(Probably) a Bear Market Rally

I wrote back in early December how “stocks felt heavy”. This felt like a bear market to me, even though the indexes were holding up extremely well. They went on to new highs in the late December Santa Claus rally.

I went on to describe how it felt eerily like the second half of 2015. And how I was worried that the first month of 2022 would be like the carnage of the first month of 2016.

That feeling certainly turned out to be right. We have seen a very similar result. And now that so many stocks have become incredibly oversold and have charts that have gone straight down, it looks like we might rally.

But I think this will be a bear market rally.

That means that I need to be careful not to keep longs too long. I’m hopeful that I can get some nice bounces in the beaten down names I’ve been adding to over the last couple weeks. But I have to be careful not to get greedy and hope for a return to prior highs.

I’m looking for a bounce. A strong one, at least I hope, but not a straight run to higher highs.

If I had any guts, what I would have done over the last couple weeks is just buy more biotechs, buy more small caps, load up. This has been a huge drawdown and so many names are trading at levels that do not value the business at very much, and in the case of Biotechs, value it negatively.

But as it is, I am betting with the money of my family, which I have done well with over the years and so my primary objective is not to blow it. Don’t lose, try to win where you can. The antithesis of the hedge fund that needs to perform to survive. So small risks only.

I did add to a couple biotechs on Monday when the fear was palpable. And there is one new biotech I added this week, on Wednesday after results. More on that in a second. But I did not go all in by any stretch. As much as I think this sector is poised to rise, I can’t take too many chances in case I am wrong.

There was also one non-biotech name that I added to this week that I wanted to talk about and think may be mis-priced here after a very deep drawdown.

Finance of America.

FOA has done nothing but go down since its SPAC merger was finalized in March.

The correct response to this chart would be – but this is a SPAC, right? Isn’t this par for the course?

The list of SPACs down 80% or more is very long. There are so many terrible businesses, or really just businesses that are way to early stage to be on the public market, that have gone public via SPAC, and now they are all getting killed.

But FOA is not really like most of these businesses. This not a LiDAR or robotics or EV company expected to begin generating revenue in 2030 and trading on the hopes and dreams of an investor presentation until then.

FOA is really kind of boring. They are simply a mortgage origination company.

That comes with its own problems. Like many mortgage companies, FOA is complicated. They originate loans, they securitize loans, their balance sheet is a mess of loans held for sale and debt held to fund them. Much of it is non-recourse and not really part of the book value of the business, per-se. There are Special Purpose Entities that hold the loans before sale and variable interest entities where FOA has no economic interest but does hold management over and so they are consolidated. It makes understanding the company very hard.

On top of that usual complexity, FOA has extra complexity because it is not a usual origination company.

Your typical mortgage originator sells the majority of its loans through Fannie and Freddie securitizations. These are called agency loans. These are loans to prime borrowers that qualify to be insured.

Fannie and Freddie originations are pretty commoditized. There are lots of mortgage origination companies that can make these loans, it doesn’t lead to much moat and margins are tight.

However last year with COVID, this market did what a lot of markets did. It went on tilt. Margins skyrocketed to (I believe) over 600 bps at one point as people refinanced their homes en masse . The usual level is more like 150-200 bps.

That was great for FOA because they made a lot of money along with every other mortgage originator.

So FOA rode this wave and came public around March. Which is about the same time that the dislocations in the mortgage market began to ease.

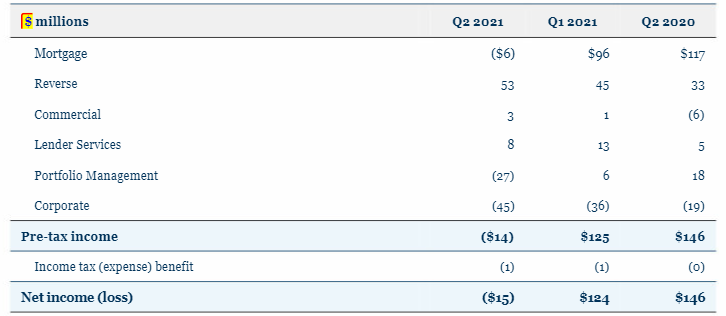

The consequence is that the blowout earnings of 2020 reversed in 2021. Their Q2 earnings look like a mess.

So what do you think a stock will do if it goes public and the first quarter out of the gate its highest income business (Mortgage) goes from $117 million of pre-tax income the year before to -$6 million this year?

It’s going to shit the bed is what its going to do.

You can try and explain all you like that this is “in-line with industry trends” (they did), that there are a bunch of “non-recurring costs” that impacted the results (there were) and that mark-to-market accounting hammered the numbers even more (they did).

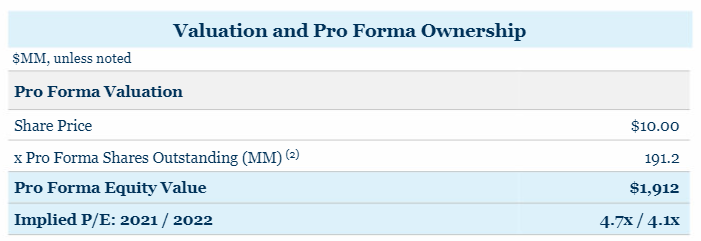

No one cares. Most of your shareholder base (the one’s that can sell the stock) only have a foggy idea what you do. They bought you because you were a SPAC that went to market at a $1.9 billion equity value on the belief they were buying something at 4x earnings (see below, from the March 2021 presentation).

And now they are saying, these guys lost money? Get me the hell out of this!

So selling begets selling. It doesn’t help that gain-on-sale margins on mortgages continue to normalize through Q3 and Q4. Take a look at the chart of Rocket Companies, LoanDepot or even Mr. Cooper. They are all going down because mortgage gain-on-sale profits are coming back to earth.

Ok, so why am I investing in this hot mess?

Because like I said at the start of this, FOA is not your usual origination company. And I don’t think the market has bothered to look at it enough to figure that out yet.

Yes, FOA has an origination business. But a large part of that origination business is non-agency mortgages. Think subprime. And of the business they have, most of it is purchase, not refinancing.

So ok, that could help. But its still originations.

The bigger part of the story is that FOA has 3 other businesses that are not originating mortgages for people buying or refinancing their house. These businesses are:

- Reverse Mortgage

- Commercial Lending

- Home Improvement loans

Each of these are far more niche than mortgage originations. That also means, they aren’t as much a commodity business that is subject to low margins. They aren’t nearly as rate sensitive.

Together these businesses make up what FOA calls their Specialty Finance and Services segment.

Likely because they recognized that their stock was in deep doodoo, FOA scrambled on their third quarter call to try to explain to investors that they are not just a mortgage origination company. They outlined a 7-point “market mis-perception” case:

- Their comparison set is mortgage companies

- Yet their origination segment is only about 20% of earnings

- Individual companies in their reverse, commercial and lender services businesses trade at far higher multiples than mortgage companies and then them

- transaction multiples in these sectors always underscored by expectation of sector growth – example of Anchor Loans by Pretium Mortgage a week ago. See here: https://www.prnewswire.com/news-releases/pretium-acquires-anchor-loans-to-deliver-enhanced-capital-solutions-for-homebuyers-301414181.html

- The mortgage platform they have is geared to purchase market

- It is also geared to non-agency which they think will reduce volatility compared to agency dependent refis

- They plan to double down on reverse, commercial and home improvement lending

It didn’t really work. It is tough to change perception when you are a SPAC that went to market as a mortgage company, hardly any brokerage covers you, and all the mortgage companies and SPACs are getting creamed.

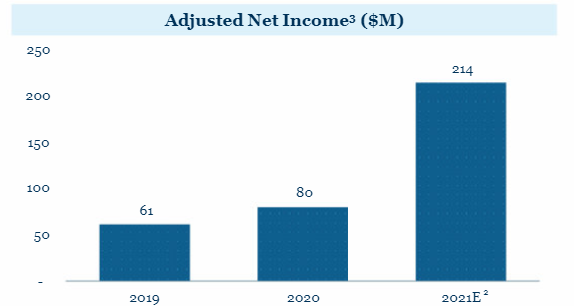

So where are we now? Well, FOA gave the following guidance for Q4:

It works out to about $70 million of adjusted net income for the quarter. This is less than the $75 million of adjusted net income in Q3. So still not good right?

Well, yes and no. Even if FOA meets guidance it is down quarter over quarter, I’ll give you that. And that is largely because the mortgage business continues to normalize (meaning go down), which is really no surprise. A bank I follow closely, called SB Financial Group, has a large origination business. They reported Thursday. Their originations were down 25% year-over-year and their gain-on-sale margin was down from 503 bps to 288 bps. LoanDepot hasn’t reported, but their guide was for Q4 gain-on-sale margins of 210-260 bps versus 290 bps in Q3.

So yes, earnings are still being dragged down by mortgage. But the rest of the business – the Specialty business – is doing quite well.

At the midpoint, adjusted net income from SF&S would be at $64.8 million in Q4. In Q3 it was $59.6 million. This year it is up pretty significantly over 2019 and 2020.

The problem is the mortgage business has been down more.

But where we are now is an adjusted net income level of around $280 million annualized with the mortgage business contributing ~$20 million of that.

There are 191 million shares fully diluted. So that works out to $1.50 EPS. The stock is under $4, trades at about 2.5x PE.

While the stock traded at 4x PE at the time it went public, that was on a much higher “E” and those were on peak, unsustainable, earnings. Now it is on earnings largely from SF&S, which is growing.

I’m not the only one sniffing around this stock. Leon Cooperman was on their Q3 call asking questions. Cooperman held 900k of Replay Acquisition Group before the merger, but has increased his position to 4.4 million shares in Q2 and 4.7 million shares in Q3. He has been buying all the way down.

Cooperman focused his questions entirely on the long term:

Just a couple of high level questions. I noticed on your press release of earnings, you referred to yourself as a high growth consumer and specialty lending business. I think the stock sells is somewhere between two and three times earnings, we’re starting to see just high growth. I know you spent a lot of time this morning discussing why, do you think the market, are you relying upon the market just to wake up and change the expectations or there proactive things you could do, I notice for example that GE is breaking themselves up in the three companies. So, that would be question number one.

36:19 And related to that question is, forget about the next quarter, but on a five-year basis, when you refer to yourself as a high growth consumer specialty lending business, what kind of growth do you think the company can support on a five-year basis per annum? And secondly, on the cover sheet there are three earnings numbers, it’s the basic $0.36, there’s the fully diluted zero point two two dollars, and then there is the adjusted net income of seventy five million dollars or zero point three nine dollars, which do you think given you’re now into the business the most relevant to your business.

36:50 The kind of number that we shaped dividend policy going forward or are the kind of activities? Those are two questions, and congratulations on a good quarter.

The answers were that they aren’t going to break themselves up because the mortgage business generates customers for the specialty businesses, they can grow SF&S at 15% per year and that we should focus on the adjusted net income number.

Cooperman has always been a pretty astute mortgage investor. I followed him into Arbor Realty years ago (at about the same price as FOA is at now, coincidentally) and did quite well alongside him.

So that is FOA.

A Little Bit of Biotechs

I finally bought more Eiger this week. I waited and waited and waited to add to my position but when it cracked down to $3.55 on Monday I said enough is enough and doubled down.

I did add one other new biotech stock this week. Checkpoint Therapeutics.

I say new but I owned this for a week around New Years. I bought it then as a tax-loss selling idea and it didn’t work so I quickly sold. Now I bought it back.

But this time I buy it back with a bit more conviction.

The reason I have some more conviction is Checkpoint released results on their anti-PD-L1 drug candidate.

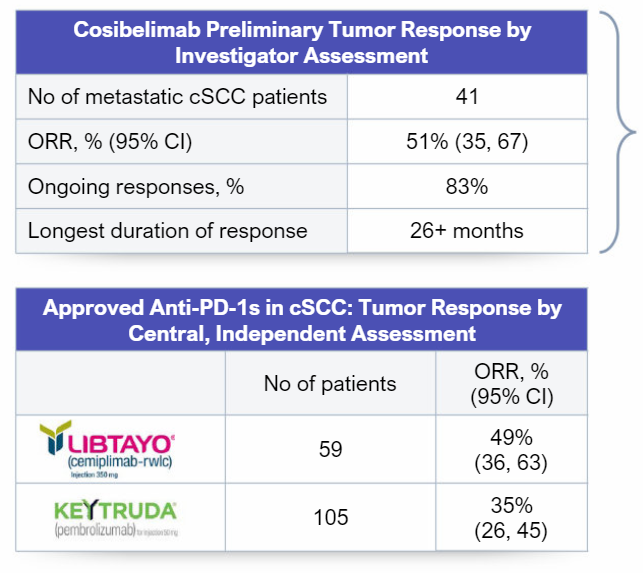

I had said that Cosibelimab had released some interim results previously. Here are those results, followed by the new results:

And here are the new results from the larger patient cohort:

They noted that “the median duration of response (“DOR”) had not yet been reached at the data cut-off point (76% of responses are ongoing)”.

Compare the final results to Keytruda (Merck) and Libtayo (from Regeneron) results. They look pretty much the same, if not better. And the safety profile looks good too. Here is what B Riley says:

we call out that the response rate is in line with or better than the two approved PD-1 inhibitors on the market in this indication, the complete response (CR) rate is trending positively, and the safety profile indicates cosibelimab could be a preferred combination partner

This is how HCW titled their note the day of the release:

Again, this is a very big market. Checkpoint’s strategy is to undercut the big players (Keytruda is owned by Merck, Opdivo by Bristol Myers) on price and take a piece of it:

So I don’t know. Either the analysts are missing something, as am I, or this is just such a bad biotech market that even if you get just the right results, the best your stock can do is stay flat.

But I could be wrong. They do have to muscle their way in against big-Pharma. And its not a better drug, other than maybe the safety profile. Maybe that is what is holding the stock back.

But it also is a very bad biotech market. I’m guessing that it has at least something to do with the latter. I think it is worth a small position, at least for a pop.

Could FOA fears be due to company selling their loans after originating? With spiking inflation, and higher rates, despite short holding period, they might take losses if things get volatile?

And if rates rise significantly, there is probably less appetite to borrow money, so this could hurt their income.

Not saying it isn’t cheap, just trying to come up with ways this can go wrong.

I don’t think so. Originating loans and selling them is pretty much what everyone in the business does. You hedge your rate exposure short term based on the size of the book you hold, which is another reason the financial statements are so complicated.

If rates rise then yes their basic origination business suffers, which is what is happening right now. But the point I’m trying to make is that most of their business comes from these other specialty lending that are not as rate sensitive. FOA is being treated as if it was just a regular mortgage broker and its not.

In fact, I am of the mind that reverse mortgage might actually become more attractive as rates rise because home owners lose some of the ability to use their home as ATM via helocs and have to look for income elsewhere.

I think the downside case has to revolve around reverse mortgage, and it almost has to be a combination of continued slow uptake of reverse mortgages by seniors and a bad business at FOA where they lose market share. From what I’ve read its not super rate-sensitive.

I own Checkpoint and will likely own FOA in the near future, but 2 worries I have:

HCW’s excitement is dangerously close to a red flag for me. I do not have much firsthand experience tracking their recs, but they have a very bad rep among people I respect.

Unless I’m misreading/misinterpreting, FOA’s very large overhang of units will be a drag until they’re converted or otherwise dealt with. It’s a ~$700 million (FD) market cap business, with each FD share backed by ~$2 tangible equity. Given the moving parts, the adjustments, and the huge slug of goodwill (and other intangibles), it’s still very much a show-me (and don’t-write-me-down!) story.

Conversely, the initiation of a dividend might mentally move their earnings from “adjusted” into “real” for potential share purchasers (though it didn’t work that well for, say, Homepoint, which trades at ~.75x tangible equity and is, of course, a different fish).

I think* I know where you are getting the TBV number from and I think it might be higher but I admit its really hard to break it all out.

So I’m assuming you are getting the number from the balance sheet, then subtracting all the intangible assets, just like you normally do.

But I’m not sure if thats accurate because so much of what is on balance sheet is nonrecourse. I haven’t been able to put together a complete picture of what is the balance sheet actually is, ex-non recourse debt, VIEs and SPEs.

So instead I went at it by looking at their March 2021 presentation, where they said they traded at 2x TBV at YE 2020 based on their March 1st stock price. If you back into that to get a TBV at YE 2020 and add the comprehensive income of the first 3qs I get a TBV of about $4.15.

Yeah, that makes sense; I should say that I tried briefly to tease out the exact shape of the BS and had similar (probably greater!) issues and then went to the “guess others’ guess of the beauty contest winner” method.

Basically, I’m trying to figure out what changes the story on FOA. A glancer would say, “oh, wow, 25% of book, profitable,” but that clearly isn’t anyone’s perception now.

Someone digging in a little will say, “unit overhang, massive intangibles, massive adjustments.” That’s where we are now.

A third-level thinker will say, “Net out nonrecourse, etc., to get a true picture.” That’s what the company’s trying to do when it presents, but it hasn’t worked yet; what gets us there?

I think an external validation of the numbers presented is necessary. The main way I can think of that happening is with a dividend that bears some relation to the presented dividend capacity (quite possibly I am gaming the psychology incorrectly, but I feel like a token dividend would not move the needle and may indeed do some harm). There may be other ways they get there–could be that their communications finally start to succeed–but I feel a stable/growing/sizeable dividend is the likeliest, because it’s very “real.” Cooperman’s involvement is a good sign for this, as is the company’s dividend policy: a maybe rather than a no.

On the other hand, on the CC they noted that they are reinvesting in growth at the moment. So it could be a little while.

The complexity here is likely why there’s an opportunity. The challenge is to be confident that it’s hiding something that’s there, rather than something that’s not. Signposts: conversion of units, body language/specifics on earnings calls, dividend initiation (obviously want to be ahead of that), dividend growth. Danger signs: writedowns, new adjustment criteria. I see the likeliest path is this rerates as the picture becomes clearer, which is why I’m likely buying after a little more work (of questionable quality!).

Have you ever looked at TFFP?

I did back when you and that Carlson guy were talking about a potential deal for a vaccine but that didn’t seem to pan out and I haven’t really looked since. Is there something interesting there?

I love TFFP here. It is under pressure from a big seller but fundamentally everything has become better. They are working with Pfizer and have over 30 other programs including vaccines. CEO has overpromised on timing in 2021 but made otherwise great progress.I would happily own it just for the internal programs but there are partnerships coming as well and my bet is Q1.

I decided to sell CKPT again. It continues to be weak and my biotech weighting is to heavy for my liking.

This FOA thing is free falling. Got in at about $3.3. Why are they not buying back stock? Pretty insane to do anything else if they really will earn $200m+ the coming year.

Seems priced to go back to 2019 earnings at this point.

Well the obvious answer is that I’m just wrong and this business is way more sensitive to rates then I thought it would be. Mortgage rates are running high and the stock price is going the opposite direction so I think that is what the market is saying.

I don’t know, but I figure I might as well wait for them to report first at this point. If it is a disaster I’ll sell then. Not adding though.

Peers should be selling off more then though? Not exactly perfect comps, but $COOP and $PFSI haven’t cratered.

Do you think those are the best comps? Both own a lot of servicing, which is going up in value quite a bit with this move up in rates. Maybe RKT or LDI might be better?

Yeah. Honestly Im a bit of a tourist on this stock. Gambling that any sort of positive news will cause a bump at these levels.

At least earnings date is on a Monday and not Friday, so it probably will not be completely terrible?

Interesting lookthrough to FOA reverse-mortgage unit value based on the $75mln EFC paid for the remaining 50% of Longbridge. So ~$150 mln for ~$2.2bln in 2021 originations. FOA did, probably, $3.5-4bln. No doubt not apples to apples but still, maybe $1.20-1.40 of value per share their based on this comp.

Hmmm, yeah that isn’t much of a multiple is it. Looks like 5x net income. A bit weird that they doubled volume with no net income increase YOY? Nevertheless, I’ve been having my doubts about this idea and this just adds to it. Thanks for the info

Actually wait – FOA did $70mm of net income from their reverse mortgage business in Q3 and these guys did $31.5mm for the full year. So is it really $1.50 – $2.00 per share if its the same multiple?

One last thing before I go to bed. Longbridge had negative revenue and negative net income in Q3. Said from marks on loans held for investment and hits to MSRs. Not sure what to make of that.

It seems like a different model than FOA? When I look at the Longbridge 2020 FY results that EFC discloses, all their revenue comes from RM loans held for investment. Their gain on sale in minimal. I’ll have to think about this. So they don’t sell their loans, they hold them against HMBS obligations? Is that what FOA does in some way – I was under impression they sold the loans, took the gain on sale and were done with them.

Real Q, as you noted, is what normalized earning power in each biz is, and how “normalizable” that E is; a 4x on RM’s 2019 #s=~$1.35/share. I actually think finding ~40% of current share price on a conservative/not-fully comparable p/s vs. p/e basis in this segment gives a pretty nice partial floor. It’s a peek into a mirror of a black box that proves somebody smart (I think pretty well of Ellington) sees value there.

I must be missing a piece of your calc. So if I look at the FOA 10Q, Net income before tax for reverse mortgage was $168mm for the 9 months. Annualize that its $224mm. I’m not sure about taxes, looks like 10% – so say $200mm net income. At 4x that would be $800mm valuation. 191mm shares outstanding would be ~$4 per share. How are you looking at it differently?

I was using the year 2019 numbers, a far from perfect baseline even if it’s the most recent “normal” year. RM(/RO) results have bounced around between $28mm and $200MM+/year over the last few years, and so I think a struggle for anyone looking at the co is what annual earnings to assume from this segment. I think the company narrative of being the leader in a vast underpenetrated market is a good one, but everybody likes comps. So the EFC transaction–imperfect as it is in a number of significant ways–provides an anchor. Anyone looking at FOA can say, basically, “At least I know the reverse section is probably worth a minimum of $1.20-1.50 to someone” while building a valuation model.

I am sort of a dumb guy (as should be evident), so this is my “dumb-guy” model, to figure out what somebody else might seeing/missing, and how that could change. Just having that one data point might nudge something from the “too hard” pile to the “worth more work” one. Maybe a silly way to look at it, but my notion was less about specifics of valuation (though that is definitely a consideration) than about whether investors will see it as something that can be valaued at all.

K, fair enough

I’m out of FOA now. Just isn’t working. What can you do.