Latest Thoughts on Buying Bank Stocks

We are a month into this banking crisis. I still don’t really know what I want to do about it.

It’s why I haven’t said much about it. My opinion keeps waffling. And it depends on exactly which banking crisis we are talking about.

What have I done? Not much. I’ve taken small positions in a few small banks – BSVN, SBFG and EQBK. I’ve bumbled around a few times with the larger regional banks (KEY, MTB, RF) on a small scale, buying each on a couple occasions but chickening out of the positions within a day or two.

While many (including JPM head Jamie Dimon) are saying we are coming to the end of the banking crisis, I’m not sure enough that the coast is clear to buy confidently into these names just yet.

Dimon is likely right though – the acute phase is probably over. At least this particular acute phase is over. The rapid flight of deposits, of bank runs, maybe more importantly the fear of bank runs, seems in the past.

But I made this tweet about what I was more concerned about (flight not fight).

This situation makes me uncomfortable. Maybe more uncomfortable than just watching SIVB and FRC wobble on the precipice over a weekend.

What I don’t like about the “drip” scenario is that there is really nothing imminent. Its just what I said in the tweet – a drip, drip, drip of higher deposit costs for virtually every bank out there, acting like a frog in ever-warming water (is that really a thing?) leading to a slow boil on each incremental loan these banks make.

At least with FRC or SIVB someone had to do something. But with this “drip” scenario no one is really going to care. Except earnings at the banks are going to slip, loan growth will slow then stop and then loans overall will subsequently decline. I’m not really sure where it goes from there except one of my key precepts is that things will turn out ok as long as credit grows and this situation isn’t good for credit which means it isn’t good for things.

As for the banks themselves, it’s really hard to forecast what their earnings are going to be. Almost all the banks seem extremely cheap on last years numbers. And many are now cheap on a Price/Tangible Book. But forward earnings… well I just don’t know.

Banks always talk about deposit beta. That is the portion of Fed Funds that is passed on to borrowers. Last year betas got into the high-teens and low 20s. Last quarter I was seeing estimates that betas would peak in the mid-30s. That would mean on a 5% fed funds rate, deposit rates would get to 1.75%.

But this is for interest bearing deposits. Most banks have a decent amount of non-interest bearing deposits as well. I’m never really sure how the banks are factoring in non-interest bearing moving to interest bearing in their forecasts. I wonder, with the events of the last month, how many non-interest bearing deposits have taken a closer look and realized they have options.

What I do know is that you can get some ugly earnings numbers by playing with higher beta assumptions and especially assumptions that non-interest bearing deposits move to the interest side.

After what we’ve seen over the last month it is almost certain that deposit rates are going higher than they were before. I don’t think 2.5% as a peak is out of the question. That would still be way less than you can get in the money-market.

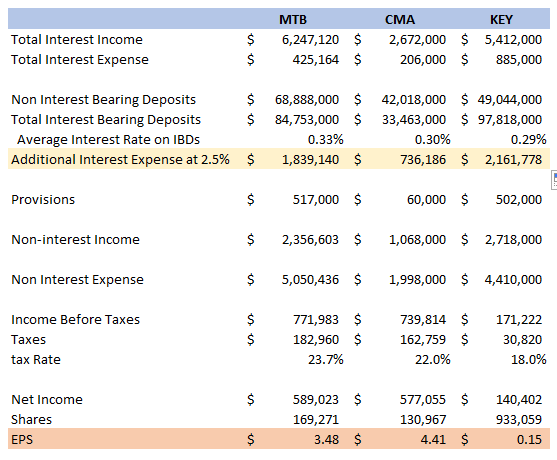

What does that mean for banks? Well, here are 3 banks that I have looked at carefully over the last month. I owned both KEY and MTB on two occasions but didn’t have the gumption to stick with them.

All I’ve done is taken the numbers from the 10-K, looked at the deposit distribution and added the additional interest expense from deposit rates going to 2.5%.

Of the 3, Comerica comes out looking the best. Earnings per share only fall from $8.47 per share to $4.41 per share. MTB sees earnings fall from over $11 per share to $3.48. KEY goes negative.

Comerica looks the best because they have so many non-interest bearing deposits. But is it really realistic that all these deposits stay in that bucket? What if 25% of them go interest bearing?

Those numbers are getting ugly. Key has a loss.

If you really want to get negative, just assume the overall deposit costs get to 2.5%. Each of these banks is suddenly deep in the red. Yikes!

Of course, whether that, or any of these scenarios, happen is up for debate. I’m simplifying a lot here – mostly on purpose to present just how sensitive these banks are to rising deposit costs. But there is bound to be a lot more going on than just deposit betas. And none of this happens overnight. Its gotta be at least another year before deposit costs creep up to this level.

But what happens if this, relatively benign scenario plays out: Inflation continues to come down but it is just a touch sticky. We can’t seem to sustain 2%. We start thinking 3% is best we can do. The economy doesn’t fall out of bed, it does what it has been doing, which is performing pretty, pretty good. The Fed funds is still at 5% in the summer of 2024 and there is no sign they are cutting any time soon.

Man, some of those bank earnings are going to look really bad if that happens.

And that makes me nervous. Because that doesn’t seem like a world in equilibrium.

Maybe I’m missing something, but wouldn’t the bank just raised loan rates and fees to push margins back up? That’s what the Canadian (monopolistic) banks would do. Is there too much competition pressure in the US?

Good question. A couple thoughts about that, applies to Canadian banks too.

First, the essence of this problem is that banks borrow short but lend long. So the deposit rates are going to reset faster than the loans. You can change from demand to a GIC deposit (in Canada) tomorrow but if you have a mortgage you have to wait till your term is up (unless rates are dropping and its actually in-the-money to refinance). Its vice versa for banks.

Take MTB. Their loan book is 80% coming due 2024+. So that 80% is not changing. The part of it that is variable rate changes but that is already in the numbers from last year.

The other 20% of MTBs loan book is either demand or comes due this year. But a bunch of that is already variable rate, so it has benefited from the rate rise.

So I’m not saying MTB won’t see a rise in interest from their loan book. But it will be less than the rise in deposit costs. And if deposit costs rise much further than everyone has been anticipating (which is kind of what I am worrying about in this post), it could get a bit ugly.

Now a bank could kind of double down and grow their loan book at current higher rates to try to outrun the deposit cost increase but that is dangerous and investors will see what they are doing quickly and I don’t think they will be rewarded for it in this environment.

What MTB could* do, and a lot of banks could do, is sell securities. They sell securities and use the proceeds to either A. make more loans or B. buy new securities at higher rates. The problem with this is you are monetizing the loss because these securities books are way under water (which is basically the problem that started this whole debacle of the last month).

But some banks with excess capital will do this. If you read Chris Whalen he keeps hinting this is coming. Banks that can are going to say screw it, let’s reset, sell securities (at a loss), take the big hit up front, reinvest the proceeds at higher rates and preserve their earnings so they can get on with life and not have this drip, drip, drip they are in.

Honestly, I think this dynamic (rising deposit costs, limited things banks can do about it) is why regionals aren’t bouncing back quickly. Its not some fear of a cataclysmic bank run on all these banks. Its like the slow recognition that until we have a firmer grasp of where betas are going to end up, we don’t know the earnings of these banks.

Thanks. That is a very helpful explanation,