Ships and Steel – Managing versus Predicting

I always struggle with days like Thursday. A sudden about face in the market and you have to figure out what to do.

Two days later, I’m still not sure what to do. I have done stuff, but I may undo them or I may do other things altogether.

Four sectors that I own stocks in took a dump Thursday – steel, shipping, banks and gold.

Gold

So first off – gold. This one is easy. You just sell. I have found that it is already best to sell gold stocks first and ask questions later. If it turns around just buy them back. There is always a chance to buy them back with gold stocks. I have invested in gold stocks for 15 years. I can’t think of one time where they “got away from me”.

I don’t own New Gold any more, I don’t own any Gran Colombia (which I had bought Monday) and I sold most of Wesdome and Fiore.

The only thing that gives me pause is Wesdome – and that simply is that it hardly sold off.

The stock is (relatively) so strong. I don’t know what is going on there but while bigger gold names fell 5-6%, Wesdome was actually flat at one point on Thursday. That is why I kept a bit.

Banks

Second – banks. With the banks I am in a different spot because I have sold a lot of my positions. So this is more about whether to buy them back.

I was really surprised to see both the banks and gold down. They have been a hedge to one another over the last year. When one is up the other is down.

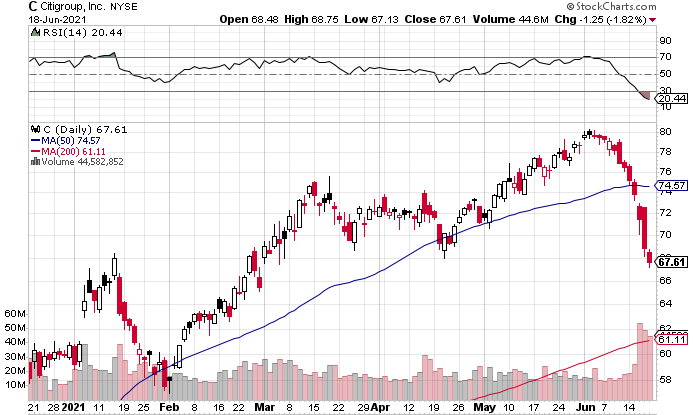

When you look at the big money center banks, they have been down for days. The charts of JP Morgan and Citigroup in particular are really ugly. I mean, what the heck is going on with this:

This large bank move was not Fed induced by the looks of when it started. It just carried over to the small banks on Thursday.Whenever the banks start going down I feel like I have to figure out what it means. This case is no different but I have not figured it out yet. I won’t be adding to my positions until I do.

As for the other two – shipping and steel… I am battling my mindset versus the volatility of these sectors.

My mindset is – do not lose money. If I make some great, but more important, don’t lose any. The problem is that shipping and steel are two sectors where you can lose money very quickly if things go against you.

Which is why, even though they do not make up a particularly large part of my portfolio, they are taking an outsized amount of my attention right now.

Shipping

In the case of shipping, the stocks suffered quite a drop on Thursday, which makes the decision more immediate.

But I sold some of the shippers the week before so that played into it as well. I did not go into Thursday’s drop with full positions in these names.

Nevertheless, I did sell some more. For reasons I will explain. But on Friday I added a new container (not containership) idea, Triton International, so that offset those sales some. I still own less of these stocks than I did coming into Thursday but enough to be nervous about them going forward.

Containerships

Let’s go back to where the market is. First, containership rates are still at all-time highs and they look to be going higher.

This article, from American Shipper, says that rates are actually “accelerating”. There is a huge backlog of ships (90 of them) just sitting off the coast of China ports because of a Covid outbreak at the very large port of Yantian. While this backlog has come down a bit (from 104 a week previous) that is only because the ships scheduled to dock at Yantian are omitting the port altogether.

Ships omitting the port has consequences because the containers that are supposed to be loaded from the port are stacking up. According to this CNBC article:

Approximately 160,000 40-foot containers, the equivalent of 300,000 TEUs, or 20-foot equivalent units, are waiting to be exported, according to logistics companies with operating knowledge of the port.

300,000 TEUs would be about 10 days of shipping from the port.

This article from gcaptain put it this way:

Yantian Port now says it will be back to normal by the end of June, but just as it took several weeks for ship schedules and supply chains to recover from the vessel blocking the Suez Canal in March, it may take months for the cargo backlog in southern China to clear while the fallout ripples to ports worldwide.

“The trend is worrying, and unceasing congestion is becoming a global problem,” A.P. Moller-Maersk A/S, the world’s No. 1 container carrier, said in a statement Thursday.

Over 90% of the world’s electronics are exported out of the Port of Yantian.

Another article from Lloyds List says it will take weeks to work through the backlog and that is the best case scenario.

The gcaptain article estimated “the congestion in Yantian will take six to eight weeks to clear. That timetable is a problem because it extends the disruptions into the late-summer period of peak demand from the U.S. and Europe, where retailers and other importers restock warehouses ahead of the year-end holiday shopping rush.”

So the port congestion runs into the holiday rush runs into other economies opening up as they become vaccinated. And no significant new ships builds are coming along for 2 years.

Meanwhile the containership companies are booking 2 or 3 year charters at rates well above $30K/d. Today I saw a 3 year time charter at $42k per day and a 5 year charter at $34k per day.

The much, much hated NMM (just read the post of @the5hippingman on twitter) charted 5 containerships for 36 months on Tuesday. With these charters these ships will bring in $60 million of EBITDA per year.

That is from 5 ships. NMM has 51 dry bulk ships and 38 containerships. NMM has an EV of $1 billion.

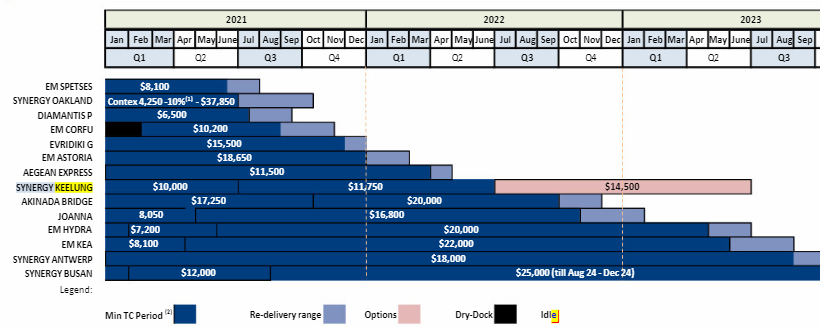

As for Euroseas, which has been my main containership play, they have about half of their vessels opening up for new charters between now and the second quarter of 2022.

Those vessels are going to recharter at much higher rates.

The SPETSES, DIAMANTIS AND CORFU are all currently operating at charter rates of $7k-$8k per day. At current rates they will be able to re-charter at $20k-$25k. The OAKLAND, which is a bigger Panamax ship, was booked out at $4k per day in Q1. In Q2 they will be on a better but very short charter of $38k until July. When that charter ends, these sort of Panamax vessels are getting $40k for years right now.

Analysts have been raising estimates for Euroseas for some time, and we are now at an average of $7.42 EPS for 2022.

So the market looks very positive. What makes me nervous about the containership market is the new build order book. That order book (which I showed last post) has grown a lot in the last 6 months or so. That makes me think that investors will be less likely to bid up containerships on current earnings, as they realize those earnings won’t last.

The other thing that is tough about containership stocks is there just aren’t that many stocks out there, at least on North American exchanges. It is one of the reasons I bought Triton.

The cheapest of the bunch is NMM, which is one of the basket of 3 that own, but it has a real problem with credibility, and because their CEO, Angelica Frangou, does not always do what is in the best interests of shareholders, there is a chance that some day we wake up to news with NMM that destroy the value of the 2x P/E valuation.

Euroseas and Danaos are both up a lot in the last few weeks. So its really hard not to be trimming those on the least bit of worry.

So I sold some Navios and Danaos Containerships and a little more Euroseas. But I still own all to a lesser degree, as the market is so strong I could easily see it having at least one more leg up.

Dry Bulk

The dry bulk market is a little different than the containership market because rates are just strong, not crazy, insanely strong, while the order book is very, very low (see my last post for this). For this reason, I am a little less trigger happy with my dry bulk stocks.

I did lighten up on Star Bulk earlier this week but I ploughed about half of that into Diana Shipping and Globus Maritime, so my overall exposure to dry bulk is still about 75% of the what it was (with containerships I’ve taken about 1/2 off the table overall).

Together with Grindrod, these moves mean I’m moving down the chain in quality and size, which might be seen as a dumb idea if we are moving towards the end of this move.

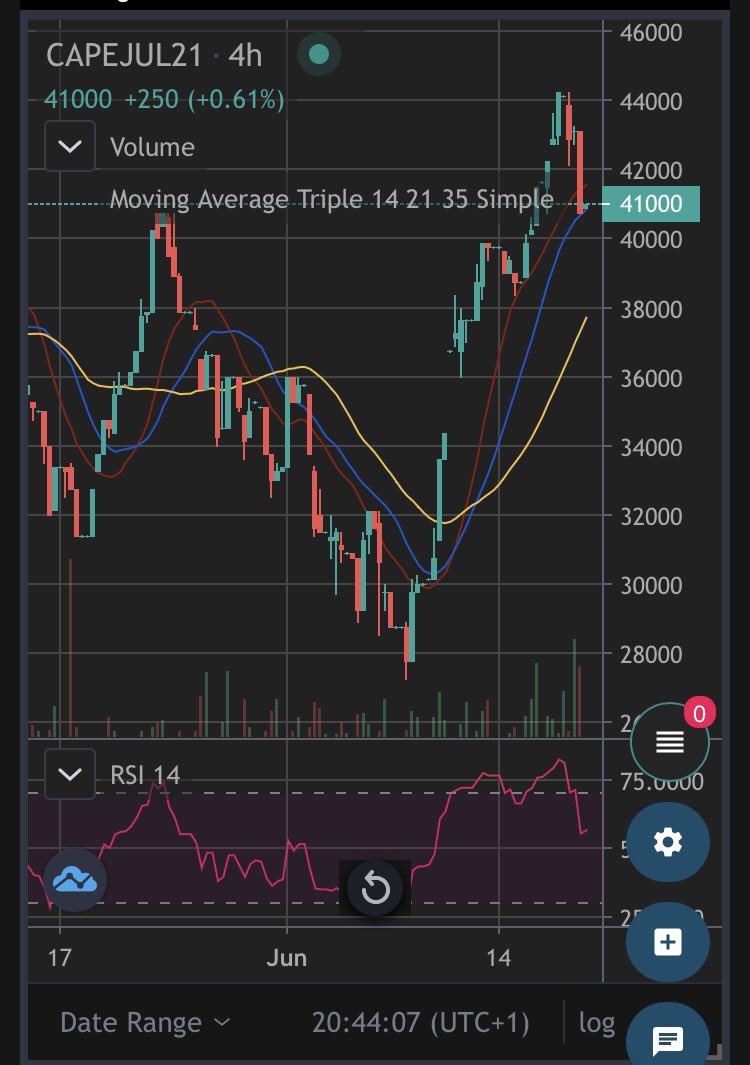

In the dry bulk market, while Capesize FFA’s (that is future freight rate agreements) have pulled back a little the last couple of days, they have had a very good move over the last 2-weeks and they are around $40k, which bodes well for dry bulk shippers.

The smaller size ships, so the Panamax, Supramax and Handysize, are seeing even better rates. Grindrod and Globus Maritime both own these smaller ships. Diana Shipping owns both the larger Capesize and the smaller Panamax/Supramax size.

The crux of my desire to hold dry bulk is that stocks like Grindrod are just so cheap on multiples. I’m going to go through Grindrod as an example.

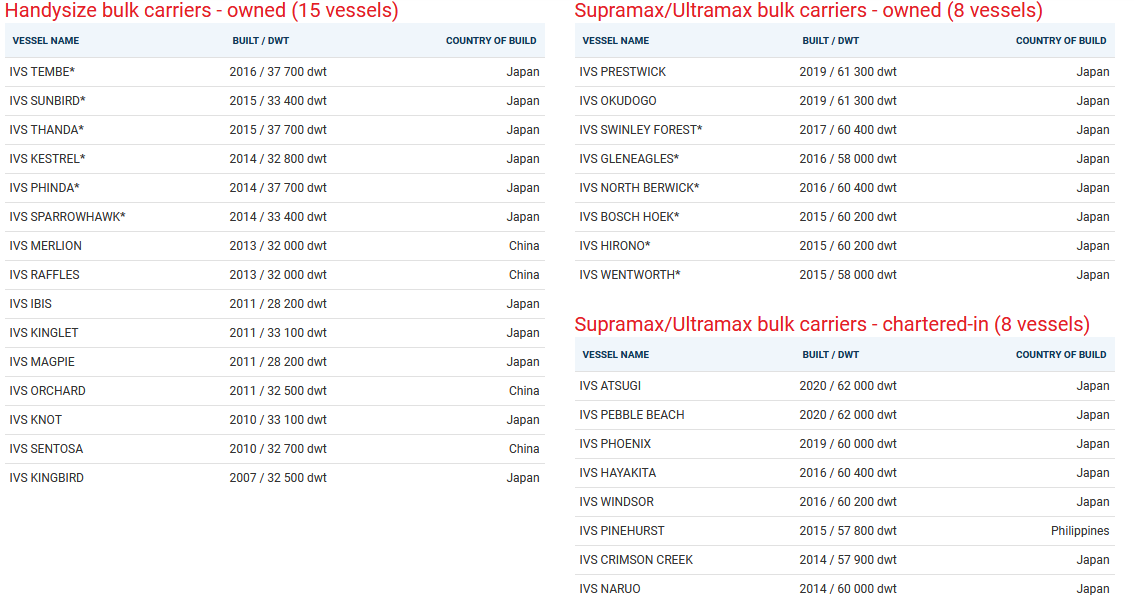

Grindrod has 15 Handysize and 16 Supramax size vessels.

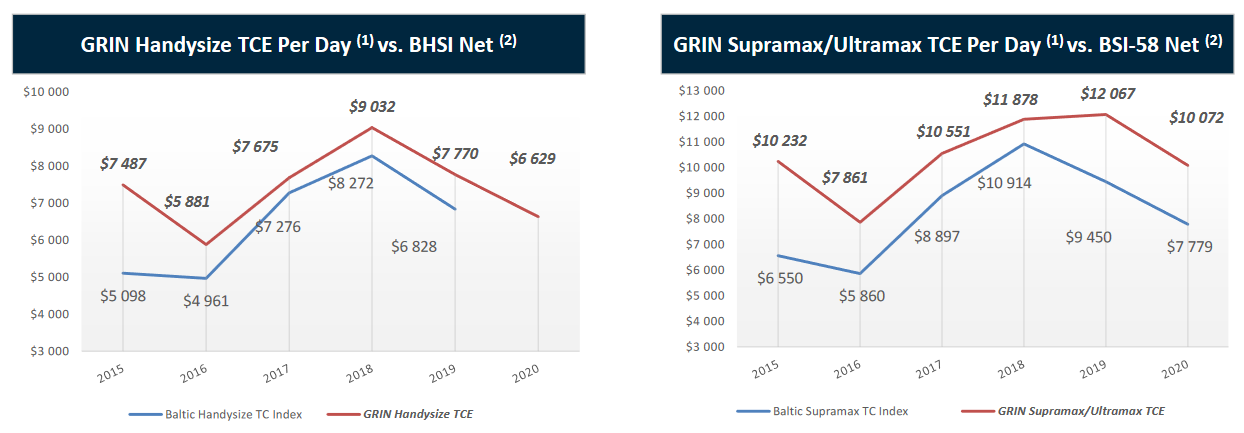

Now let’s look at where rates are versus where they have been. Supramax vessels are contracting out at $32k per day right now. In 2020 Grindrod averaged $10k per day. Handysize vessels are going for $22k per day right now while Grindrod averaged $6.6k per day in 2020.

So Grindrod is experiencing far higher rates now that it has in the past. I mean, we are close to triple the 5-year rates on these ships.

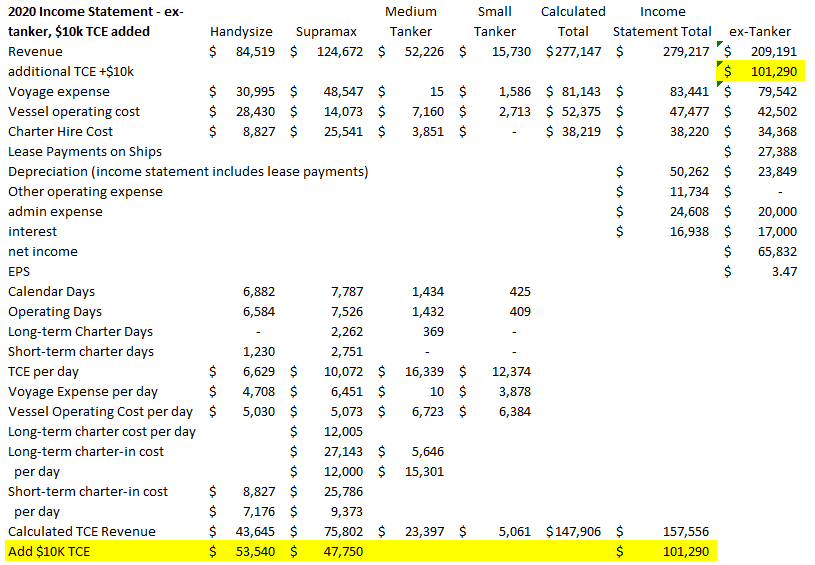

I did a very back-of-the-napkin estimate of what even an extra $10k of TCE means for Grindrod. $3.50 of EPS. You can see the results below.

The spreadsheet is a bit convoluted, but the important column is the last one, where I have taken the 2020 numbers, removed the impact of tankers (they have since been sold) and added revenue from an additional $10k TCE for the owned and long-term charter operating days.

What is worthwhile pointing out is that A. TCE’s right now are more like $15k-$20k above the 2020 numbers. B. I’m assuming no positive impact from the short-term charter-in days (which were ~1/3 of Supramax days in 2020). C. I did not reduce the debt payments even though Grindrod has paid off about 1/4 of their debt. And D. cash flow is higher – nearly $90 million.

So to sum this up: Grindrod has a market cap of $200 million right now. Cash flow at the +$10K TCE level is close to half their market cap. Every $10k increase in TCE after that is another ~$100 million.

So that is why I am reluctant to sell. Particularly when the order book for new builds is extremely low, it appears that the environmental regulations coming into play on propulsion systems is going to make shipowners wary of ordering new builds, and shipyards are filled with orders of LNG and containerships for the next couple of years anyway.

Whereas with containerships I am wary of how high investors will bid up stocks when the end of the cycle can be seen, I cannot say that for dry bulk.

Steel

In the case of steel, the two stocks I own, Stelco and Algoma, did not really go down much. So the question becomes, do I sell while I still can?

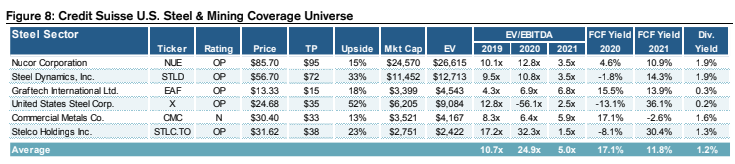

While steel makes me very nervous, I still decided to hold on. As I wrote about previously, both Stelco and Algoma are very cheap compared to their US peers. According to Credit Suisse, Stelco trades at like half of what the US steel companies do. I don’t see any good reason for this discount.

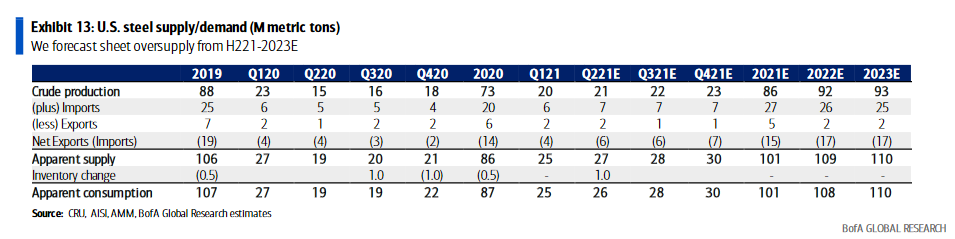

The bear case for steel is summarized by Bank of America, who has been calling for “Steelmaggeddon”. Steelmaggeddon for some time. They are basically saying a bunch of new supply coming on that will wipe out the deficit and bring prices back to $600/t next year. Actually, BofA was saying by H221 but that does not seem likely now, so they have pushed it out to 2022 now.

This is BofA’s US supply/demand forecast for their Steelmaggeddon forecast:

It actually seems pretty balanced to me (the numbers don’t actually add up either). It also depends on steel demand not getting back to 2019 levels until 2022.

On the other side, Morgan Stanley is pretty bullish steel prices. They think steel could stay near the $1,700/t level until Q1 of next year.

They note that: demand strong across all end uses, demand does not appear to be inflated by significant double ordering, inventories are uncomfortably low and some service centers are seeing “unprecedented level of contract demand”.

Average estimates are for Stelco to earn $13.50 this year, followed by $6.50 next year (because no one believes steel is going to stay near this level). Algoma isn’t covered by anyone but its multiples would be about the same.

The reason to keep an eye on steel is China and carbon. If China is serious about their commitments to greening steel, they have to begin to slow down the dirtiest production.

China produces about 1 billion tonnes of steel a year. If China cuts even 1% of its dirtiest steel production, that is more than all the new North American capacity adds next year. And China is talking far, far bigger numbers than 1%.

FT has been the best on reporting this story. They said in an article last week that:

These changes are going to have a big impact on China steel production over the next 4 years:

The Tangshan province, which produces 14% of China’s steel promised big cuts earlier this year:

It is almost unimaginable to me that China could drop that much steel production. The market would go crazy. Chinese steel companies are already trying to build plants outside of China to offset. It is going to be a delicate balance.

And so far this year, we aren’t seeing the cutback. Steel production in China, at least the official numbers, is up.

So it might not be a huge cut overnight. But my point is more on direction. China is not going to be adding steel production like they have, at the margin they are more likely to reduce it, and as a result it is quite possible we could see exports from China decline.

This seems to me to be the sort of thing super cycles are made of.

Going back to that BofA supply/demand balance, they are predicting exports to the United States to increase.

Add it up, and I’m not ready to through in the towel on these two names just yet.

It seems kind of counter intuitive that China would push up steel prices that much. With how much they are now frantically trying to push down other commodity prices.

Just curious, why not own LEGO, as that seems potentially the cheapest of the bunch here?

I think the big picture dynamic that may lead to higher steel prices than historical averages is that China is committing to decarbonization, will shut heavily polluting blast furnaces and that will limit supply increases.

LEGO is Algoma.

Oh yea my bad.

So the thesis is basically, elevated steel prices at least at $900-1k per ton for at least the medium term. In that case Algoma is trading at about 3x earnings. And will have an EV of zero in about 3.5 years.

But isn’t Algoma much cheaper? They generated $500m in EBITDA during 2018-2020, or roughly 33% of current market cap, while Stelco only generated a little over 10% of their current market cap in EBITDA during that period. And that is before planned improvements which will lower cost significantly for Algoma.

Also the $900m EBITDA figure for 2021 seems pretty conservative with where steel is expected to trade over the next 12 months.If in Q4 this year and Q1 next year they can fetch $1300-1700, they would earn >50% of their market cap in 2 quarters.

Interesting article on prime steel scrap supply situation:

https://www.fastmarkets.com/article/3993977/opportunity-for-a-scrap-pricing-supercycle

It paints a pretty pessimistic picture already a few years out. Given that all these steel producers are stampeding into EAF furnaces, maybe finding a company that profits from high scrap prices could be an interesting play?

One way is to buy a Stelco that is using blast furnaces. Higher scrap means higher steel prices.