Every quarter I spend an evening or two going through the reports of the 15 or so gold stocks that I follow and updating a spreadsheet that I use to track their progress and compare them against each other.

I do not use the spreadsheet in the way a strict value investor might. I do not search out and buy the cheapest gold stock of the bunch on a cash flow metric or per ounce metric. I do look for value, but I also look for growth. The stock market tends to treat gold producers in much the same way they treat any other business: stocks with superior growth potential get bid up to higher valuations. On the other side of the coin, you can sit on what appears to be an undervalued producer for a long time if that producer has a poor pipeline of projects or has no prospects to produce near term incremental ounces.

I did exactly that recently with Aurizon Mines. I was attracted to the value, it was cheap compared to its peers, it had a lot of cash on its balance sheet and no debt, and they have a well run and profitable operation at Casa Berardi. Yet Aurizon does not have a strong growth pipelne. Its closest to completion project is an open pit prospect called Joanna which, while it could one day produce a lot of gold, has been stuck in the feasibility stage for more than a few years and has the worry of requiring a large capital outlay out front. When you add that to a number of fairly early stage exploration projects the result is a company without the near term potential to grow ounces significantly. I sat on Aurizon for almost 6 months based on its value story and the stock went nowhere.

At the other end of the spectrum is a company like Argonaut Gold. I owned Argonaut Gold for a while last fall but sold out way too soon. I sold because I saw the stock was priced dearly compared to many of its peers. However I failed to adequately account for the growth opportunities. It was a silly oversight; I had originally bought the stock because of the low capital cost heap leach projects that they could bring to market quickly. Somehow though I forgot about this, got caught up in the valuation and that led me to sell too early. The stock has since doubled to $10 before pulling back in the recent carnage that has brought all gold stocks to their knees.

When I was looking for gold producing companies a couple of weeks ago I was on the lookout for the next Argonaut Gold. Unfortunately I have not been able to find them (if you have some ideas, please drop me a note). In my opinion the closest comparison to Argonaut in terms of near term low capital cost growth potential is Atna Resources. Atna has a legitimate chance of increasing their gold production from 40,000 to over 150,000 ounces in the next couple of years. What makes Atna an imperfect comparison is that most of its projects hover around the cash cost level of $900 per oz, which is on the high side of the cash cost scale, whereas Argonaut has been able to achieve the double whammy of low cash cost low capital cost growth.

A second producer that I have bought (back) recently is OceanaGold. I have had good luck with buying OceanaGold when the market hates them and selling when the market starts to show some love. This time around I may hold on for a bit longer. OceanaGold has typically been one of the cheapest gold stocks on cash flow metrics. This is because, in part, they have struggled with costs and production at their existing mines. However, their soon to be producing mine in the Philippines (Didipio) will bring about some growth to the company, and perhaps more importantly, it will reduce the corporate cash flow numbers substantially.

One thing that got me interested in OceanaGold again was my research of Agnico-Eagle (which by the way is the third producer I own right now). While Agnico-Eagle has had some difficulties with the closure of their GOldex mine, they remain one of the best growth stories in the industry and I believe the market will come around to forgetting about Goldex and recognizing this once again. Agnico-Eagle owns 5 operating mines. Of those five, one mine, Meadowbank, produces about 1/3 of the production. At the corporate level, Agnico-Eagle has reasonably low cash costs. They were $594 per oz in the first quarter. However Meadowbank, the largest mine, has cash costs over $1000 per oz. On its own its a marginal mine that produces a large number of ounces. Together with the other low cost assets that Agnico has, it receives a much higher valuation than it would on its own.

I liken this situation to the one at OceanaGold. At OceanaGold, the corporate level cash costs should come down fairly substantially with the introduction of gold production from Didipio. Didipio will produce a lot of copper in addition to its gold, and this will make the cash costs of the project appear to be quite low. The cash costs of OceanaGold will not get down to the level of a company like Agnico-Eagle (the high cost mines at Oceana will continue to make up too much of the production) but I do not see it as unreasonable to think they will drop into the high $700 range. My bet on OceanaGold is that when production begins at Didipio, analysts will begin to revalue the company on the basis of a mid-cost producer rather than a high cost one, and that should provide for some upside in the stock.

I updated the spreadsheet below over the weekend. I did not update it during this week with stock prices for each stock tabled. The prices are as of Friday’s close. There has been so much movement in many of these gold names in the last couple days that the prices are already somewhat outdated.

My hope with gold and gold stocks is that this move is for real. What I think we need to have for this move to be real is action out of Europe that brings gold back into the system. I wrote this weekend about how, in general, the turmoil in Europe should cause weakness in paper currencies and lead to strength in gold. On Sunday Donald Coxe was interviewed on King World News and decribed a scenario whereby gold would be used along with a value added tax as colateral for euro-bonds on ther periphery. While I am a bit fuzzy on what the details of such a bond might be, I believe that conceptually this is the sort of event that has the potential to create a great rally. On the other hand my enthusiasm is tempered that if nothing is done in Europe, and if the Federal Reserve does indeed decide that QE is not working (I don’t think its nearly as clear as others do that the Fed will mindlessly embark on further quantitive easing. The Fed is, after all, a data centric institution, and if it appears that the benefits of QE are not what was anticipated, and I believe that has been the case, they may decide that a third installment is not beneficial).

Donald Coxe had a very good conference call last week. To be honest, I think his calls have been pretty boring for the last 6 months. He doesn’t have any better grasp on the Euro-crisis then anyone else, yet the situation in Europe is of such a systemic nature that any insight he provided on anything else, always became prempted with the caveat: Assuming all goes well in Europe.

Well last Friday he broke from this mold and made his first endeavour into the terrain of bullish sentiment in some time.

His reason?

The banks.

The main reason for his bullish outlook is the outperformance of the regional bank index, the KRE. As Coxe said:

When you get 3 months of outperformance while the S&P is itself recovering that is a powerful sign that the market has digested the bad news and that things will get better.

The KRE has indeed been outperforming.

I must admit, I’m tentative to proclaim my outright bullishness just yet. Tto be fair to Coxe, he qualified his own bullihs stance by pointing out that there was still a lot else that had to go right for the bullish call to play out.

I do admit, however, that the signs are beginning to accumulate. Jobless claims are trending down, the ISM is looking more stable, news out of China (particularly that inflation has fallen) is starting to sound more positive, and heck, even the Italian and Spanish 10-year yields are trending down at the moment.

So what do you buy if you are bullish?

Well, on the conference call Coxe proclaimed (once again) the supremecy of the commodity stocks. A bit of a broken record is he, but why stop with what works. Well I am long oil, long gold, thinking about how I might get long copper or coal (but more on that below). I have those bases covered. Perhaps the more specific question you might ask, is what does one buy when the KRE is outperforming?

And the logical answer to that?

…buy the regional banks

I’ve been accumulating the shares of a number of regional banks over the past few months. What is my thesis?

The lows of August felt like a bottom

There is volume in some bank stocks that typically have had no volume whatsoever (is somebody starting to care?)

The housing market in some regions is bottoming

The write-downs at many of these banks has peaked

How much further below book value these businesses can go?

I’ve been listening to this mortgage broker and originator podcast called Lykken on Lending on my bike ride into work for the last 3 months. Its interesting stuff. The first thing that’s interesting is just how intertwined real estate is with regulation. They actually have a regular segment on this show that is dedicated to new legislation being considered by congress or the senate. Its crazy! Second thing that is interesting; there is starting to be some signs of life in the mortgage market. For the first time we are seeing private lenders getting back into the game. They had a company on a couple weeks ago that was funded by Lew Raneiri (the godfather of securitization) and that is looking for loans that are just below the level of what passes for the GSE’s.

It’s starting again!

In this short clip below, Jim the Realtor, prominently featured on CalculatedRisk, makes out the bull case for a barn-burner spring. Says Jim: “I think we get into spring time – if rates are still this low – it’s going to be a real frenzy.”

Kyle Bass and MGIC

Another favorite of mine, Kyle Bass, recently bought a large stake (just under 5%) in MGIC. I stepped through MGIC over Christmas and will review the work I did another time, but to make a few brief conclusions I determined the value certainly might be there but I just don’t understand the business (the mortgage insurers are hugely levered companies with massive amounts of housing liabilities against them) well enough to pull the trigger. Specifically, the solvency of MGIC and the rest of the insurers seems to depend as much on the ability of the insurers to mark their liability per payout (in other words how much they owe for the foreclosure they insured) as anything else, and that appears to be a bit of black magic to me.

Nevertheless, MGIC has moved substantially higher since that time, something that seems unlikely if the housing market were about to (triple?) dip again. Here is what Bass had to say about MGIC and the housing market a couple of months ago. From the WSJ:

Mr. Bass said that while the housing market was still around two to three years from firmly “bottoming out,” he said any future price declines would be quite modest. “I don’t anticipate a huge decline,” he said.

I think he’s right. Residential housing is closer to a bottom then a top. And its bottomed in some markets.

The Housing Market Turns?

Residential housing is the lifeblood of most regional and community banks. A turn in those markets could turn the fortunes of these companies.That’s why I’ve picked up shares in the following stocks over the last couple of months:

Oneida Financial (ONFC)

Bank of Commerce Holdings (BOCH)

Atlantic Coast Financial (ACFC)

Community Bankers Trust (BTC)

Apart from Oneida, these stocks are not for the faint of heart. I know there are plenty of well capitalized but fairly valued banks out there that can return you 10-15% per year in all likelihood. I want a bit more than that though. So I am willing to step out on the limb a bit further to get it.

Xenith Bankshares and the problem with RBC practice accounts

I’m going to get into Xenith in a second but first let me say something about this RBC practice account.

Great idea. The idea to be able to put fake money into an account, to have it count commissions and to be able to make buys and sells in real time is super.

The problem lies in the execution. First there was the problem placing orders. This started back in September. I wrote them about it. They said they would fix it. They wrote:

Here we are in January, I still have to do this clugey workaround where before I can place an order I have to start it through my margin account and then at the last step switch the practice account.

Now, just yesterday, another problem. Apparently I can’t place an order for select NASDAQ stocks. In particular those that are NASDAQ:CM (capital markets). This just started. I phoned RBC. Luckily I’m on their gold plus customer plan or whatever its called so I get some service. They look into it, see what’s wrong, but now they have to send it to their “back office people” to fix it.

We shall see.

Thus it is that while I own XBKS, I do not own XBKS in my practice account. I don’t know when that will happen. If any of my readers knows of another better service for tracking a mock portfolio, please email me.

Anyways, that’s the story, onto the stock.

My latest bank pick: Xenith Bankshares

Xenith Bankshares is a community bank centered out of Richmond Virginia.

The bank specalizes in making commercial loans, which make up some 88% of their loan book.

Xenith was involved in two transactions during the summer, buying banks from two other distressed Virginia lenders (Paragon Community Bank and Virginia Business Bank or VBB). In the case of VBB, the bank was bankrupt and the transaction took place through the FDIC. In the case of Paragon, Xenith just took over the Richmond based operations of the banks. In both cases, the company is only responsible for the performing loans on these banks books.

The history of Xenith and these two transactions have already been written up in two excellent posts on a website called Frog’s Kiss, here and here. I will not dwell on the details of the bank to much further, because all the information is there.

Why Xenith?

Xenith is aggressively growing their loan book in Virginia, both through transactions like the above, and organically through new loans. They have done a good job of making loans, and so far nonperforming assets are not a significant threat.

And yet you aren’t paying much for this growth. The company has a tangible book value of a little over $65M, whereas at the current share price of $3.70, the market capitalization is a little under $40M.

Why so cheap?

Well for one, the bank isn’t profitable yet. Xenith has been losing about $1.5M per quarter all in for the last couple of years. For two, it is a bank and after all no one wants to own a bank, right?

Of course that might be about to change.

Part of the bet here is that the management at Xenith can integrate these recent transactions and bring their profitability up to the company’s standard. The company was created originally with a takeover of First Bankshares. This was a sleepy little commercial lender that had a fairly weak interest margin. The management at Xenith have been successful in increasing the NIM significantly since that time (see below). The expectation is that they will do something similar with the newly acquired loan and deposit base.

The second part of the bet is that Xenith has a lot more room to grow. The company’s tangible equity (as noted above), is about $64M. Loans and securities and other risk assets are about $360M. So the company is only employing about 6x leverage. They should be able to raise this to around 10x over the course of the next year.

If they do, and are successful in their lending endeavors, you might expect the company to deliver a return of somewhere around 1% to 1.5% return on assets. Taken another way, you might expect the company to deliver somewhere between 8% and 12% return on current equity when its all said and done. Projecting either of these metrics leads to a fairly cheap earnings multiple (somewhere between 4x and 7.5x earnings depending on their success. This suggests that as this plays out over the next couple of years, you could expect the stock price to at least double (and optimistically quadruple if the banks become loved again) from current levels as they move ahead.

Gramercy Capital: CDO-2005 passes the over-collateralization test?

With Gramercy, as much sleuthing that I am doing of the company, I feel like I do almost as much sleuthing of other investors. With Gramercy, one of the best to follow is PlanMaestro. He posts a blog called Variant Perceptions, also posts on yahoo, investorshub, and corner of berkshire and hathaway. In this case the relevant piece comes from the latter. Says Plan:

Jameson Inn was already written off 100% for OC purposes and CDO 2005 passed again its most recent test .

As those of you that read last weeks letter would know, I pointed out that CDO 2005 was unlikely to pass any time soon if it was only curing its undercollateralization with interest payments. To have passed again, one of two things must have happened.

About $100M of the assets held were paid back, with the proceeds being used to pay out the senior CDO holders

One of the written down loans began to reperform

To discuss the possibility of the latter, there was news this week that the Vegas Hilton, which is in receivership and which has been 60% written down by Gramercy in CDO 2005. For some time now Goldman Sachs, which holds the mortgage on the LVH along with Gramercy and another party, have been trying to convince the courts to let them run the hotel and gaming operations while it goes through the foreclosure process. The problem is that the gaming license is owned by the previous owners Colony Resorts. Colony Resorts had been fighting back saying that if their gaming license was used by the receiver, they could be liable without having any oversight control.

The issue was very recently brought to the court, which ruled that the receiver would only have non-gaming authority. But then the Nevada Gaming Commission passed its own contrary verdict, allowing for the casino to operate under the existing license. The matter went back to the courts and just last week news came out that the ruling was in favor of Goldman.

Given the information I have, I can only speculate that this contributed to the change in the collateral test. The loan sat on the books of CDO 2005 at about $29M as of March. It was apparently written down 60%, though I have no confirmation of that figure. CDO 2005 was about $18M short as of last October. Putting that all together, it seems very unlikely the loan could have had that big of an impact on the collateral test. Still its an interesting exercise to go through, and a positive development both that the CDO 2005 is now passing, and that the LVH loan is likely accruing some interest again.

Argonaut Gold Pulls together a Strong PEA

This whole short Argonaut Gold trade didn’t exactly work out.. In fact, I don’t know what I was thinking. I need to start reading my own press clippings.

To recap, two weeks ago I shorted some Argonaut against part of my long of Aurizon Gold. My reasoning was that if gold continued to fall Argonaut, being much more highly valued then Aurizon and at the same time having less cash, would have further to tumble.

I’m a little embarrassed that I made this suggestion. It was only two months ago that I had been arguing that Argonaut was one of the better gold stock investments out there. I had it right originally. That thesis, which is available here, was that Argonaut had very strong growth opportunities and those growth opportunities could be accomplished with minimal CAPEX. If there is one thing the Street loves, its growth. If there is another thing the Street loves, its not having to put up a bunch of cash up front to get that growth.

Today the company released the PEA it had completed on the La Colorada project.

The PEA showed the following highlights:

Initial Capital Expenditure for the project is estimated at $14.5 million with a Sustaining Capital of $11.7 million.

Operating costs of $620/oz over the LOM, including $1.50/t mining costs, $2.36/t processing costs, and a 3.4:1 strip ratio

Gold equivalent production of 53,000oz per year over 9 years

Pre-tax Net Present Value (“NPV”) of $278 million using a 5% discount rate at $1500/oz gold

Overall the numbers would be mediocre if it were not for the capital costs, which at $14.5M is chump change for a project this size. This is even less than the my estimate of $25M to which I commented: There are not many companies that can boast near term production potential with so little up front costs.

When I had shorted Argonaut against a portion of my Aurizon long it was with the idea that the quarterly results might show disappointment and the idea that the gold price might be susceptible to an even bigger pullback. El Castillo has underperformed the last couple of quarters, and with a mine that is of as low a grade as El Castillo the operators run a very fine line between success and failure.

That could still be the case, but having witnessed the stocks continuing rise I am reluctant to wait and find out. I got out Monday when the PEA came out. At this level ($8) the stock is too expensive to buy. I have to just admit I made a mistake by selling it in the first place (I owned both Aurizon and Argonaut back in October, but sold Argonaut after poor 3rd quarter results), and move on.

Is Aurizon a Value Trap?

How bad was that decision I made back in October to sell Argonaut and hold Aurizon? Well, I owned both stocks until the middle of October, when I sold Argonaut after less than impressive 3rd quarter results.

[cid:image001.png@01CCD208.8AEC6020]

This is a painful chart for me to look at.

Nevertheless, pain is a necessary condition of learning, and it helps some time to agonize over your own stupidity for a while, just so that its really grilled into you not to do the same thing again.

With that in mind, what did I do wrong?

Aurizon Mines: Visions of Joanna someday

In contrast to Argonaut, Aurizon does not seem to be in much of a rush at all to bring Joanna into production. This timeline says it all:

May 12th 2008

Aurizon first commissioned a pre-feasibility study on Joanna.

November 11, 2009

Aurizon finally received that pre-feasibility study and proceed to a full feasibility study.

Aurizon delays the feasibility study for Joanna again, saying: “the projected capital and operating costs appear to be significantly higher than previously anticipated. The increased scope of the project, as a result of the expanded mineral resource base, has increased capital costs, including those associated with an autoclave process. The costs of ore and waste stockpiles, tailings and of materials and equipment have also all been trending higher, along with the gold price.”

January 11, 2012

Another update giving an ETA: Feasibility study work on the Hosco deposit will continue in 2012 with completion of the study anticipated by mid-year. The feasibility study will incorporate a reserve update based on the increased mineral resource estimate announced on June 13, 2011, together with results of metallurgical pilot tests, a geotechnical study, updated capital and operating cost estimates, and other relevant studies.

Its been almost 4 years since the original pre-feasibility study on Joanna was complete! At this rate they should be mining by 2100.

As is obvious from above, there have been some metallurgical difficulties with Joanna. Was I too optimistic with my analysis?

To compare, the original pre-feasibility study assumed $187M in CAPEX. The operating costs were estimated at $434/oz. My analysis assumed $215M CAPEX, and operating costs of $717/oz. I think I have been safely conservative on the operating costs. I may turn out to be less so with the CAPEX.

The more fundamental point is that when I invested in Aurizon I strayed from my usual criteria for choosing mining companies in a couple key respects. Both of these have come back to haunt me:

A. Look for miners with a strong pipeline of growth. The market likes growth. It does not always appreciate value. The reason there is supposed “value stocks” is because the market does not appreciate value in itself.

B. Capital costs must be low and mining methods must be simple. The best mine to invest in is a simple heap leach deposit. High capital costs tend to get higher. Complicated mining and recovery processes tend to underperform to plan.

So what am I going to do about it?

Unfortunately there is not much I can do. Argonaut is $8 and Aurizon is $5. Most of the move in AR has been done. I’m not going to chase it at this point. Aurizon is probably much akin to OceanaGold, which I have played much more intelligently by buying the stock at $2.20 and selling it at $2.70 again and again. With Aurizon those numbers are probably around $5 and $6. Indeed I did sell some Aurizon around the $6 range the last time it was there but I think that its time to recognize that without a strong feasibility study for Joanna, that $6-$7 is about all you can expect here.

Portfolio

I’m getting too many stocks in my portfolio. I am also seeing my cash position dwindle because I keep picking up new stocks without selling old ones. I am still extremely cautious about Europe, and being so, I am getting uncomfortable with both of these trends in my portfolio. In the next couple weeks I am going to reevaluate what I own and start paring where I need to. The problem, as it always is, is that I like the prospects of all the stocks I own. Unfortunately, as I think I showed rather clearly in my last post describing my 2011 performance, I am just as often wrong about that as I am right. The likelihood of my own fallibility must never be underestimated.

All the Devils are Here (though most have probably moved to Europe)

Over the winter break I read the book All the Devils are Here, by Bethany Mclean and Joe Nocera. The book essentially traces out all the strands that culminated in the panic of September 2008. The book identified the following factors:

A reliance on ideology instead of analysis. In particular this applies to the Federal Reserve and Alan Greenspan, whose ideological “market is always right” view permeated the decisions of the Fed and to some extent those of the other regulatory bodies. But more generally, ideology, specifically free market ideology, seemed to permeate through all the political and financial institutions to the point that it replaced a sober look at reality. Similarly, for many traders and investment bankers, an ideological reliance on “the model” often led to an ignorance of the potential risks of an outlier scenario

The absence of regulation. For a variety of reasons (the power of the lobby groups, the political infighting between the regulatory bodies, the ideological free market view of the participants and the myopic focus on regulators on Fannie and Freddie) an attempt to regulate the subprime industry was hardly even contemplated until it was too late.

The development of securitization. The most important consequence of the innovations to pool mortgages, to tranche pools, and then to create pools of pools (CDO’s) was that the lender and the borrower became further and further divorced by more degrees of separation. The securitization process created so many layers of intermediaries between the party who actually ended up with the loan on their books and the party that took the money that risks were easily lost in the translation.

The rubber stamped AAA status provided by the ratings agencies. Some books focus on how the rating agencies didn’t understand what they were rating. Mclean and Nocera point out that the revenue structure of the agencies was doomed to be corrupted. A system where the raters are paid by the producers of the securities they rate might be considered to be an insane one. The result was that the agencies were played off against one another by the investment banks; market share went to the most relaxed rating. Add to this the fact that the agencies, particularly Moody’s, became focused on profits at the expense of their inherent conflict of interest, and you had a situation ripe for abuse.

Greed. Politicians more concerned with their own campaign donations than with promoting sustainable public policy. Company executives intent strictly on their own promotion and profit. Mortgage originators with essentially no moral compass at all. The system was (and is) corrupt.

A lack of understanding. The same characters at play as with greed. So few people saw the disaster coming. Sure some did, there were a few regulators and a few hedge funds that saw how unsustainable the leverage being piled on in the mortgage sector was. But the vast majority didn’t have a clue. Even the supposed smart money didn’t really get smart until 2006-2007.

It is this last point, the lack of understanding, that I think is most relevant to what we face today. It really surprised me how little the people in influential and powerful positions understood the concepts that they were making decisions with regard to. Even Hank Paulson, who is actually portrayed in quite a positive light, was completely blind to the corruption and leverage being amassed in the mortgage market.

This naturally begs the question of Europe: how many of the politicians and bureaucrats in the EU really understand the situation they are trying to navigate? Do they really know the risks inherent in the decisions that they are making? Do they even really understand the banking sector they are trying to protect?

The last 6 months for me has been an education in how the modern banking system works. I have been trying to read all that I can, all the boring, technical aspects. And I don’t think for a minute think that I’ve wrapped my head around it. There are so many moving and interdependent parts. It’s also not a very tangible subject. It simply isn’t something that is easily understood.

Thus I think it’s a legitimate question as to whether the bureaucrats of Europe have the understanding required to navigate the minefield of sovereign defaults and banking bankruptcies. As Lehman showed, it only takes one mistake to create a loss of confidence that spirals uncontrollably.

How can you take on risk with this in mind?

The end of (tax loss) selling?

The week after tax-loss selling is always an interesting one. It provides the first glimpse into whether a security has been facing unrelenting selling because of investors simply wishing to take their losses (and their tax breaks) and move on, or whether something more nefarious is at play. Along the lines of the former, this week provided a rather marked jump in a number of the regional bank stocks that I have initiated a position in. Most conspicuous of these moves was that of Atlantic Coast Financial.

A Take-over Imminent for ACFC?

ACFC had a rather astounding 50%+ move this week. I really have no idea what precipitated the move. To take it with a grain of salt, the volume for the stock this week was less than spectacular, though the same could be said for almost the entire move down.

As I pointed out last week the stock is a bit of a flyer; the bank is a mortgage lender in one of the most crippled mortgage markets (Florida), they have bad loans coming out their wazoo, and a stock that has fallen from $10 to $1 in less than a year generally does not do so on speculative panic alone. Nevertheless, part of the story is the book value, which even with 3 years of bad loan write-downs lies at a rather surreal $19 per share (versus a share price of $1.70 when I bought it).

The other part of the story is simply the realization that what is going on with this bank (and many of these little community banks that got caught up in making bad loans at the wrong time) is a race between the write-downs of their past transgressions and the earnings of their current performing loan book. With ACFC it is not at all clear to me that the bad loans will win out; in fact I tried to make the case last week that with a little luck (and an improving economy) the performing book may very soon be able to out-earn the losses on a consistent basis. If this happens, the shares are clearly worth more than 10% of book value. Even if it just becomes a possibility, a shrewd competitor may be tempted to take a plunge. I constructed the chart below to try to see where ACFC is in that process. The chart compares earnings before provisions (black) to the quarter over quarter change in non-performing loans (red). Its basically a look at whether the company is out-earning the loans going bad each quarter. The 3rd quarter was the first in four that the black won out.

Community Bankers Trust: Another Regional Bank with a Move of its Own

While ACFC was the best of the lot of regionals, there were others that showed signs of life. Community Bankers Trust surged on Friday. The stock remains at about 1/3 of book value. If it were not for Europe and the ever-impending doom there, I would add more. As well, Oneida Financial continues to push higher. Unlike ACFC, BOCH and BTC, Oneida is a terribly boring bank trading at about book that is probably going to do nothing but increase in price by 10% a year and pay a 5% dividend until one day it gets bought out. At some point I might get bored with with relatively low return, but in this environment, I am happy to take a reward with so little risk.

Will Gold Stocks Rise now that Tax-loss Selling is over?

As for the golds, Esperanza, Canaco and Geologix all are showing classic signs of a let-up in tax loss selling. All are well above where I bought them. Aurizon, on the other hand, continues to be sold rather indiscriminately. Yes, I realize that the price of gold is getting clobbered on a regular basis. I can appreciate that investors may be questioning the wisdom of holding gold as a hedge to anything given the fact that it seems to dramatically underperform on risk-off days.

Still, I scratch my head at Aurizon. Here is a low cost gold producer that is comparatively less correlated to the price of gold than most of its competitors. For one, if you are low cost you are by definition high margin. Thus, a $30 move in the price of gold is of much less impact to a producer with $1000/oz margin (like Aurizon), than say a producer with a $500/oz margin. Yet Aurizon regularly trades down MORE than your average gold producer on the down days.

Going Short Argonaut Gold and long Aurizon Mines

So confounded have I been that in order to hedge my risk with Aurizon I have decided to take a short position in a fellow gold producer, Argonaut Gold. To be sure, there is nothing wrong with Argonaut Gold. I wrote the company up rather glowingly a couple months ago. However that was at $5, and now AR trades at $7, while in the same time Aurizon has fallen to less than $5. Below is a comparison of the key metrics of both companies.

So to briefly summarize the above, Aurizon produces more than twice as much gold, it produces over double the cash flow, and to top it off, Aurizon’s 3rd quarter was stronger than Argonaut’s. Argonaut potentially has a better pipeline of projects, but this is more than nullified by the fact that Aurizon trades at almost half the price on a per producing ounce basis, produces those ounces at $50-$100 cheaper, and has over $1 in cash on its balance sheet while Argonaut has a mere 30 cents. It simply doesn’t make sense.

While I remain bullish the price of gold, I also remain wary that I am not very right in this bullishness at the moment, and so it seems like the prudent thing to do to short what seems relatively over valued and buy what seems relatively undervalued. Anyways, that is what I did.

I also bought back OceanaGold for another run. Its getting to be repetitive, but it has been a consistant source of profits. Buy OceanaGold below $2.20 and sell it above $2.70. I must have done this 3 times already in the last 9 months.

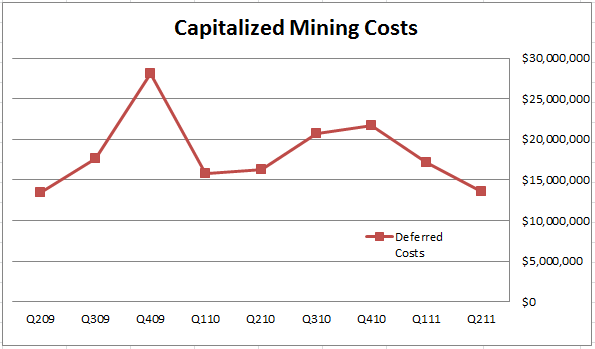

Last month I wrote a post about the second quarter results from OceanaGold . In that post I looked at the company’s assertion that the quarter was not as bad as it appeared on the surface because the total mining costs had not changed significantly. What had changed was that more of the costs were being expensed and less of the costs were being capitalized. Below was a chart I provided showing how OceanaGold’s capitalized mining costs had varied over the course of the last couple of years.

To generalize the point of that post, looking strictly at expensed costs (cash costs) as a judge of a company’s quarterly performance has its flaws.

So just to refresh, the difference between expensed and capital costs is as follows. Expensed costs show up on the income statement and factor into the commonly evaluated cash cost number for a company. Under most accounting methodologies these are the costs that can be directly attributed to the ore being mined. Capitalized costs, on the other hand, are hidden on the cash flow statement under the Financial Activities, usually showing up as Property, Plant and Equipment. They can be one time charges such as a new pinion bearing housing on the ball mill, or they can be pre-mining expenses such as the stripping away of overburden to get to ore that will be mined later.

While the expensed costs get all the headlines, the capitalized costs don’t get much attention at all. Yet both types of costs are equal in the place where it really counts: how the company’s cash balance changes from quarter to quarter.

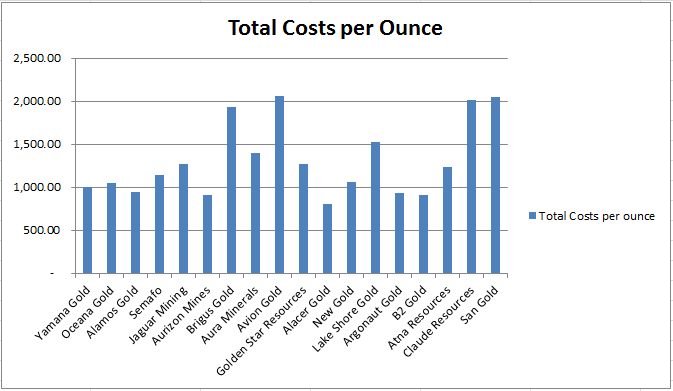

The work I did for OceanaGold led me to wonder what the same sort of analysis would look like for other gold companies. What are the total costs of mining on a quarterly basis and how do they differ from the reported (expensed) cash costs that get so much attention from the brokerage community? What we are really interested in with any company is how much free cash they can generate. If a company is generating a lot of operating cash but is plowing that cash right back into the mine as sustaining capital, well then they are running on the spot. So total costs is what matters, be they lumpier and messier than cash costs or not.

Moreover I have to imagine that there is grey area when applying the criteria of what constitutes an expensed cost and what constitutes a capitalized cost. The implementation whatever accounting methodology is used probably varies from company to company. Simply looking at cash costs might ignore these discrepancies and paint a poor picture of what’s really going on in the operations.

To look at the effect of overall costs, what I have done is simply this. I took the cash costs stated by each company for the last two quarters and added to those costs the additions to property, plant and equipment as reported on their cashflow statement. Then I divided summation of these two costs by the ounces produced over the first two quarters. Because PP&A is likely to be more variable, it might be worthwhile to do this over a longer time horizon, but for now this will have to suffice.

This is an interesting result. It is particularly interesting when you compare the list against the same list of companies sorted on the more traditional cast costs metric.

What you see is that the companies that are lowest on the cash cost scale are not necessarily the lowest on the total costs scale.

Now of course, like everything, these results have to be taken with a grain of salt. One of the reasons that capitalized costs are not added to cash costs in for traditional analysis is because they are inherently lumpy. One time purchases that should be capitalized could skew the picture of the quarterly performance of a company. Brigus Gold is a good example of this. They are ramping up their underground mine at Black Fox right now. There are a lot of capitalized costs associated with that ramp up.

I went another step further by looking at costs for the full year 2010. That graph is shown below. Here a few of the companies (Lake Shore, Atna, Alacer, etc) drop off the list because they didn’t have comparable production for the period for one reason or another.

To make a few observations from the above graphs, the first being that OceanaGold does not look like such a high cost producer. While their cash costs are higher than the norm, their capitalized costs have consistently been lower than normal. I wonder how much this is caused by having a mature mine.

Another observation I would make is that Aurizon Mines truly is a (if not the) low cost producer. Both OceanaGold and Aurizon Mine are cash generators, which should serve them well over the longer term as they develop their mines.

A final observation is that B2Gold is worth taking a closer look at.

Why so cheap?

Why so cheap?

{kind=link}