A Change in the Oil Narrative (and I bought Moneygram)

With the market finally correcting as I had hoped I am sitting in the fortunate position of having large index shorts (via RWM and SH), a few individual stock shorts, a large position in gold stocks and lots of cash.

I am looking for names to add though I won’t rush into it. I don’t really understand the significance of what is occurring in Hong Kong. Until I do, I feel like I am best suited sitting pat.

I did add one name that I spent the weekend reviewing. Moneygram. Unfortunately, the stock is up today even as the market is down, but I decided to take that as a positive sign and bought a starter position anyway. Moneygram fits the bill as being a bombed-out stock with an intriguing upside. In particular, their partnership with Ripple: if Ripple is truly a faster settlement technology it could be quite meaningful to Moneygram.

I will talk more about Moneygram later. What I wanted to write about here was something totally different. Oil stocks.

Its been a while since I’ve taken a meaningful position in an oil producer as anything more than a trade. I took positions in a couple of oil service stocks back toward the December lows that I thought I would hold for the long-run but didn’t (Tetra Technologies and Superior Drilling, both of which worked out temporarily but which I skedaddled from when it became clear the rig count was going to keep falling). And of course, there are the forever fledgling positions in Cathedral Energy Services and Energy Services of America, which I basically don’t look at anymore and just hope for a takeover at some point.

But I have for the most part stayed away from buying oil producers.

The ones in the United States have not made much sense to me as they continue to outspend their cash flow and I remain suspicious about the long-term productivity of the high IP wells from the US shale plays.

The oil stocks in Canada are far more interesting. I’ve watched them all year and they just keep getting cheaper. Recently, I decided to take positions in a couple.

It seems to me that, rather ironically, the Canadian producers are ahead of the curve. They have been forced by pipeline constraints to change their business model from growth to one with a focus on free cash generation. While for the last few years this has led to dismal performance by Canadian oil stocks, I believe that it could soon start to bear fruit.

Why? Well there seems to be a change in narrative taking place in the oil market. If it takes hold it could usher in a new perspective for investors of energy equities and in particular for Canadian equities.

The oil market is complicated, and data is incomplete. As a consequence, the market is usually dominated by one or two narratives that determine the sentiment of investors in the sector. As long as the data is not too much at odds with that narrative, the narrative will determine the trajectory of the commodity and industry that supports it.

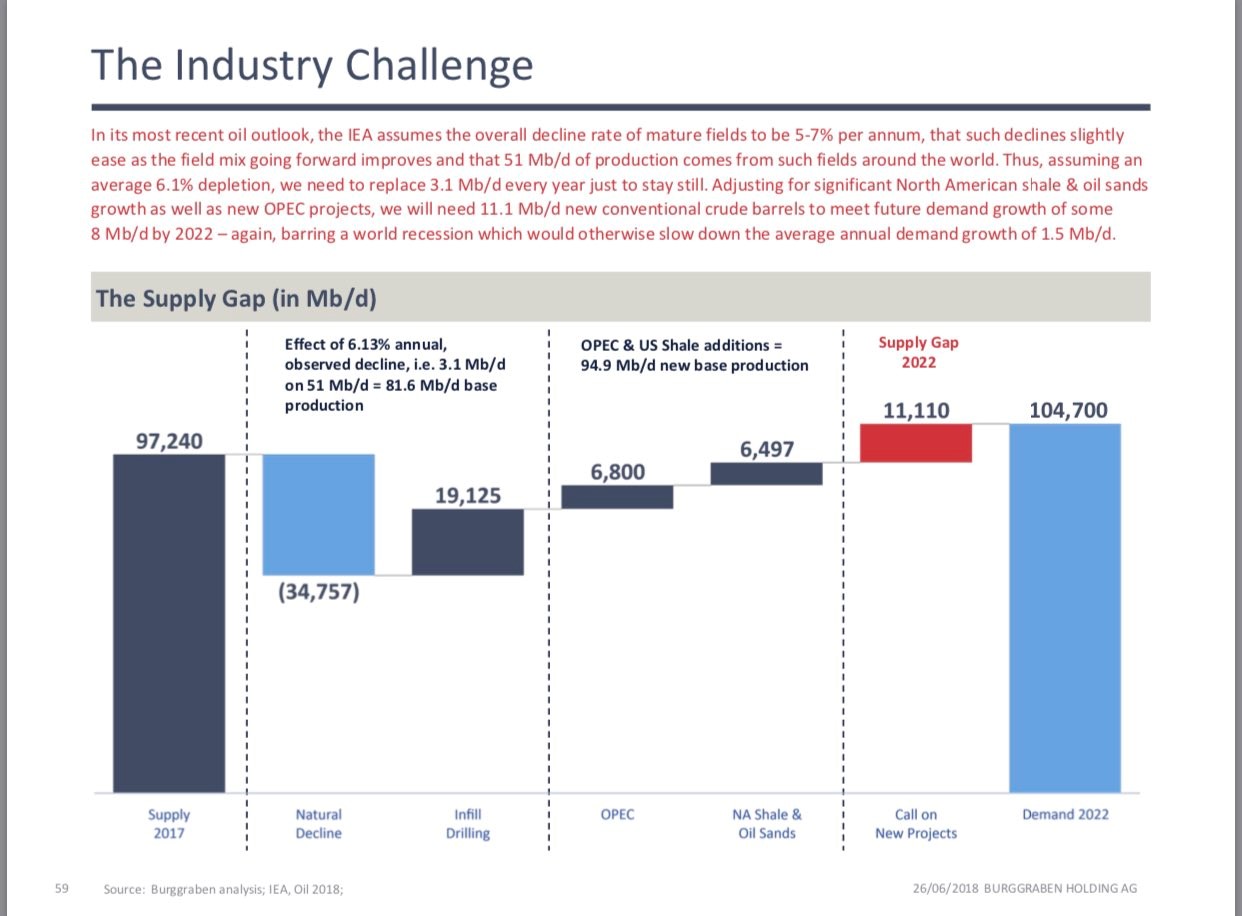

The dominant narrative for some time has been that US shale growth will sop up any demand growth the world requires. Maybe even more negatively, the belief has been that the Permian is so productive, so unstoppable, that producers will continue to increase production unless oil prices are so low that oil stocks are basically worthless.

Thus, it has been that even though the medium term supply gap looks fairly constructive, the believe has been that shale and in particular Permian production will make up any short fall.

While there are several reasons that oil equity prices have been terrible for the last few years, the big one is simply the corollary of this narrative: there is no upside in the price of oil.

The reason that any of us invest in commodities is for the possibility of a big “pop” in the commodity. I sat in gold for nearly a year waiting for the “pop” that we are now experiencing. If there was no opportunity for such a surge, I wouldn’t have bothered.

That is where we are with oil equities.

So that has been part of the story that has gotten us to this. And you can see how important shale additions are and the thought has been that shale will adjust to fill any of the supply gap.

That is the narrative and I think it might be changing. I’m starting to see articles and comments that question shale. Articles that ask whether the “technology” that is supposedly so productive has just been pushing production forward and that the wells drilled are not what was expected once you get past the first 12, 24 or 36 months, particularly in acreage that is not of the highest tier.

There has also been news that the Permian statistics aren’t quite as compelling as thought, that a lot more wells have been drilled then originally thought, and therefore that the efficiency of the overall field is not as strong as maybe it was originally thought to be.

At the front lines what we are seeing are questions about the long-term production of shale basins.

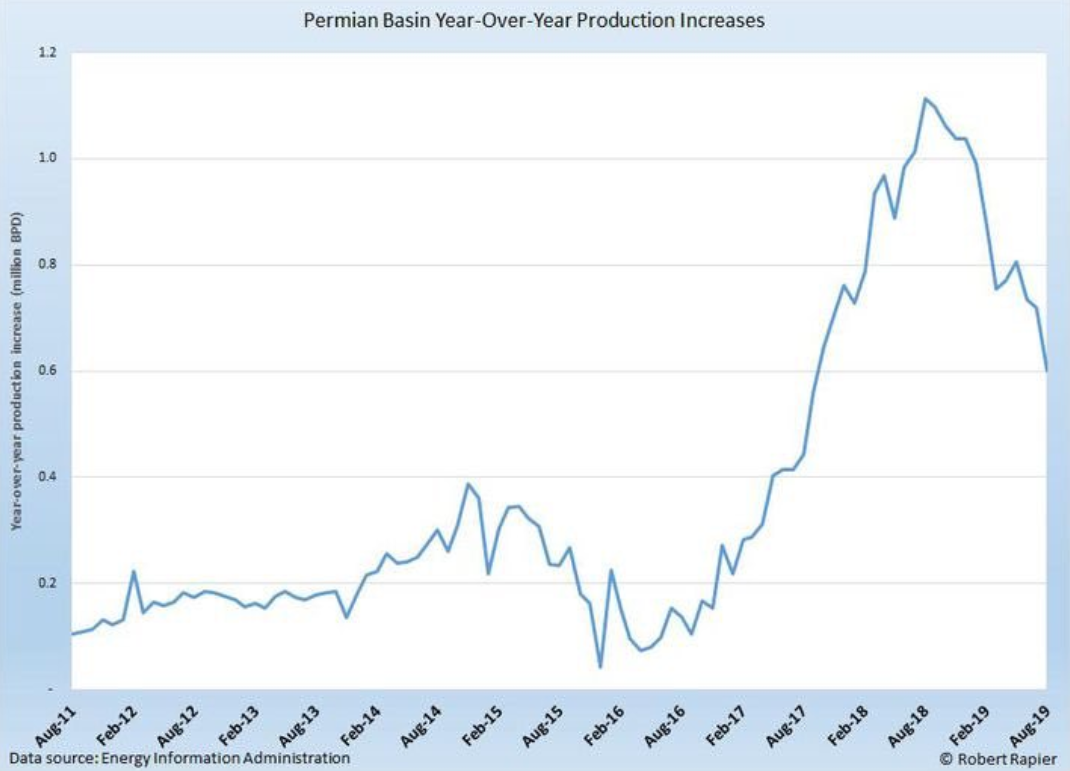

Other articles suggest that the “inventory” of wells is not the vast sea that it was thought to be, that more wells may be producing than originally thought, and that therefore the productivity of basins like the Permian are not as strong as originally thought.

Other articles suggest that the “inventory” of wells is not the vast sea that it was thought to be, that more wells may be producing than originally thought, and that therefore the productivity of basins like the Permian are not as strong as originally thought.

Of course, take all of this with a grain of salt. The Permian remains an extremely productive field and holds many years of growing oil production in the ground. Also, the Permian is pipeline constrained right now so we need to see what happens when those constraints are removed in the second half of this year before drawing too firm a conclusion.

Nevertheless, there is some reason to believe that at the margins, shale is not the panacea it was thought to be.

On top of that US oil companies are beginning to be forced to follow their Canadian cousins and cut back on their unconstrained growth model. Production continues to grow, but that growth rate may have peaked.

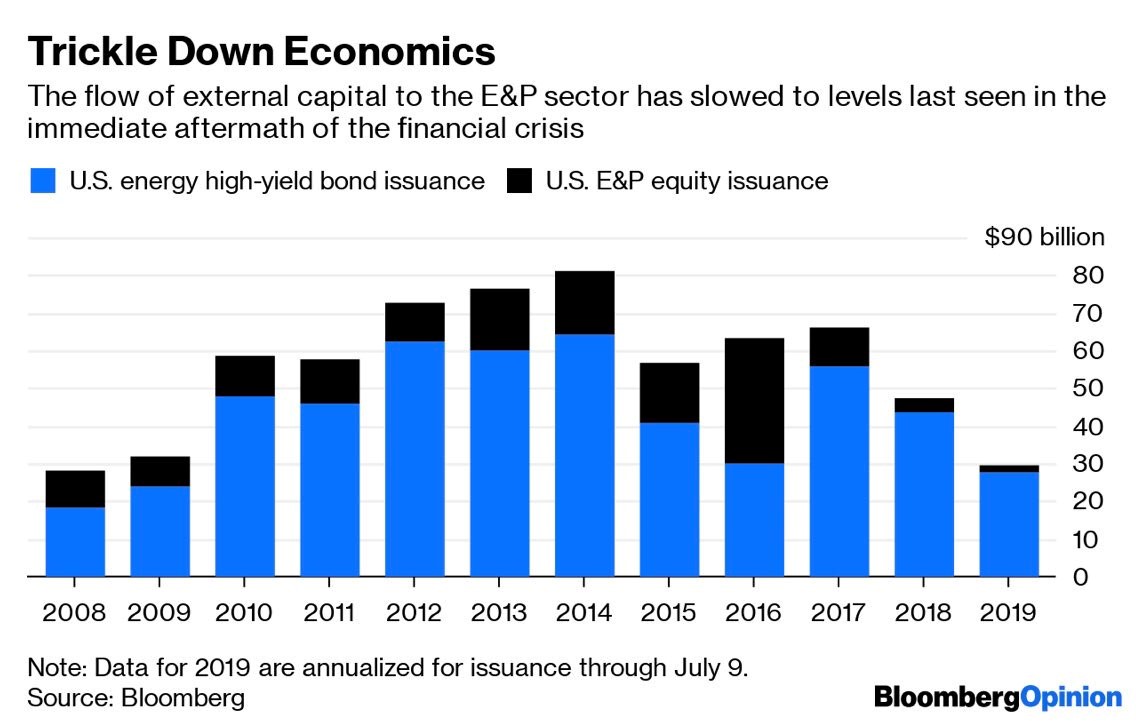

The rethinking of growth seems to be happening because A. the results of non-Tier 1 acreage aren’t as strong as had been hoped and B. because capital is drying up.

Both equity and high yield bond issuance of E&Ps continues to shrink. Private equity, which has been going into the secondary basins and buying up fringe lands, appears to be stepping back and in some cases looking to sell.

The fly in the ointment is of course the global economy. If demand fails to grow all of these signs could turn out to be moot.

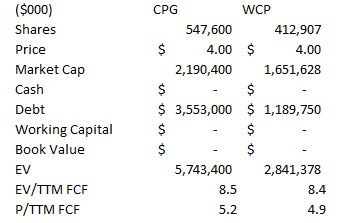

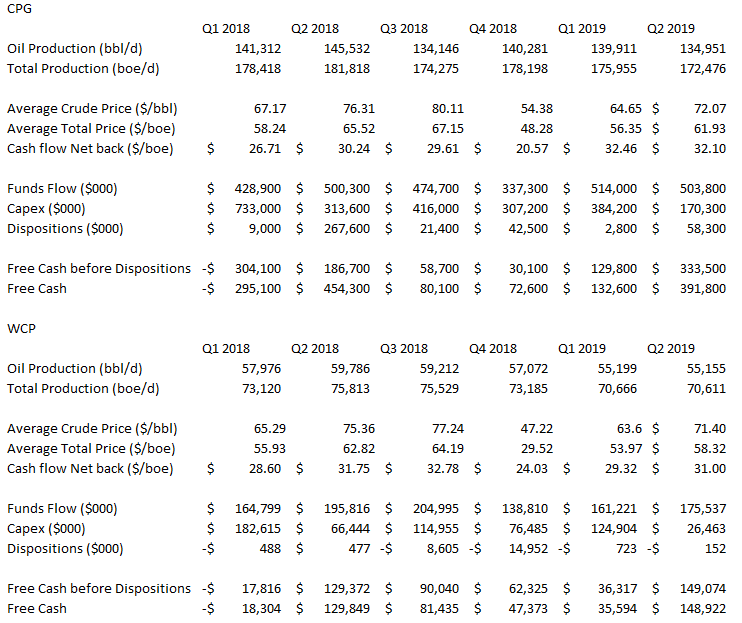

I understand that and will keep this position, like all my positions right now, small. But Canadian oil equities are compelling from a value point of view. Consider the tables of two that I decided to wade into, Crescent Point and Whitecap.

To be sure, there is very little growth here and in Crescent Points case they have been selling off production. But both companies have figured out how to generate free cash (not operating cash, free cash) quarter after quarter for the last year.

While it may seem totally unrelated at first, I was looking at the quarter of Texas Instruments (mainly because it is a stock I am short) a couple of weeks ago.

I was struck by the similarities of the business model of Texas Instruments to the business model of Crescent Point in particular over the last 4 quarters.

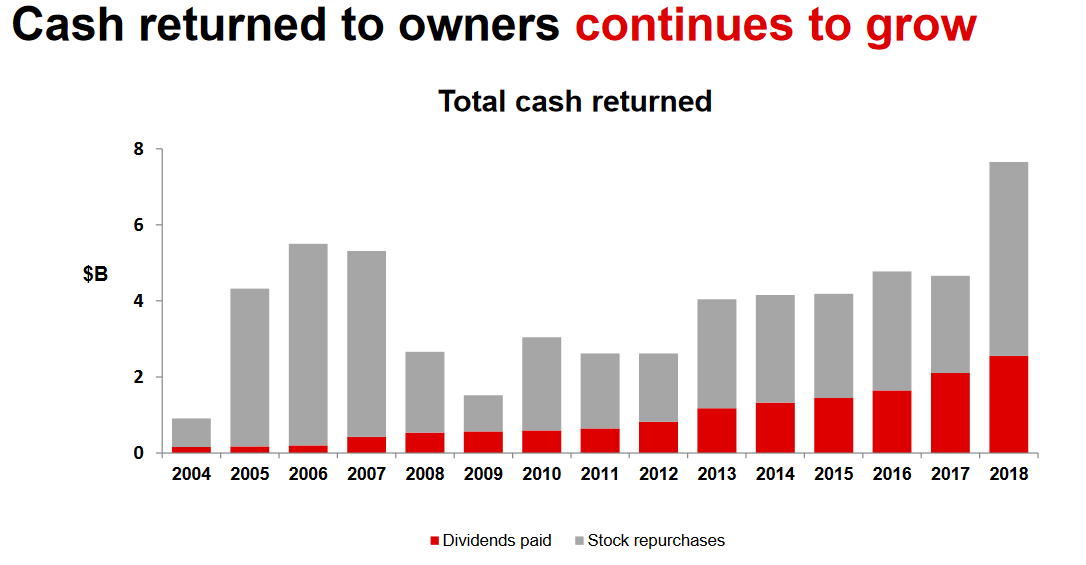

Texas Instruments trades at a 4.8% free cash flow yield, so basically 21x free cash flow. They don’t get the valuation because their business is growing at leaps and bounds. In fact, revenue is expected to decline from $15.8 billion to $14.7 billion in 2019. Even looking longer-term, revenue was close to $14 billion back in 2010, which means growth since that time has been minimal. At best this looks like a 5% growth business over the long-run.

But Texas Instruments gets a reasonably strong valuation because the company has been very good at returning cash to shareholders. In particular, Texas Instruments is excellent at repurchasing stock.

I realize that the comparison is far from perfect. Oil is not technology. But see my point. The Canadian oil producers have transitioned to a business model that emphasizes free cash flow. Now they are beginning to return that free cash back to shareholders by buying up their shares.

This combined with a change in narrative to one where shale is not going to produce unlimited oil, and it could be enough to change the fortunes of Canadian oil stocks.

We are still very early in the narrative change, and as I said it could be totally derailed by a global recession or some other trade induced calamity. So hold your breath.

But if this change in narrative has legs, it, in combination with the newly found free cash flow generation of Canadian oil equities, is worth a bet. I’ve made a small bet and will be watching closely to see how it evolves to determine whether it warrants a larger one.

My man…it’s funny that I bought MGI on Friday after I listened to the call. I also think a MGI/WU long/short could work. Although not as much conviction on the short leg of that trade.

I’m trying to kill the CAD energy thesis and I can’t. I also don’t think anyone really understands the operating cost structure in a strong USDCAD environment. Big fan of CPG, WCP.to and others, no position yet.

Any updates on fiore/superior? Seems like subpar news from both dragging them down, but have not delved deeper

SGI had terrible cost numbers but the stope grades are improving and that is what should matter in the long run. I don’t know what you saw on Fiore, I did not see any news other than drilling results?

Sorry, yeah just the drilling results. Noted about SGI, thank you!

This oil trade basically isn’t working. The builds are too big and maybe just the global economy too weak. I still think I’ll be right about this eventually but I’m out for now.

I retract that. Can’t stay out of this trade, at least in some small size.