Are all the banks the same?

Thursday I tweeted the following:

It seems like pretty much everyone is saying that the regional banks are hooped. You’ve got Chris Whalen saying that ALLY and COF are next. You have Hugh Hendry coming out on Bloomberg saying that its going to get “real bad” and that he suspects “fed officials are considering a lock on bank deposits”. Jim Bianco said on the Forward Guidance podcast that “everyone is demanding their money back right away”.

This is almost no differentiation made when banks are talked about. They are simply referred to as “the regional banks”. All 4,000+ of them (community banks included).

It should thus be no surprise that this last move down has not discriminated much. It has just been an across the board wipe out.

But are all banks facing the same stress?

Here’s what I did last week. I took a bunch of the larger regional banks that provided FY 2023 guidance with their Q1 results and I roughed out the numbers of what their earning might look like.

I kept reading on Twitter that the move in the regional banks was justified because regional banks earnings are becoming so impaired.

So surely this must mean that regional banks guidance for 2023 has come down dramatically? I mean they reported only two weeks ago. And this after the blow-ups of all but FRC. Some of this impairments must be in the guides, right?

I was curious how bad it would be.

I didn’t use any crazy assumptions. I pretty much stuck with A. what the company guided to and B. what first quarter results were.

Here is what those results looked like for two fairly large regional banks that have been hit quite hard in the last week and even harder in the last month and a half: FITB and KEY.

Fifth Third Bancorp

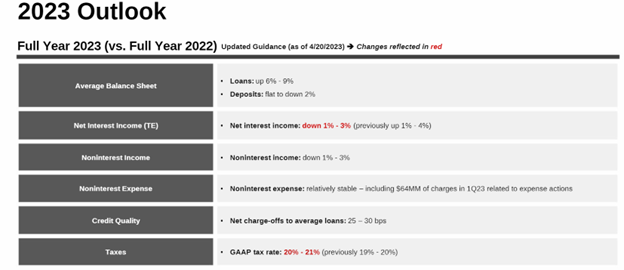

Starting with FITB, here is the guidance they gave on their Q1 call:

Loans up, net interest income up, non interest income up, expenses up.

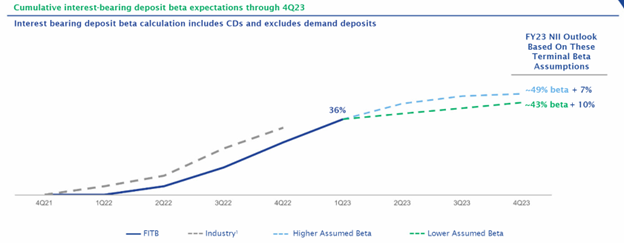

FITB gave the following guidance for deposit betas. I used 45% for my average, which I ballpark is about inline with their worst-case scenario where beta reaches 49% by the end of Q423:

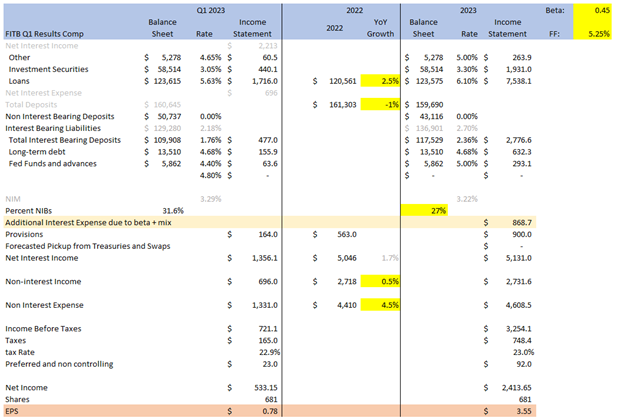

FITB also gave us their average interest assets and liabilities table on Page 21 of their Q1 Earnings Release.

From this information, in the spreadsheet below I essentially reconciled guidance and Q1 results to come up with what earnings would look like to be inline with it all.

I played around with loan and security yields to get something close to the net interest margin growth they guided to (note I ended up with 7.1% vs their 7-10% range).

Bright yellow cells are guidance or estimates. The grey cells are used for comparison but not in the calculations. The cell described at “Additional Interest Expense due to beta + mix” is just the FY 2023 deposit cost less the Q1 2023 deposit cost annualized. I added this calculation to see just how much the additional deposit cost of rising beta and lower non-interest bearing deposits is to each bank.

It is a curious result. All in, FITB earnings come out at $3.55 EPS. Their NIM declines slightly even though their interest-bearing deposit costs rise from 1.76% to an average of 2.36% (because their loans and securities continue to earn more as well).

In addition to the guidance, I assumed provision for loan losses increases as the year goes on (averaging $184mm per quarter for the rest of the year). I also assumed non-interest-bearing deposits decline from 31.6% to a 27% average – which would be consistent with a year-end number of about ~25% NIBs.

Keycorp

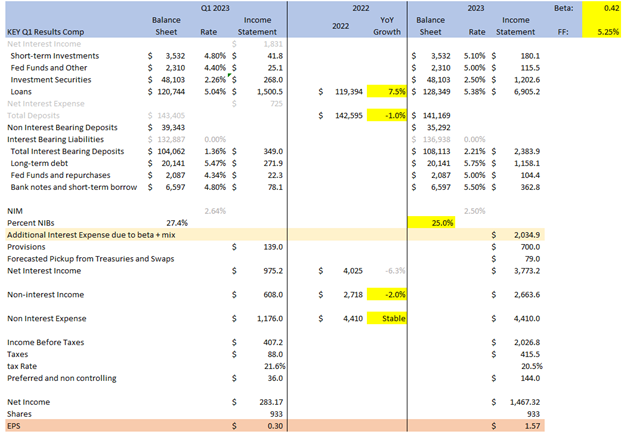

I did the same thing for KEY. Now KEY had a bad Q1. They missed on their estimates and lowered their guide. When I set out to work through what this meant for 2023, I thought the result may be quite ugly. After all, consider Mike Mayo’s comment for KEY during the Q&A:

It’s rough when an analyst is calling you out like that. This was KEY’s outlook:

They lowered net interest income and increased their tax rate.

KEY gave us an estimate of deposit betas “peaking in the low-40s”.

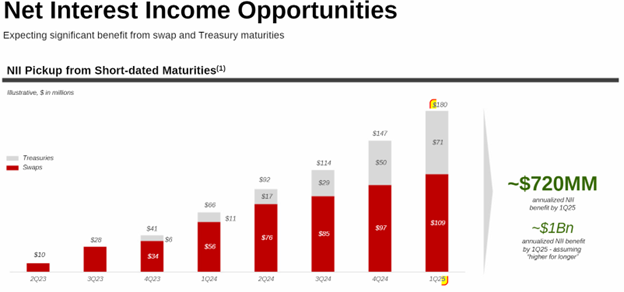

KEY also gave one other data point that is interesting. Below is the impact on net interest income of the rollover of short-term securities. This impact is fairly low for 2023 ($79 million total) but it increases a lot going into 2024. I think it is interesting because much of what we are told implies that the banks will only face rising costs and that they have nothing to offset those costs.

I included this in the line Forecasted Pickup from Treasuries and Swaps.

And here is what KEY’s forecast looks like. Again, bright yellow are their estimates, grey are used for comparison not in calculations.

Surprising. KEY earnings come in at $1.57 per share.

I don’t know, I mean I welcome anyone to go through these numbers and see where they might be wrong. But they are essentially built from management guidance so unless I have a math error, there isn’t a lot else that could be going on.

So I don’t know, what am I missing? Why did KEY fall 10% on Thursday into the $8’s, FITB fall 7% to nearly a new 52-week low? All I saw on twitter was that the regional banks are in trouble and the fall in the regional banks is justified and regional banks are facing deposit runs and regional banks business model is fundamentally impaired.

There are really two things that can wrong with these two banks:

- Their deposit costs could come in much higher than they are estimating.

- Their loan book could have far more defaults.

On point #1, this has to be the biggest unknown. Will deposit costs go up even more? Will betas (measured as deposit costs as a percentage of the Fed Funds rate) far exceed historical norms? This has to be what a big part of what the market is pricing in. After all, deposit costs rose a lot in Q1. Maybe this is just the start.

On the other hand, Q1 may have been the peak for beta velocity. Rate increases have slowed. Beta lags, which means Q1 was pricing in much of the extremely fast rate velocity of late-2022. Will it really just keep accelerating?

I don’t know, but I wanted to look at what happened if beta got really bad. If I add 20 points to the beta of KEY and FITB, bringing it up to 62% and 65% respectively, earnings at KEY go down to $0.61 per share and FITB down to $2.25 per share.

That is a steep decline.

But a 60% deposit beta would be extremely high compared to historical standards. I went back and looked at what banks were saying when they were modeling beta early in the cycle. KEY was saying that 30% was roughly the historical average. FITB said the previous cycle (which did have a much lower terminal rate) was 38%. We are already looking at numbers above that and if it gets to 60%, it would be way, way above that.

Could it really go that high? I don’t know. But this unknown has to be the big risk right now. If there is a second order comment to be made it is that if beta goes that high, the bank earnings get very sensitive to small changes. For example, KEY with 62% beta gives me 61c EPS. At 60% beta its 70c. At 65% beta its 46c.

The other thing that could go wrong is the loan book. KEY and FITB aren’t particularly exposed to commercial real estate (8.9% and 8.4% of total loans respectively). Some regionals, particularly the smaller one’s, have CRE exposure that is so large that really you have to take their earnings with a grain of salt if you think CRE is in trouble.

But if CRE becomes such a big problem that KEY and FITB are stressed by it, there are 3 out of 4 of the banks in the country, including some bigger one’s than these two, that will be in big trouble.

We will see. Going into last week I had a few shorts on regional banks that were A. exposed heavily to CRE, B. had very high and rising deposit costs and C. saw their NIM shrink a lot in Q1. On Thursday I covered most of those and I went long KEY and MTB (I am already long PNC) for a short-term trade.

While this feels like anything but a fat-pitch (I’m not convinced that the worst if over given where the economy is and where it may cause inflation to go and I really have no clue how high deposit costs go over the long-run) it is a trade that worked out at least for Friday. We’ll see if that continues.

The thesis is that A. management isn’t lying about their outlook based on where they see things now, B. that shorts have gotten complacent and are just shorting the regional bank index (KRE) which is dragging down all banks when not all banks are in the same boat. C. nothing in the economy or in their business is deteriorating as rapidly as the stock prices suggest it is.

https://aswathdamodaran.blogspot.com/2023/05/good-bad-banks-and-good-bad-investments.html this should interest you

Thanks Florian

To me the biggest issue seems the deposit beta. This is the most rapid hiking cycle in a long time and we have all the modern tools, like banking on your phone etc.

So could these executives just underestimate the betas?

I mean why would you leave any non material cash in a low yielding account when you can get 5% or so from highly liquid money market funds?

Yeah its the big question. But to give a couple examples. For one, a lot of these deposits are relationship deposits. So KEY for example has a big commercial deposit franchise and those deposits can be the result of loans they made or are connected to a loan relationship. second i wonder how much of these deposits are there because they have to be. There is this assumption that there is all this money floating in banks that is going to be moved but that kinda of implicitly assumes that all the CFOs out there aren’t doing their job. Im sure theres some but I wonder how much. I think FITB said on their Q1 call that 88% of their deposits are relationships utilizing TM services and avg age is 24 years, which means its part of their working capital. Third, on consumer – I know for myself my deposits haven’t changed much at all. The amount i have is enough to cover bills and credit cards for a couple months. And I’m not going to move that out to a money market so I have to manage it back and forth every 30 days to pay my bills. I don’t actually know of anyone who had $50k just sitting in the bank. Usually the amount there is enough to get by for a couple months.

Also this is not new. For sure there is some moving but this is 6 months in. I know i talked with my family 6 months ago and what excess we did have we were all transferring into GICs way back then. This isn’t really a new phenonemon. I got 5% GICs in October.

And why would some of these large banks say they saw inflows in mid-March from SIVB et al when those depositors actually had the choice to put it somewhere else. JPM and BAC don’t seem to be raising deposits much at all. If its really so simple as everyone moving money shouldn’t it effect all banks?

Lots of questions. But Chris Whalen said deposits costs are going to 5% and they are going to have to stop deposit outflows at some point. So I don’t know, who knows?

Gotcha, thanks for this perspective.

I would have guessed there is more really “excess” money in low yielding deposit accounts.

Maybe there is? I’m just giving the other side of it.

I listened to the BWLK conference appearance. It looks interesting. Do you think they need to raise capital at some point?

Yep, love the BWLK story and management. I am confident they will be a huge winner over time.

They do NOT NEED to raise money. They should breakeven soon and not burn cash, a lot of their Citi revenue is paid upfront for example.

That being said, they have been clear to me that they could grow faster with more sales people and capital available. I don’t expect a raise any time soon but if it were to happen it would be bullish. I think they want to raise a little money once the stock is higher and maybe in conjunction with a NASDAQ listing, but they’ll first get on the TSX.

It is one of my top 5 together with PESI, SNIPF, LCFY and LFCR.

MFIN one of those small banks with fairly static NIM and stable deposits. They use broker deposits which “have no right of voluntary withdrawals” and NIM was fairly stable at 8.5%, down from 8.9% Y/Y. MFIN also has a immaterial investment port so no OCI losses.

MFIN actually might have an undervalued port due to its charge off medallions loans, and MFIN collected an outsized amount in the MRQ so potential upside there.

Have you looked at FHN? Could be an interesting trade as the arb traders are dumping it.