Research: SharpSpring’s Investor Day

SharpSpring has really taken off these last couple weeks. I would attribute the strength to:

- Everything is going up

- Q3 was quite good especially the underlying metrics

- Investors are starting to warm up to them (esp. the unconventional customer acquisition model they have)

With respect to (3), I noticed that there is a SumZero post on SharpSpring.

I can’t access SumZero, but the fact someone, likely a fund, is pushing them is a positive.

SharpSpring held an investor day this week. On it they described their business and their long-term model. They admitted that one of their challenges is explaining why their model works when it appears on the surface that it should not.

I still like the stock (I’m still holding), but I have to admit it remains hard for me to wrap my head around how I should think about the comps with other SaaS names. It is such a different SaaS model.

Carlson (SharpSpring’s CEO) described it pretty clearly on the call this week:

One of the — probably one of the most confusing things about our business or concerning things to an outside investor who doesn’t understand how our business works is our logo churn. On a monthly basis, we’re hovering around 3% logo churn. That’s often a problem for SaaS businesses

As I have learned more about SaaS businesses, I have come to appreciate that one of the primary tenants is that “churn is bad”.

Because SharpSpring violates this tenant with prejudice, one would expect it to weigh heavily on the stock (and until very recently, it likely did).

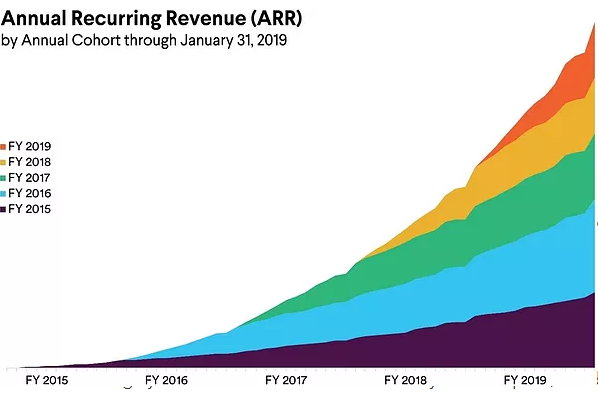

To put it in stark, comparative terms, consider the following ARR by cohort chart from the Slack S-1 (from January 2019):

See how there is a the nice, up-sloping curve to each of the cohorts, thereby illustrating the revenue expansion of existing customers that more than makes up for any churn.

Now look at SharpSpring:

The slope is ominously down and to the right.

But here’s the thing. That churn does not seem to matter.

SharpSpring customers have a lifetime value (LTV) of $59k. Their cost to acquire customers (CAC) is $7.5k. So their LTV/CAC, which is what really matters, is 8x.

That isn’t as good as Slack’s (which was ~12x in January 2019) but it is much better than most.

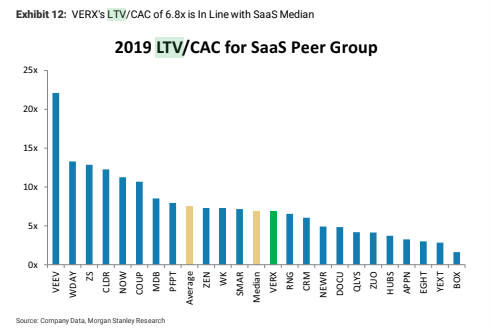

Consider the following Morgan Stanley peer group comp of LTV/CAC:

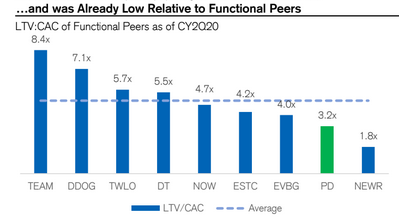

And consider this, more recent LTV/CAC peer group comp, taken from the Credit Suisse Initiation report on PagerDuty:

Now look at Hubspot, the competition. Hubspot only has an LTV/CAC of 5x, and this is a competitor that trades at about 3x the valuation of SharpSpring even after the big move we’ve seen in the stock (the following is from Morgan Stanley):

Even though SharpSpring churns through customers like a grass fire, the combination of A. having some very high value customers that stay on and B. not spending very much to acquire them, seems to outweigh that, and it leads to unit economics that are actually very good.

So good in fact, that the push is on from analysts for SharpSpring to spend more and grow faster. This was something else they addressed on the call.

If SharpSpring decides to step on the growth pedal, it will be interesting to see how it goes. The possible Achilles heel of their model (it would seem to me), is that they are running through their addressable market faster than most would, because so many are churning. So I wonder if that addressable market may not be so big?

But maybe that is not the case. The customer acquisition pipe that they use is via digital marketing agencies, who partner with SharpSpring and then acquire SharpSpring users on their behalf. According to what Carlson said in the investor day, there are 60,000+ digital marketing agencies in North America and Europe and SharpSpring currently has about 2,000. So there are still a lot of customers to churn through.

Anyway, I’m glad the market is starting to see what I thought I saw with the stock. I just wish I could see it a bit more clearly myself.

Here are the rest of my notes:

- talk about net revenue retention and how the maturity of customers is important, how because they are a relatively new company, they don’t have the mature customer base, or are just getting it

- “power” of their business is lost when you average the more mature cohorts and the newer ones

- the new customers are holding down the ARR numbers – and if they grow faster, the weight on ARR is bigger

- have penetrated 2,000 of 60,000 digital marketing agencies – around the same as Hubspot

- they think longer term they can get to 80% gross margins and 20% operating margins

- customer LTV is $59k while CAC is $7.5k – so 8x

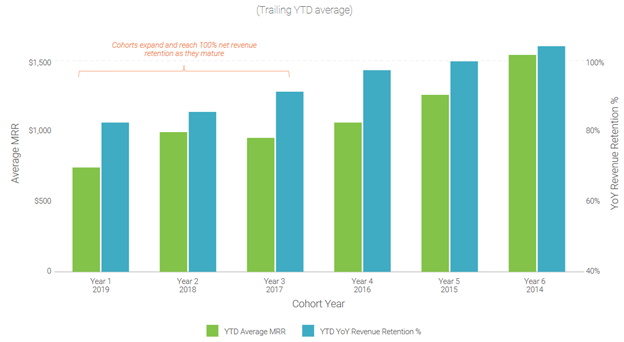

- older cohorts – 4+ years, are above 100% revenue retention:

- move from 5-pack of licenses to start to 3-pack has reduced time to get expansion revenue

- their agency customers provide tier 1 support – once they are onboarded with clients, support the agencies require to provide this is not a lot

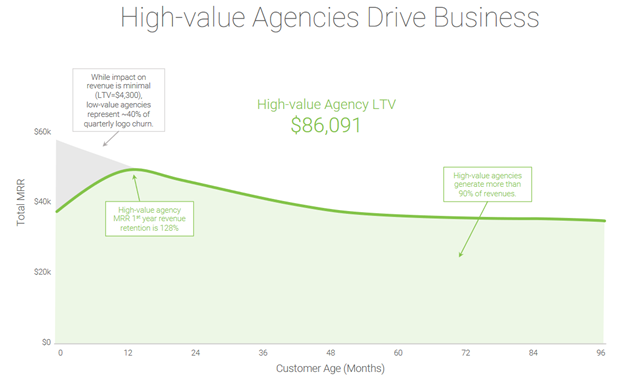

- this is the key slide I think – it shows the early attrition of the 40% of “low value” agencies and the high-value and rapidly increasing MRR of the high-value agencies:

- the cohort that they signed 6 years ago is paying 70% of MRR 6.5 years later – so even with the attrition, the remaining make up for it quite a bit

- just purely looking at high-value agencies – the LTV is $86k and the CAC is $9.300 so its 9.2x

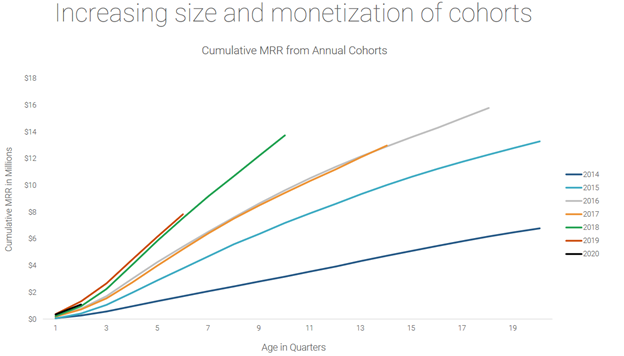

- in more recent years, the MRR of new customers has been rising:

- they are also seeing new customers spend more quickly

- far cheaper platform than competition:

- with only one exception companies they compete with today are same ones they competed with 8 years ago – the one new entry is ActiveCampaign, but it is an old company that entered space more recently

- in one of the questions they imply they might be willing to invest more, grow faster, accept a lower LTV/CAC to get that growth

- before COVID their expectation was to hit high-40%s growth rate in 2020

- you can see looking at the older cohorts that revenue retention jumps in Year 2 and then it does shrink, so there is attrition after year 2:

- but after year 3 it seems to flatten out – which is basically what they were saying – revenue retention flattens at around the same level it started out at

- Also worth pointing out that the 2021 number implicit in the chart is only 21% growth – that is okay but not stellar

Greenhaven Road has had a position for a while and Scott Miller (the PM) worked his way onto their board last year. In his “value investing” circle, he’s been somewhat vocal about SHSP, he’s also on SumZero: http://www.greenhavenroad.com/investor-letters/. So that may be the fund you’re suspecting.

Also, Miller managed to get Savneet Singh onto the board as well. Savneet is the CEO of Par Technology, another company that is getting some love in the saas-can-be-value camp lately. I don’t know too much about him other than he has a healthy respect for Buffett, I’m planning on listening to a podcast interview with him soon. He may very well be worthy of the man crush numerous managers seem to have on him.

Thanks for the SHSP writeup, it’s been a holding of mine that I’ve wanted a better understanding of.

Thanks for that info. It fills in a blank as to why the stock has been soaring and also why there seem to be a couple of anonymous twitter accounts popping up – one with the sole purpose, it seems, of bashing the stock. When I see that sort of thing i always start wondering what is going on in the background. But if the stock is getting some higher profile names onboard, there is bound to be push back I guess. I still struggle a little with the model though, so I don’t totally discount the shorts here.