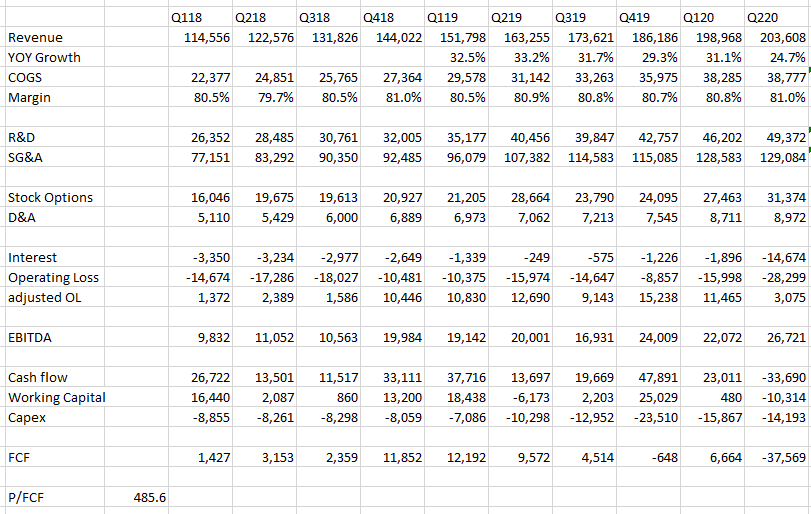

- revenue was up 25% to $204mm – this compares to 31% yoy growth in Q120 and 33% yoy growth in Q219

- positive surprise on customer acquisitions

- they had lowered the price of their Starter Suite by 2/3 in Q120 which drove growth in customers

- total customers grew 34% – 7,896 new adds vs 4-5k new adds last quarters

- the promotion could lower revenue growth over next 12 months – it is extended to Q320

- billings was up 20% yoy

- there was 400% increase in suites install base – due to free user upgrades and new businesses moving online

- avg sub revenue per customer was down 5% yoy though

- guidance of 23% revenue increase – up from 19% before – $210.5mm at midpoint

- here’s the funny thing about Hubspot, while the stock has shot up to new highs, its not really based on any increase in estimates, estimates went down and then came back up again and are basically still below where they were:

- So really take a look at this chart. This chart is not just showing 2020. Its showing 2021 and 2022 estimates as well. So we are looking at changes to analyst revenue forecasts for next year and the year after. And, um, they have hardly changed. This is the big “pull forward” in software adoption? Really? Because it looks pretty damn flat to me. The stock is up a ton. But the forecasts – not so much.

- their poor cash flow in Q220 is kind of weird – everything yoy on the income statement looks comparable to Q219 but for some reason they burned through $23mm of cash before working capital.

- the only thing I see on the cash flow statement is this repayment of convertible:

- I wonder if that shouldn’t really be subtracted as an operating activity?

- Its really strange to me that Q220 cash flow was as bad as it was given results are basically similar yoy (and they are growing of course)

- what strikes me as well is that in the last 5 years their top line has grown 6x but really their EBITDA loss has only shrunk like by like $25mm. And if you want to argue that its because of the sub-growth – that MS argument that growth is masking true profitability, then why don’t we see EBITDA improvement accelerating as their growth rate goes from 57% down to 32%