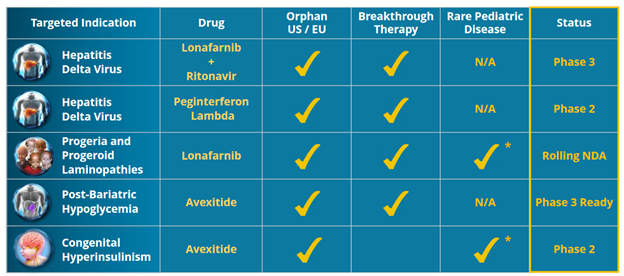

Eiger Approval

Eiger’s Lonafarnib was approved for the ultra-rare disease Progeria on Friday night.

Progeria sounds like a terrible disease that previously had no approved treatment. It is great to see that now there is at least some option available.

I’m not expecting a big move up in the stock, but we may see weakness (“sell the news” is sort of EIGR’s MO and if short term traders are disappointed they may pile on) and that could be an opportunity.

Expectations of approval were already very high. This was more of a downside risk scenario – if the approval had not happened the stock would have been whacked.

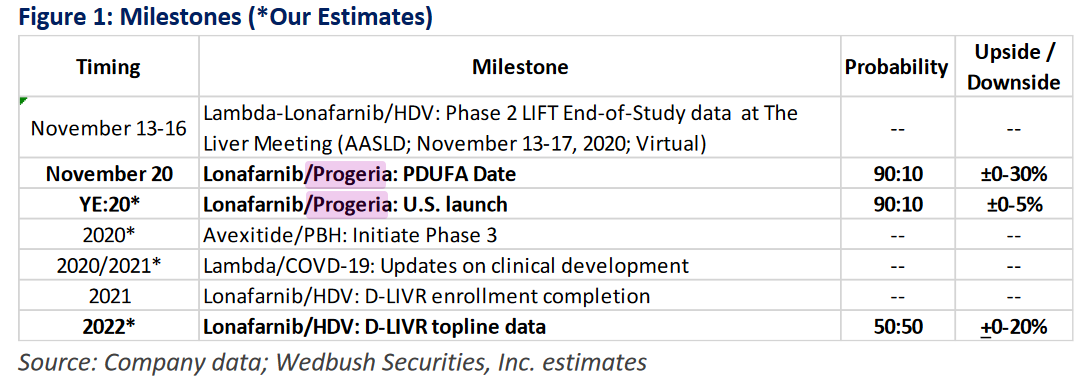

Wedbush had estimated probability of approval at 90% and did not assign any upside if the approval happened:

So it is not a big positive. But the approval does have some value to Eiger.

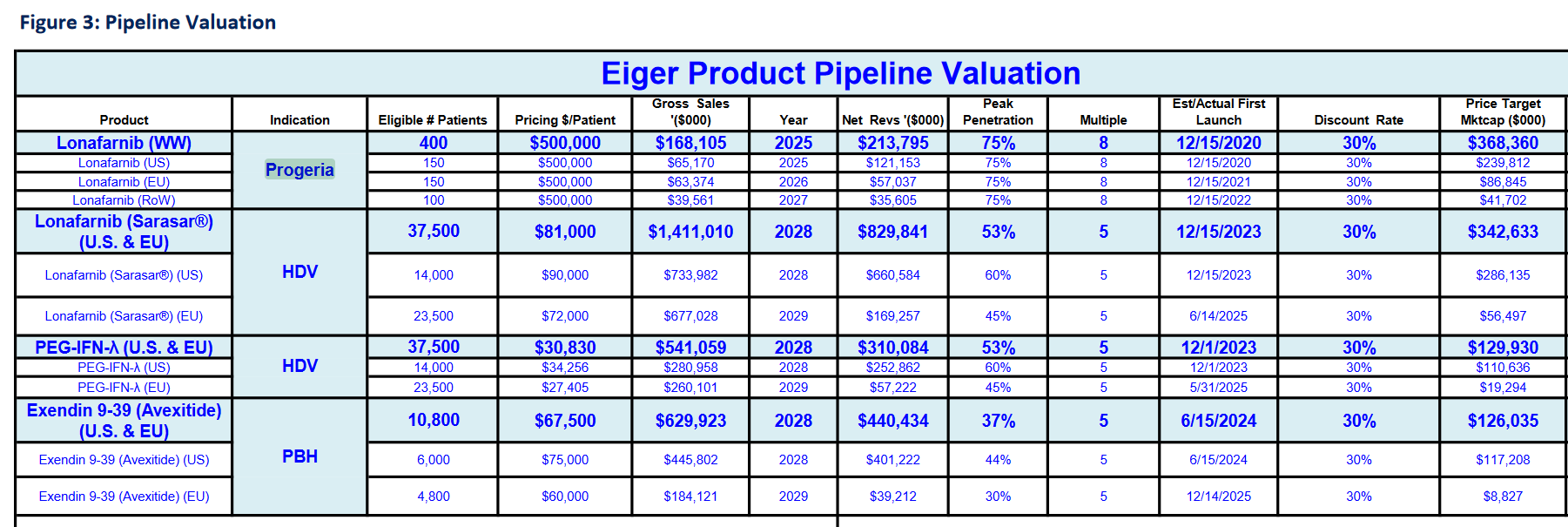

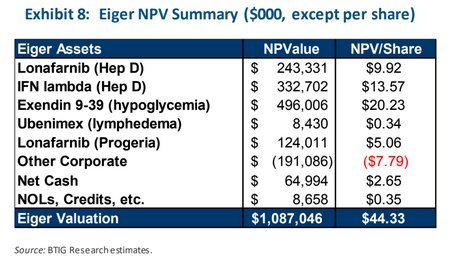

To be honest, I was surprised by the assessment of Wedbush and BTIG on the value of an approval (below). They assign more value to Progeria than I would have thought.

Wedbush estimates a market value of $368 million to Eiger.

BTIG assigns a $124 million NPV.

Eiger has said in the past that revenue won’t be a lot. The disease is just too rare. So I am a little skeptical of the numbers from BTIG and Wedbush. $368 million would be more than the current market cap. I don’t think the market will see it that way.

The more certain cash infusion comes from the other announcement last night. With the rare disease approval, Eiger also received something called a Pediatric Disease Priority Review Voucher (PRV).

A PRV can be redeemed for a priority review by the FDA of another product.

What makes the PRV particularly useful is that you can sell it. Eiger can auction it off to another company that it would be more valuable to.

From what I can see, these PRVs are worth around $80-$100 million.

As part of their agreement with the Progeria Research Foundation, which is the group they ran the trials with, Eiger splits the proceeds of a PRV sale with them.

So Eiger stands to net $40-$50 million from the sale of the PRV.

Eiger has cash of $60 million right now. So the PRV puts them over $100 million.

That should be enough to carry them through the other trials in progress (for HDV and PBH, as well as COVID), without having to raise capital.

The market cap of the stock is about $300 million. What I like about Eiger, what makes it the only biotech that I am willing to hold through approval events like Friday, is that there are just so many late stage shots on goal.

I will keep holding this one and add if the market gets silly about it again.