Week 22: Still Partial to Cash

(see end of post for current portfolio composition)

When you are 57% cash, its difficult to outperform the market to the upside.

That is exactly what happened this week. The TSX was up 5%, the S&P up 6%, the Venture up 3.3%, and my portfolio was up a lowly 2.9%. Having as much cash as I do certainly has protected me against the downward trend over the last 4 months, but it will also prevent my portfolio from having outsized gains if we have a significant rally.

I Remain Wary of Europe

I am, however, in no mood to change my tact. Though I admit that the developments this week were constructive, and they could very well lead to a continuation of the market rally. In the short term, the dollar liquidity provided by the central banks will allow the European banks to fund themselves for a while longer. Probably more important, Mario Draghi’s statement below, clipped from this WSJ blog post, sets the stage for rate cuts and at least raises the possibility of a QE of sorts out of Europe

Yesterday, Mr. Draghi made a statement that we find tectonic-plating-shifting-like in nature when he said firstly that the “Downside risks to the economic outlook have increased.” They have indeed, and we’ve no problem with what he said for that is indeed the truth. Then, however, the plates shifted when he said, noting that the ECB’s mandate, that price stability is to be maintained “in both directions.” In other words, the ECB’s mandate forces the authorities to be concerned about deflationary risks as well as those inflationary. Did you hear the plates shifting? You should have for they have indeed shifted. Draghi’s warning was that the authorities are just as concerned about deflation as inflation and that monetary expansion is to be considered just as has monetary contraction.

Yet if anything I am less inclined to add to investments. I am more convinced that the outcome is Europe is close at hand, and the while a positive resolution (assuming there is such a thing) would lead to a continuation in the move to the upside, the risk still remains that the resolution won’t be positive. I am sure in such a case everything (save the USD and treasuries) will go down.

Bass Talks Again at AmeriCatalyst Conference

Case and point is Kyle Bass, who in my opinion has the clearest explanation of the problems in Europe. He was again at the AmeriCatalyst conference this year, and a few days ago the segment was postedto youtube.

One of the interesting points that Bass makes is that while Greece bonds are trading at astronomical interest rates, the actual rate of interest the Greeks pay is a little more than 4%. At thta interest rate, interest payments in Greece are 16% of government revenues. This was basically the tipping point of no return for the country.

It reminded me of something I wrote in my analysis of Italy a few weeks ago:

According to Italy’s Ministry of Economy and Finance, Italy’s outstanding debt is around E1.85B or USD$2.5t (2010 figure but Italy is close to a balanced budget so its probably nearly the same this year). Government revenues in 2010 were E729B or USD$950B. To do a little simple math then, every increase in the Italian rate of borrowing of 1% results in an eventual increase in borrowing costs for Italy of about $25B, or about 2.5% of government revenues.

In 2010 Italy paid E80B in interest expenditures. So right now the average interest rate that Italy is paying is about 4.3%. A 1% rise therefore raises the average interest rate to 5.3%…Once the market starts to determine that you are on a road to insolvency, its pretty easy to get pushed on the fast track. In the case of Italy, 6% is starting to get closer to 7% every day. If yields rose 3-4%, then Italy would begin to have a problem with the interest that had to pay on their debt.

The problem that I alluded to above is that when you have as much debt as Italy has (or for that matter Greece or Portugal or Japan or even the United States has), your ability to pay that debt is as much determined by the market’s perception of how able you are to pay your debt as it is of anything.

I also noted that “if yields rose 3-4%, then Italy would begin to have a problem with the interest that they had to pay on their debt”. Well here we are. Right now Italy has interest payment that are a little under 11% of government revenues. At 8% interest rates, Italy would eventually soar past Greece’s paltry 16% of revenues on a path that would eventually lead them above 20% of revenues. Hmmm….

Is the Gold There?

Another very interesting clip from the interview occurs at the 42 minute mark. If you don’t listen to any other part of the interview, I would beg you to listen to this. Bass gets asked why he decided to take delivery of the gold futures he held on the Comex. He explains how he looked into the situation at the Comex. Turns out they had $80B of open interest and $2.7B of deliverables. This seemed to him to be slightly underfunded. He went to the head of delivery’s at the Comex and asks what they would do if suddenly everybody (or at least 4% of contract holders) wanted to take delivery. The response he gets is A. “Oh Kyle that never happens, we rarely get 1% of contracts taking delivery”, and B. price would fix the problem.

In other words: there is no plan for what to do if everyone wants to take delivery.

This is one of those situations that isn’t a problem until it is a problem and so far it isn’t a problem. But when it becomes a problem, and when Comex or whatever clearinghouse that has teh problem has to pony up more gold then it has, well that is the definition of a squeeze. But maybe this never happens. If it does happen, price is going to do something, and that is go straight up.

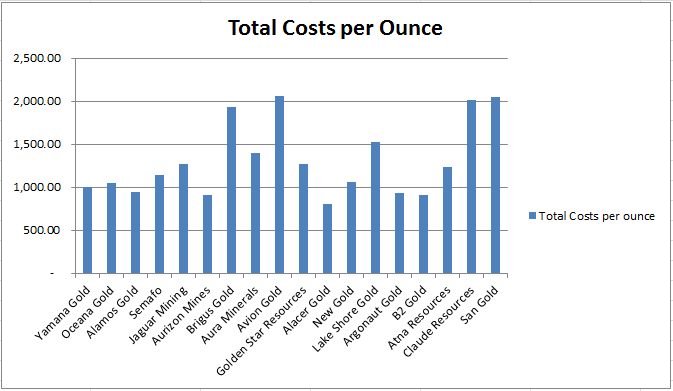

The Best Bargain Among the Gold Stocks

I have been working through an analysis of Atna and while I am not quite ready to post that analysis, I am ready to say that I believe Atna is the best way of playing a bet on sustainable gold prices at $1500/oz or higher. As I have dug deeper into the company I have been surprised with just how many assets they have. In addition to a producing mine (Briggs) and a low capital cost, high grade development (Pinson), they have over 1Moz of gold in Montana (Columbia), 300Koz of oxidized resource and based on recent drill results more to come at Reward, and another 150Koz of oxidized resource a few miles away from Briggs at Cecil. And those are just the properties with a known resource. In addition they have a score of properties with exploration potential, including a few that are signed off as JV’s to be drilled using other people’s money.

In the analysis I will post later I will get deeper in the net asset value of the company, but for now consider the following table. With Atna, for a price of about $100M enterprise value, you are getting around 5Moz of total resource, of which the majority is either very high grade (Pinson) or has open pit heap leaching potential (Briggs, Reward, Cecil). All to be had for $20/oz.

I plan to increase my position in Atna even further. I could forsee a time when it is primary vehicle for investing in gold.

Portfolio Changes

As I posted earlier this week, I’ve reduced down my position in Arcan Resouces substantially. I now basically have equivalent positions in 3 domestic oil producing juniors, Arcan, Reliable Energy, and Equal Energy. Consider this to be my oil junior basket. I own much more of Coastal Energy. I have no plans to reduce my position there. Coastal remains the single best oil investment out there in my opinion. They are self-funding, are increasing their reserves with every well, and trade reasonably at $98,000 per flowing boe, and far below their NAV (the NPV10 as per the 2011 reserve report was $10.42 per share, since that time they have increased proved and probable reserves from 25mmbbl to over 90mmbbl.

Portfolio

{kind=link}