I am so annoyed with myself for not buying into this one sooner. It has been on my radar since July and for some reason I kept putting off looking at it in detail until they released earnings today. Their Silvergate Exchange Network (for digital currency clients) is acquiring customers at a faster rate, the resulting growth in NII is great and while its not the cheapest bank in the world at ~1.5x book after today’s pop, it is not ridiculous given how they have positioned themselves. Oh well, better late than never – argh.

market cap of $386mm (Friday close)

book value of $277mm – trades at 1.4x book

Operate Silvergate Exchange Network

proprietary, virtually instantaneous payment network for participants in the digital currency industry

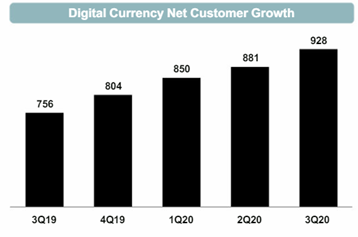

saw 68,361 transactions, volume of $36.7b – this is up 70% and 65% over Q220

Digital currency fee income of $3.3mm – up 36% compared to Q220

say they have over 200 prospective digital currency customers

Digital currency deposits grew by $586mm to $2.1b in quarter – most of their deposits are digital curency, about 90%

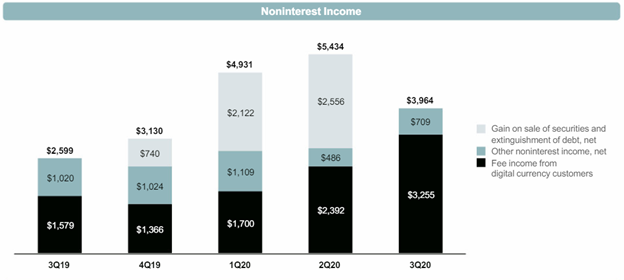

overall NII was down but that was because of no GOS:

their fee income is exploding

consider that net income for the quarter was $7mm and they had fee income from digital currencies of $3.2mm and that is increasing at $1mm per quarter right now

meanwhile their non-interest expense barely moved, up about $150k qoq

ROA was 1.13% in the quarter, ROE was 10.14% – these seem like decent numbers even if you are buying it at 1.5x book

these guys were founded out of Callinan mines, which discovered 777 mine

targeting VMS deposits

two mining districts Bathhurst and Flin Flon, also have a property in NFLD – Bichans district

Even though I talk Bathhurst first, its the Flin Flon property that is the interesting one:

Bathhurst – New Brunswick

3 properties: Nash, Headway, Superjack

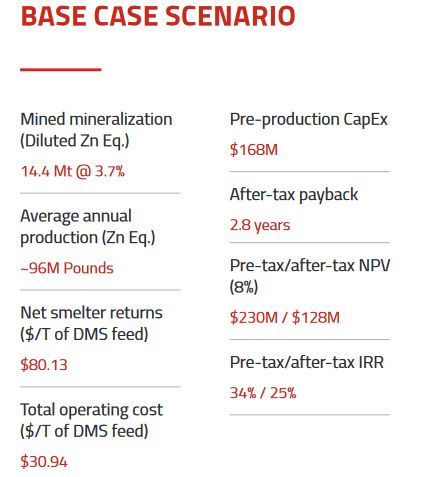

they have a PEA at Nash Creek

10 year 3,900 tpd open pit mine

963 million lbs of Zn Eq

would use existing Brunswick smelter

it wasn’t a huge mine, but not terrible either:

unfortunately it looks like it is a Zn/Pb deposit which isn’t super exciting

from what I can tell zinc is going to be in surplus for a while

but latest results seem to be finding silver

NC 20-313 intersected 28.6m of 57 g/t silver at a vertical depth of 120m including 16.5m of 94 g/t silver and NC19-306 which intersected 19m of 36.53 g/t silver, 0.52% lead and 0.38% zinc at a starting depth of 34m

the silver could be on to something but who knows

overall I’d give this project an – “ehh”

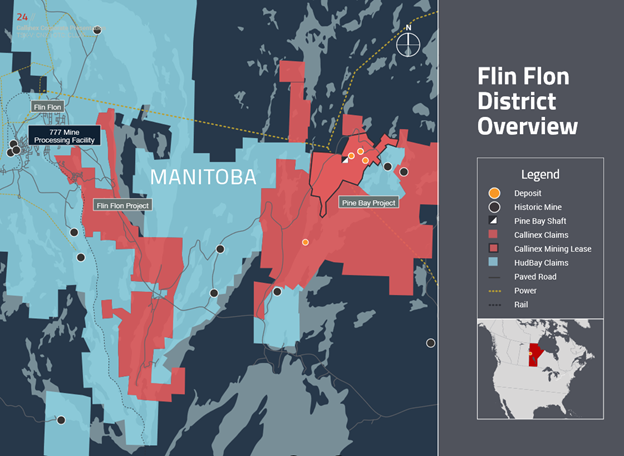

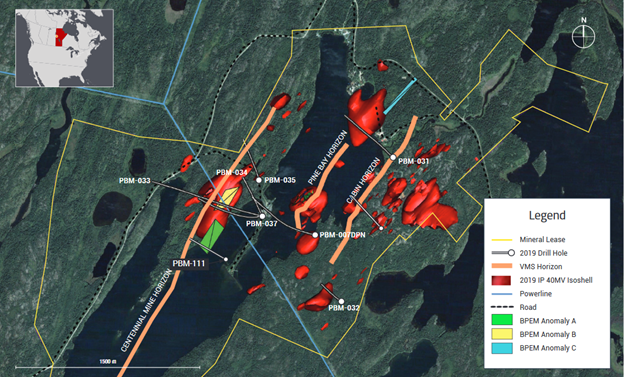

Flin Flon

right around historic mines

Callinex claims are right around the Hudbay 777 mine – they are maybe 10km to the east of Flin Flon

just like generally, it is kinda crazy that a $30mm company has this much land leased right around Flin Flon:

they call recent discovery Rainbow – it is at Pine Bay project (to the east)

targeting 3 anomolies they’ve found:

within a larger VMS corridor with a number of other mines

in Sept announced some high-grade but narrow intercepts:

So that doesn’t look that interesting, pretty narrow, who cares right?

but this is interesting:

the geology suggests something much bigger – they cut across a 260m by 600m anomoly

this walk-through of the Rainbow discovery is pretty interesting, look at the anomaly and where the drill intercepts went: https://vrify.com/embed/decks/9497

It really looks like they sliced across something that potentially could be very big

new release Tuesday that they have drilled two more holes 112 and 113 and they both have hit on something – going to lab and will know more with results then

113 is right into the anomoly, 112 is above anomoly but into massive sulphide core

We should have results on these two holes in the next couple of weeks

So basically, they are in elephant country, they just sliced across something that looks like an elephant

One more thing, after they released the news that they sliced across something that looks like an elephant, the CEO went and bought a bunch more shares at a 52 week high:

I don’t talk exploration stories much on the blog because I usually get them from newsletters and so they aren’t my original ideas. But this one I found from the insider buys and it seems interesting enough to take a position. But these next two holes could miss and the stock could tank, so high risk. The drilling so far caught my attention and just the idea that this dinky little venture company has such a big land package right around Flin Flon and surrounded by Hudbay claims.

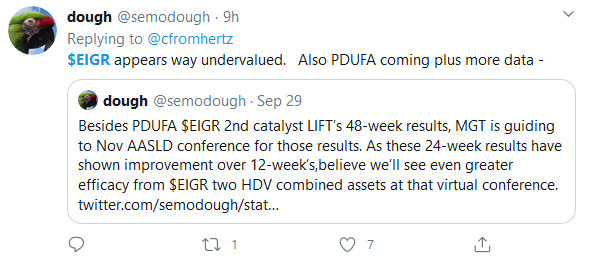

I’ve owned Eiger for a while. I bought more when they announced their first (disappointing I guess) COVID results in mid-September and the stock tanked. It was silly because this isn’t a COVID stock. But then the second set of results came out today from a COVID study in Toronto and they look very good (see end of post tweets from biotech twitter). I don’t know why the stock wasn’t up more today, given where others go when good COVID results come out. I bought even more today when it was in mid-$9s. Its still below where it was a couple months ago and again, COVID isn’t the main feature here. Notes below and COVID notes at the end.

Market cap of $300mm

$60mm of cash

here is what they are targeting:

going after rate and ultra-rare diseases

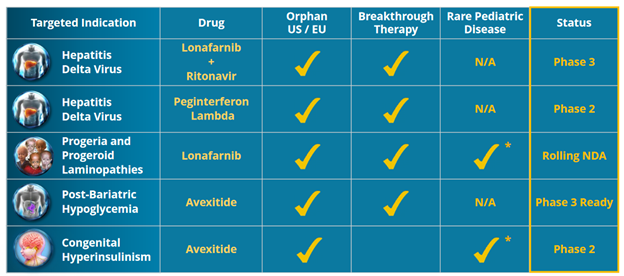

3 drug candidates: Lonafarnib, interferon Lambda, Avexitide – but really the story is about Lonafarnib and Lambda and the Phase 3 studies respectively

They’ve kinda repositioned their investor presentation from being “rare diseases” to being HDV leader – so its all about Lonafarnib and Lambda

they are a leader in HDV – Hepatitis Delta Virus

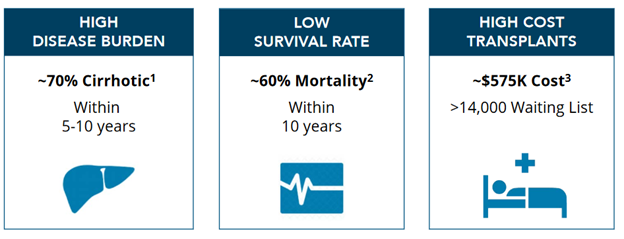

most severe form of hepatitis

4-6% of HBV patients co-invected with HDV

No FDA approved Rx

15mm to 20mm patients worldwide – orphan market in US is >100,000, in West EU is >200,000

HDV advances much faster than other forms

HDV is very expensive to care for:

targeting with interferon-lambda to reduce HDV-RNA and Lonafarnib

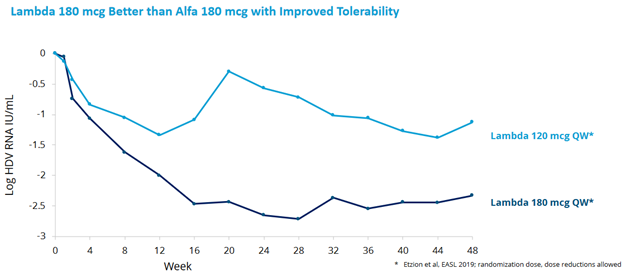

Lambda

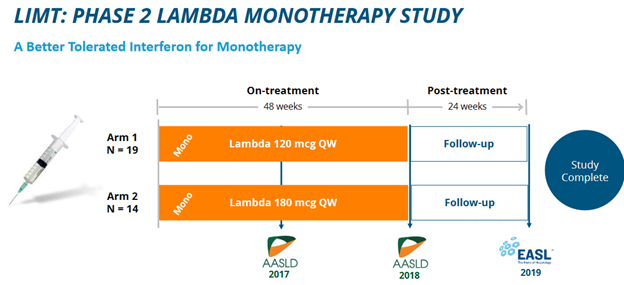

LIMT was their Phase 2 Interferon-lambda study:

results were good for the 180mg dose:

Lambda on track for approval in next 2-3 years

Phase 3 study will have 48 week treatment, 24 week post-treatment

single 180mg dose, looks like design of trial uses Lambda in both wings, just delays by 13 weeks in the one, then compares the 13 week non-use cohort with the end point of the Lambda patients – kinda odd

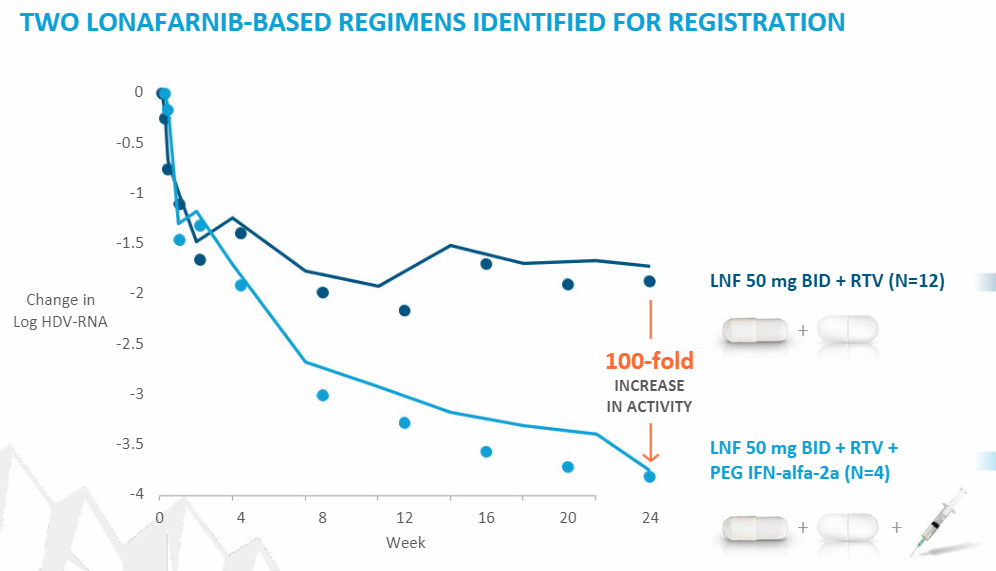

Ionafarnib

completed NDA submission for lonafarnib for the treatment of Progeria and Progeroid Laminopathies.

FDA previously granted Breakthrough Therapy Designation and Rare Pediatric Disease Designation to lonafarnib, which enables eligibility for Priority Review, if relevant criteria are met. Eiger expects to hear from the agency regarding submission acceptance and Priority Review within 60 days.

Lonafarnib licensed from Merck

with Lonafarnib – dosing was figured out in Phase 2

response in Phase 2:

but what they seem to have found with Lonafarnib is it works best in combo with Ritonavir and IFN-alfa

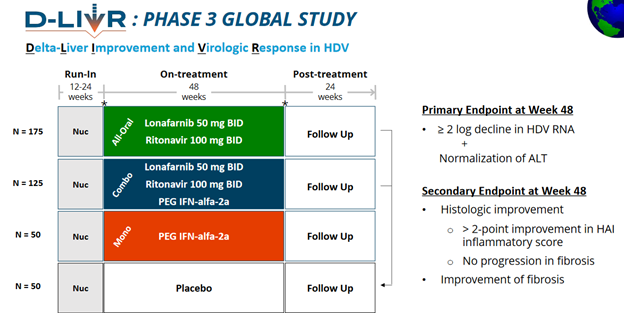

Now onto phase 3 study

the phase 3 has 3 wings, one with the 3-combo, one with 2-combo, one with just IFN-alfa

expect to complete enrollment in 2021

48 week treatment, 24 week post-treatment

Lambda for COVID

multiple studies in parallel

looks like 6 studies in total

Toronto, Stanford, Israel, Boston, NY, Baltimore

First Study

this study looked at use in mild covid – “in outpatients with mild and uncomplicated COVID-19”

A total of 120 patients were randomized 1:1 to a single subcutaneous dose of Lambda or normal saline placebo. Patients were followed for 28 days.

this study was reported Sept 28:

The primary endpoint was duration of viral shedding, determined by time to first of two consecutive negative tests for SARS-CoV-2 by qRT-PCR. The secondary endpoint was reducing duration of symptoms and hospitalization in patients with mild COVID-19.

No difference was demonstrated in duration of SARS-CoV-2 viral shedding and time to symptom resolution when compared with placebo. Median time to cessation of viral shedding in both groups was 7 days. Lambda was well-tolerated with few adverse events, which included elevated transaminases which self-resolved.

this isn’t really surprising, as they said “”We now know that untreated patients with mild COVID-19 clear virus quickly. Published reports have demonstrated evidence of a therapeutic benefit of interferons in hospitalized patients with more advanced COVID-19 disease,”

Second study reported Oct 15

mild to moderate covid

said “total of 60 patients were randomized 1:1 to a single subcutaneous dose of Lambda 180 mcg or normal saline placebo. Patients were followed for 14 days.”

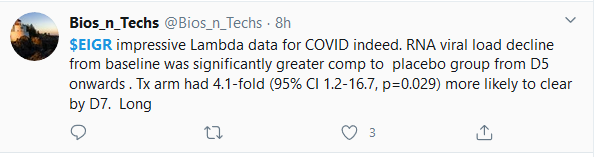

these are the results, seem significant:

SARS-CoV-2 RNA viral load decline from baseline was significantly greater in the Lambda group than in the placebo group from Day 5 onwards. After controlling for baseline viral load, those treated with Lambda were 4.1-fold (95% CI 1.2-16.7, p=0.029) more likely to clear by Day 7 than those in the placebo arm. For those with baseline viral load > 6 log copies/mL, the proportion negative at Day 7 in the Lambda group was 15 of 19 (79%) compared to 6 of 16 (38%) in the placebo group (p=0.013). This difference translated into a median time to clearance of 7 days with Lambda compared to 10 days in the placebo group (p=0.038).

also this: Lambda works particularly well in patients with high baseline viral loads

CLIQ news out today looks solid. Sales accelerated a bit in Q320 over Q2. I think it is only going to improve with the trajectory of cases we are seeing in Western Canada and the restrictions just put in place in Edmonton.

Oct Update

selling 8 stores for $21mm – $2.625mm

these stores contributed $1.9mm of profit in 2019

lower volume stores – though they were profitable ones

SSS for liquor accelerated to 15% yoy – was 13.4% yoy in Q220

Cannabis SSS increased 33% which is decent as well

said available capital resources is $70mm so that is down from August but that probably means increased inventory which could be a good thing