Puke Buying

Corrections like this are very hard. No matter what you try, it is extremely difficult to make money on days when the market is down 90 points.

I can almost stay flat on my margin account because I am short enough SaaS and momentum stocks to make up for the carnage on my longs.

But in my RRSP or my wifes cash account, even though the stocks I hold there are more weighted to dividend paying, and even though I have the index hedges, it is really tough to not lose money on a day like Friday.

Think of it this way – on a day like Friday you are likely to have 3-4 stocks down 5%. The index is down 2%. So you need 2.5x the holdings in the inverse index just to make up for those 4 stocks. Pretty quickly you’re biggest risk is all the inverse ETF you hold (which can go south on you quickly). You just can’t make the numbers work. Not to mention that if you are putting that much into just beign hedged, you might as well just be holding cash.

I think that the only time I managed a correction ideally was during COVID. And that was just because it seemed so obvious at the time to just get out entirely.

But now? I have been dragging my heels on getting out entirely. Because things just don’t seem that bad. The market seems bad, but the world doesn’t seem that bad. And many stocks are very inexpensive.

So I’m hedged, but I’m not cash. And there is a difference between the two in that when the shit really hits the fan, as Friday showed, hedging does not mean you don’t lose money.

You could put my investment ideas into 4 buckets right now.

- A bunch of banks/insurers

- A bunch of biotechs

- Gold/metals related

- Small cap idiosyncratic

I’m going to go through why I own each of the first 3 buckets.

Banks

Bucket 1 is the biggest. I own a bunch of regional and community banks that all trade at very low multiples (most are close to tangible book and at or under 10x earnings).

During the first two weeks of the year, these stocks actually did really well. As I wrote about here, my portfolio was actually going up a little, and it would have been going up a lot if not for the drag of biotech.

But this week, not so much. The KRE (that is the regional bank index) gave up its gains from the past two weeks. CUBI had a bad week. Most of the banks I own gave up the previous weeks of gains.

Do I sell? Get out?

It is hard for me to agree to that.

The outlook for banks and insurers, with Omicron likely ending COVID, with rates on the rise, with an economy that should be at least okay, should not be that bad. And the stocks are some of the cheapest one’s out there.

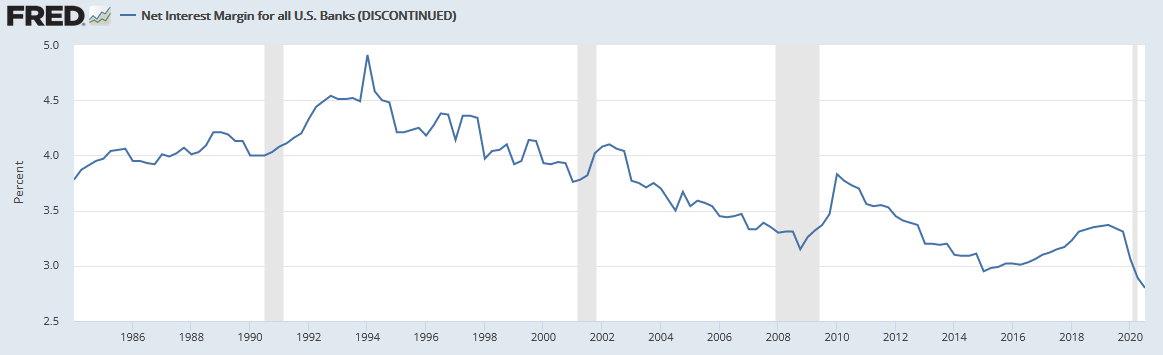

I also think there is a chance we see something that hasn’t happened in years. Expanding interest margins.

I don’t think the Fed, the Bank of Canada and others can raise short term rates too far because too many households have variable mortgages that depend on those rates. But they don’t control longer dated rates.

I wonder if we could see a world where short term rates remain low even as longer term rates slowly rise over time. I’m not talking about a wild-hyper-inflation-type rise like the crazies are shouting about. But a modest rise, so that net-interest-margins for banks maybe go up 0.5% in the next year.

Which should be beneficial because the net interest margin of banks has shrank so much over the last 10 years.

If you go through the banks I own, even though some of them have developed other businesses that don’t depend on interest, they still derive a lot of their income from interest margin. And with interest margins so low right now, for many a 0.5% increase would be akin to doubling their non-interest-income business. So its significant.

To put it another way, with commodities the old saying was to buy when the PE was high and commodity prices low and sell when the PE was low and commodity prices high.

With the banks, we are at multi-decade lows in NIMs, but the PE is low. Far lower than the market average.

So sell now? Ehhh…

On to biotechs

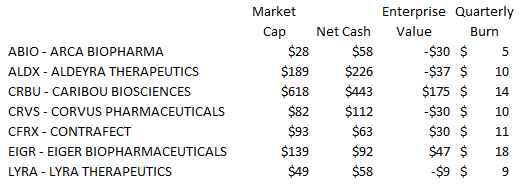

My one big mistake over the last 4 weeks has been thinking that buying biotechs at prices near or under cash with drugs in late stage trials would be a good idea. My premise, which has proved false, was that these stocks couldn’t possibly go below where they were during the peak COVID panic.

As it turns out – they can, and cash has only been a partial counter force against further share price losses. When the XBI goes down, they all go down, idiosyncrasies be damned. My only redemption has come from my SaaS and momentum short trades which apparently are tied to the hip with the XBI (for now) and thus makes money as these names lose money.

Where we are now, four of the biotechs I own have negative EV’s based on Q3 cash levels. The other 3 are getting there.

Do I sell?

Well clearly I’ve been wrong. Cash on hand has been only a bit of help. But at this point: A. apart from Caribou these stocks are all trading at only slight positive or negative enterprise values, B. apart from CRVS these stocks are at levels that are lower than they were during the worst of the COVID panic and C. they are all terribly, terribly oversold.

Nothing fundamentally has changed with these names. They are all closer to their next data read-outs then they were a month ago.

And here’s the thing I keep thinking: these names aren’t goosed by COVID numbers like a Netflix or Peloton. We are seeing an unwinding of the COVID trade, sure, makes sense, but these are just collateral damage to that. In fact, th forces at play for these biotechs are the opposite: because of COVID, drug trials didn’t get done, patients didn’t enroll, everything slowed down. Now that is ending and we can get back to normal.

I also don’t buy the argument that biotechs are rate-dependent stocks like SaaS/tech companies are. Consider this chart, which was posted by @Amarillo_Slim1 on twitter.

Biotech stocks have traded at a far higher EV/cash multiple in the past during periods where rates were much higher. So the “long-dated-assets-discount-rate-rising-present-value-compression” argument doesn’t hold water to me.

Finally, big drawdowns with biotech stocks just happen. And then they end. Consider this chart of Eiger, which is the one biotech I’ve (unfortunately) held through this entire drawdown:

This drawdown is unique in terms of the absolute price it has taken Eiger down to. I honestly never would have thought we’d see a $3-handle on this stock, what with an approved drug generating revenue and with Phase 3 results on HDV less than a year away.

But what is not unique is this steep, sudden drawdown. It has happened over and over again. And most of the time, the stock has recovered almost as fast as it has fallen. If history is any guide, it could be back to $6 in a month.

That makes me very reluctant to bail out here. Even as each of these stocks painfully slip a few cents more almost every day.

Eiger also presents an example of another point. Funds are getting involved with some of these beaten down biotechs.

The funds and clients of Columbia Management Investment Advisers now own 20% of Eiger (or more if they continued to buy this week). They have bought over 6 million shares in the last year including over 1 million in the last 3 months.

The funds mentioned in the filing that hold the bulk of the shares are Seligman Tech and Seligman Offshore funds. These don’t look like dumb investors to me. They are run by Paul Wick. His funds were profiled in November in The Institutional Investor:

A hedge fund manager best known for running long-only mutual funds is enjoying one of his best years in recent memory.

Paul Wick’s Seligman Tech Spectrum fund is up 24.37 percent for the year through October, well ahead of many other tech- and internet-focused funds, a number of which have been mired in the red for most of the year. “We’re playing in a different area that they pretty much ignore,” Wick asserted in a recent phone interview.

Wick is the lead portfolio manager for the Seligman Technology Group at Columbia Threadneedle Investments. He has been heading up Seligman’s technology investment group since 1990.

Wick is not a momo growth guy, which is probably why he has been around for so long:

“We are fundamental growth investors [who] are valuation aware,” Wick stressed in the phone interview. “Others have a tendency to forget about valuations and drive off [the] cliff periodically.”

Wick believes his group is more focused on a company’s profit margins and cash flow, as well as companies repurchasing stock or doing accretive acquisitions.

Anyway, if you read through the 13D filing, you can see that Wick’s funds and clients were large buyers in late December in the low $5s. Now we are a buck lower.

I added a bit to my biotechs on Friday. I have been cautious the last two weeks and just tried to do nothing with these positions. But Friday I broke down and added to ABIO and ALDX. Both of these stocks are WAY below cash and they have years of runway given their current burn.

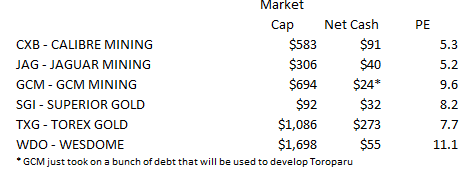

Gold

Gold is the last single theme bucket and the last bucket I will talk about.

But what can you ever say about gold stocks? Cuz who the hell knows.

If it really is a market collapse gold stocks will go down… maybe. But maybe not. During COVID they actually went up until somebody gamed the 3x ETFs and then they gave up all their gains and then some in like 3 days.

What I do know is that tech and SaaS are long duration assets. That means they are dependent on their earnings stream many years away. In the case of some of these SaaS names it had gotten so stupid that you would have to go out 30-40 years to truly realize the value on a discounted cash flow basis.

Gold stocks, on the other hand, are (like bank stocks) the opposite. They are short duration assets.

Banks give you the earnings right now, dividends right now and in some cases buybacks right now.

Gold stocks do too. In fact they are even shorter duration – basically the length of the mine, especially now when exploration is priced at a big, fat zero. Its all about today’s cash flow.

The gold stocks I own are also very reasonably priced.

Soooooo… the case can be made.

The trick right now is figuring out if these stocks can go up while other stocks go down.

It seems like the growth-cohort of SaaS/momentum/stay-at-home stocks is finally seeing their good fortune come to an end. As I tried to point out in my last post, you can make a case that there is further to fall.

And quite honestly I have a hard time believing that the descent of the growth stocks will be over until we finally see Tesla give up the ghost. It is the unquestionable kingpin and as long as it still stands the triple-waterfall collapse will not be complete.

With that as my premise, the question I can’t answer is if other stocks can go up if Tesla and all the other stocks held up by it keep falling.

If I knew the answer to that I I wouldn’t have so many hedges on my portfolio that I am essentially barricading it like I was about to be attacked by the huns.

But I do know that the stocks I own are the antithesis of growth/SaaS/momentum stocks. They are very low PE stocks. They are short duration stocks.

And I do know that during a regime change there are new winners. And even with the pummeling, I have optimism that I might be in 1 or 2 of those.

I agree, tough market, does the market pulldown everything or do individual stock fundamentals win out.

Wondering why no energy stocks? They have been on fire and fundamentally seem to have a long way to run given the underinvestment the last few years.

Well I have owned VET for some time now and I bought back some SDE I sold this week. But I decided to write this post about “buckets” so I just limited it to sectors where I owned 5+ names.

Also another thing I have been wrong about so far is that bets on companies like CHE/UN were proxy energy bets because they would benefit from price rises due to the high gas prices in Europe. So I felt I was long energy in that way, but it hasn’t really worked.

OK, thanks. Just wanted to see if I was missing something with you being out in Alberta. I’m about 10% energy and that is being generous counting stocks like BDI. Its been hard to buy as it feels like chasing, and given how poorly my energy forays have done the last few years.

I know you owned BMRA before. Have you thought about getting back into that name? They are about to announce their end-trial results by end-January.

I came close to making it a tax-loss buy back at the end of December. I think the reason I didn’t pick it was really the lower cash position, which hasn’t really worked out for me so take that FWIW, and also I was a little uneasy about how these results have gotten pushed back a couple times.

Understood. BMRA has been holding up well so far against the market sell-off, so that’s a good sign.

OSTK might be worth a look as well. The stock currently trades at 8-9x 2022 EV/EBITDA, and with the big upside potential from Medici companies, it seems very attractive You probably know more about OSTK than I do. Just bringing it to your attention in case it might have slipped off your radar.

Ever look at SMID anymore? Or way too overpriced, even with infrastructure bill?

great post, you nail it with this “Because things just don’t seem that bad. The market seems bad, but the world doesn’t seem that bad. And many stocks are very inexpensive.”

Regarding banks and NIM, have you actually checked the sensitivities? I randomly picked out CUBI and it is not at all clear to me that NIM is going to benefit a ton from rising rates.

They model “interest rate shocks” but really depends on what the assumptions are, it seems to me they assume the entire yield curve shifting up. In that case per last 10-Q for 3% higher rates they earn 8.3% higher net interest income, not that much more.

https://www.bamsec.com/filing/148881321000168?cik=1488813

If you check the 10-K page 97 https://www.bamsec.com/filing/148881321000069?cik=1488813

they had actually more liabilities than assets with duration >5 years.

Only 3 months or less and 3 to 5 years is the opposite but then we don’t know how much in each is floating or variable….

Of their interest rate hedges we only know this

“As of December 31, 2020, Customers had five financial derivatives designated in qualifying cash flow hedge relationships with a notional aggregate balance of $1.1 billion.”

So… I don’t know.

That’s not how I am looking at it Florian but to be honest I’m not really interested in getting into this with you. You have your opinion and that’s fine. best of luck.

I don’t disagree that they are cheap I was just wondering if you have looked into this at all.