A Sign of Life from the Shipping Trade?

I have been in the shipping trade for about 4 weeks now. Up until today it has not really worked.

The stocks have bounced around. I have made a little on ESEA and GRIN, lost a little on NMM and SBLK and done nothing at all with DAC. Overall, I have been flat.

I was beginning to doubt the idea. It was the usual doubt – sure the stocks seem very cheap, but maybe the market just won’t care?

There are plenty of reason for the market not to care. For one, these stocks are well off their lows of last year. For two, the shipping business is terrible, self-serving and full of management teams that have a history of incinerating cash. For three, rates are at decade highs and why get in at the top?

FWIW there are really two separate ideas here. There is a containership trade and a dry bulk trade. They have pretty different dynamics, so you need to talk about them separately.

The containership trade is the more immediate of the two. The shortages in containerships is happening now.

Containership rates are off the chart. They are at (I believe) all-time highs.

The first question that comes up when you see this chart is whether this is just a blip due to the pandemic.

To some extent that seems to be true. We have the restocking of inventory at the same time as post-pandemic demand in the United States is sky-high. There are also shutdowns at at least one very large port in China because of a COVID outbreak.

But if this was just a blip, what you would expect to see are very high spot rates and much lower two, three and four year charters.

But that is not what is happening. Containership owners are booking long-dated charters at huge rates.

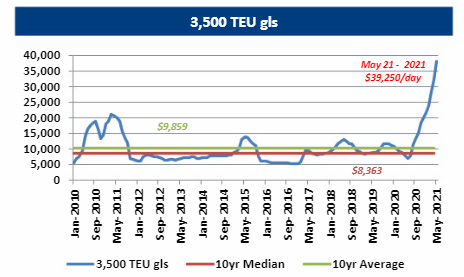

Just to give one example. A 3.8k TEU containership (a TEU is one of those big cargo containers that stuff gets shipped in) was booked last week for 5 years at $35,000 per day to CMA CGM.

A 3.8K TEU is a Panamax size (Panamax is between 3-5k TEU). This chart is from the Euroseas Investor Presentation:

3,500 TEU shipping rates have not been above $10K per day for years. And yet now there are customers willing to book them out for 5-years at $35K per day?

This makes me stand up and take notice. It does not look like a blip to me.

Yet the market is trading these stocks at levels that is saying it is just a blip.

I mentioned the Euroseas analyst estimates in my last post. Average estimates (albeit this is from the only two brokerages that cover them) are $6.50 per share EPS for 2022. That means the stock has been trading at a little over 2x earnings. This would make some sense (but not a lot in my opinion) if spot rates were sky high but long-term rates were much lower. But it makes no sense when ships are booking 5 years at $35K.

The only gotcha in the idea is that the order book has ticked up. And we know we can’t trust containership owners to make sensible decisions. These new orders won’t begin to be delivered until 2023 at the earliest, and I have read a few opinions that explain how the market will easily absorb them. But still…

The other thing about the containerships is that there is a real dearth of names, at least on the North American exchanges. There are only a handful of stocks with meaningful containership exposure. And a bunch of those have already chartered most of their ships out for the long-term. While this was a prudent move in the past (after 10+ years of a bear market in containership rates) it is not right now.

ESEA, DAC and ZIM are the only pure plays I see that have meaningful spot/short term exposure. NMM does as well, but it is not a pure play, because it owns dry bulk ships, and its management is basically a shit show (though I do own it anyway).

I have been posting a lot of articles on containerships on the RNO board. I am not going to go through all the details of these articles but suffice to say, the situation for shipping containers appears to be getting tighter, not looser. It reminds me a little of the wacky situation that developed in 2007 with the dry bulk market.

Just sayin….

On to dry bulk.

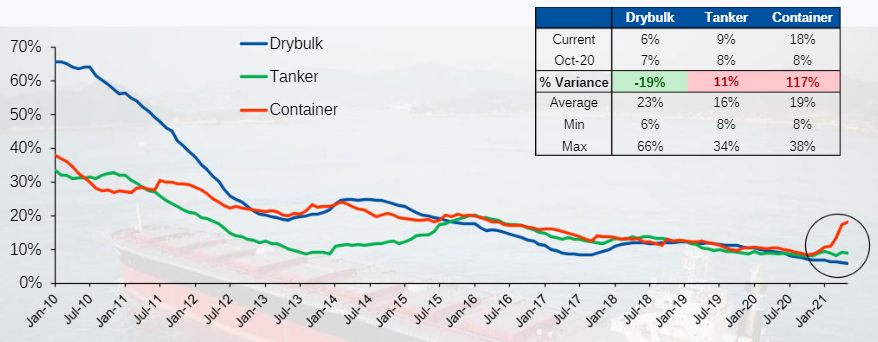

The dry bulk trade is a bit of a different beast. The dry bulk trade is a longer-term trade. Rates did spike, particularly for capesize vessels, but it seems to me they could go much higher for longer because the supply side is not responding.

In the short term though, the dry bulk rates are not as strong as containerships. In the case of Capesize ships, rates have pulled back quite a bit.

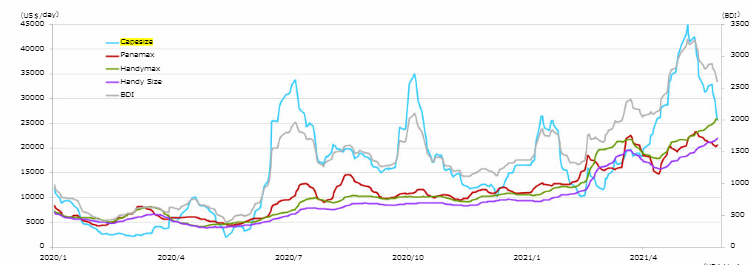

Q1 spot Capesize rates averaged $17,000, one of the best performances in several years while Q2 was tracking close to $30,000, a very high level only comparable to the 2000s bull market. But in the last couple of weeks capesize rates have pulled back to around $20,000 now.

But while Capesize rates have taken a breather, as you can see in the chart the smaller size ships have remained quite strong.

Capesize rates are very volatile/seasonal and so you can’t get too worked up over the volatility.

The big picture here is two-fold. First, dry bulk rates are going to depend on demand for bulk goods like iron ore, grain, coal, and metals. In this sense, the dry bulk sector actually fits a lot better with the commodity bull market thesis that I have been grappling with.

But dry bulk also has some negatives that come from that same thesis. For one, if China reduces steel production and switches away from dirtier steel production that will hurt iron ore and metallurgical coal imports. For two, over the longer term thermal coal transportation is bound to decline with stiffer carbon limits.

On the other hand, the dry bulk supply situation has not seen any increase in ships (see the above mentioned order book chart). The combination of shipyards that are full and the carbon requirements of new dry bulk vessels make placing new dry bulk orders a bit tricky. Star Bulk described it like this at the Capital Link conference:

The order book has decreased to a record low 5.7 percent of the fleet, with just5.8 million dead weight reported as firm orders between January and April. Upcoming environmental regulations and uncertainty about future propulsion has helped keep new orders under control, while shipyard capacity is quickly filling up with containership and other orders.

This is what Golden Ocean said about dry bulk on their last conference call:

It is clear that fleet growth is slowing down dramatically. In fact, we are looking at the lowest fleet growth in 30 years. At the moment, the order book is likely to stay muted. There’s a very limited amount of slots available before 2024. We see increasing prices for the assets, mainly due to steel, but also due to increased demand. And of course, availability of finance and new emissions are also keeping the order book in check.

We have a potential further catalyst as we will see the new IMO 2023 regulations enter into force. It is assessed by some that upwards 80% of the dry bulk fleet is not in compliance with the new regulations, and the easiest and cheapest way to get in compliance is by slow steaming. Therefore, we expect quite a lot of slow steaming from 2023 at a time where we are already seeing very, very few additions to the fleet.

For the next 2 to 3 years, we expect this situation to tighten even further. Demand is simply going to outpace supply until 2024

Finally, Stifel pointed out the following in a piece they did on dry bulk, titled “How High can you Go? Looking at Upside Potential in Dry Bulk Shipping”. They described how until ship owners know what the carbon rules are for their ships, they will be less likely to book new builds of dry bulk carriers than other types of large ships (like containerships and crude oil ships) because retrofitting a dry bulk ship is far harder:

Outfitting a large containership or VLCC with LNG capacity would only increase the cost of the ship by 5-10%, whereas the incremental cost for a Capesize vessel would be an extra 20% and for a Supramax it would be an extra 35%

The other nice thing about dry bulk is that, unlike containerships, there are a number of little shitco-like companies that operate in the sector and that will run up if rates are higher for longer. Grindrod is the one I bought so far, but there are others.

After today I am again cautiously optimistic that this idea is going to work out. But this is shipping so who really knows.

Thanks for another great post. Speaking of shitco-like dry bulk companies, have you had a chance to look at Seanergy Maritime Holdings (SHIP) and EuroDry Ltd (EDRY)? Seanergy is

capisize pure play and may be gearing up for a shipping boom by acquiring 6 capesize vessels in 2021, to go with their existing 11 vessels. EuroDry, a spin-off from Euroseas, may be worth a look, although the stock has risen 50% in the last 5 trading days.

I have looked at SHIP and that was one of the other “shitcos” i was thinking of. I haven’t looked at EuroDry before so thanks for that, I will.

What do you think about PANL, not as much upside, but downside also looks nicely covered there. And they got a bunch of new ships coming in. And it appears they do get some of the upside (see last page of presentation), and price hasn’t moved all that much yet due to a large shareholder cashing out.

Yeah they look just as good as any dry bulker as well. I have trouble differentiating which will be the biggest winners.