Well That’s Surprising

I’ve spent the last 3 posts looking at banks. And it’s not going to stop. Because this is what I find interesting right now.

From post #1 to post #3 my view has changed significantly. I went from ‘OMG this is a disaster’ to ‘you know some banks should hold up okay’ to ‘its really weird how big the gap there is between what the stock price is doing and what bank management is guiding to’.

All the time I scratch my head and wonder how it will end?

My next installment is a ‘well that’s surprising’ post. That is to say: ‘well that’s surprising’ that one of the banks at the center of the maelstrom actually doesn’t look like a complete disaster even when I model it out in very stressed scenarios.

The bank I’m talking about is Western Alliance Bancorporation. Its right in the middle of this. RIGHT in the middle. It was hammered down to single digits when Silicon Bank went belly up, it was hammered down again when First Republic went belly up, it was bought by Chris Whalen at the peak of the crisis and then sold by Chris Whalen at what is now being called the Whalen bottom. You couldn’t be more in the middle.

Now I just want to preface all this by saying I don’t own WAL. I have no intention of owning WAL. My conclusion is that they are at best walking a tight rope. And they aren’t all that cheap compared to other banks out there given the potential for further distress. So don’t turn me into a WAL bull.

But the way the stock performs (absent the rally this week) you’d expect things to be extremely dire. What I found instead was that things were more like ‘not great’.

Like I said in the last post, as much as anything I’m putting my thoughts down for my own record – so I can go back and say ahh, that’s what I missed.

Onto WAL.

WAL is interesting for a few reasons. First, this is not a security heavy bank. They aren’t like Silicon Bank with massive MTM losses on Treasuries and mortgage-backed securities.

Second, WAL originates loans with a pretty high interest rate. The average rate on WAL’s loans in Q1 2023 was 6.28%. Compare this to say Keycorp – which had 5.04%.

Of course, that means that WAL loans should be riskier. And they probably are. But right now, with the economy still apparently trucking along, that riskiness isn’t bearing out into much higher loan losses. So in a weird twist of fate, banks like WAL look better, at least on paper, because their higher rate loans can cover the rise in deposit costs better.

For WAL, the combination of high-rate loans and a relatively small portion of (low-rate) investment securities means that their net interest margin was not terrible in Q1, even though their deposit cost rose a lot.

Now that is going to get way worse in Q2 and beyond because WAL has seen an outflow of deposits since. To plug the hole they are tapping higher cost sources of deposits (or the Fed) to replace them.So far, no surprise. This is where you would expect disaster. Higher deposit costs, a collapse in net interest margin, a general mess.

What surprised me is that when I look at WAL and put some fairly significant stress on their deposits, I don’t get a complete disaster. It is not exactly rosy, but it wasn’t nearly as bad as I thought it would be.

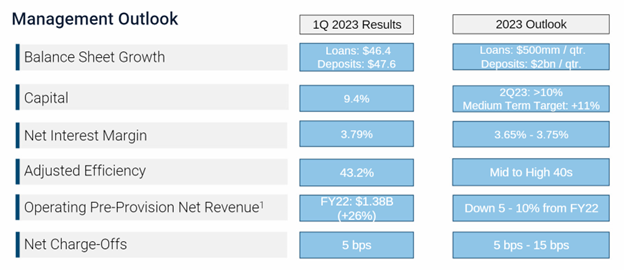

My assumptions started with management guidance. Take that FWIW.

I tried to stay consistent with WAL’s loan growth and deposit growth estimate. These are two things that management can control.

I did not follow management guidance for net interest margin, efficiency or pre-provision net revenue estimate because I wanted to assume much higher deposit costs, which throws off all of these metrics.

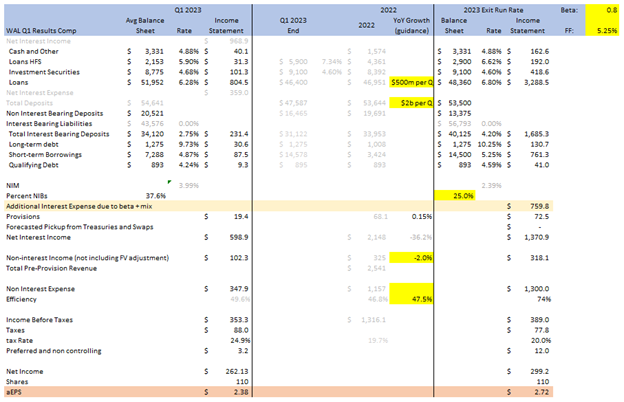

Essentially, I am assuming that WAL can build back their deposits but at a painful price. The key assumption I’ve made, and really this is just a guess, is that WAL has a deposit beta of 80% by the end of the year. That means that if the Fed keeps rates at 5.25%, WAL will have deposit costs of 5.25% x 0.8 = 4.2%. Which is pretty high.

Below is what I get for earnings. Now this is kind of a pseudo-run rate on earnings. I’m not trying to come up with a 2023 number or a 2024 number. It is more of an annualized steady-state look of where things could be at YE in a distressed scenario.

It is not great, but it is not terrible. Of course, to put it in context, WAL made almost $10 EPS last year. So it is a massive drop in profitability. But they are still profitable, which is more than I would have expected.

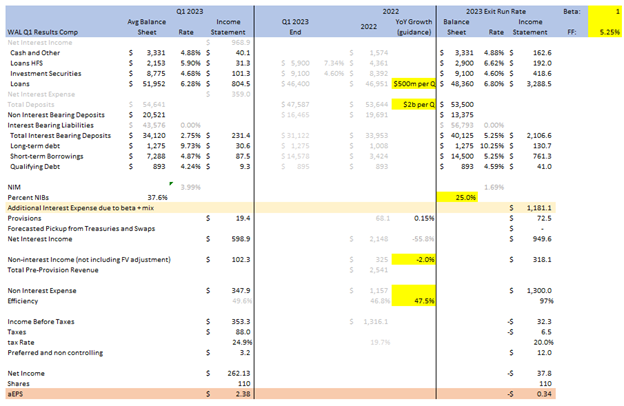

Next, I assumed the absolutely apocalyptic case where deposit costs go right up to the Fed Funds rate (Beta = 1). In this case, as you might expect, EPS goes negative, but surprisingly it is still less than a $1/share loss. I would have expected much worse?

Why are these estimates are better than I would have expected? I think it comes down to WAL’s high interest rate loans that can cover the deposit costs (and most of the other non-interest expense) even when those deposit costs are through the roof. WAL also has a strong mortgage business that delivers fee income (their non-interest income was $100 million in Q1).

There are plenty of caveats to consider with these numbers. For one, I am not thinking about credit quality at all here. If WAL’s loans start to go south, things would fall apart quickly.

WAL has also entered this hyper-sensitivity zone where the numbers are extra sensitive to changes in assumptions as you get closer to break-even. It becomes a precarious tight rope. For example, if non-interest bearing deposits drop to 20% (instead of the 25% I assumed), EPS drops to $1.90 and -$1.37 per share for the two scenarios. It doesn’t take much for things to spiral down.

Which is why I am absolutely not saying WAL is a stock I am looking to buy. I mean it would be trading at >10x earnings on my 80% beta stressed case. That situation is not implausible. There are plenty of banks that have lower PE’s without all the distress and certainly not the battleground element.

Nevertheless, it strikes me as interesting that even with a battleground stock and what should be some very extreme assumptions, I don’t get a complete disaster of a result. Surprising!