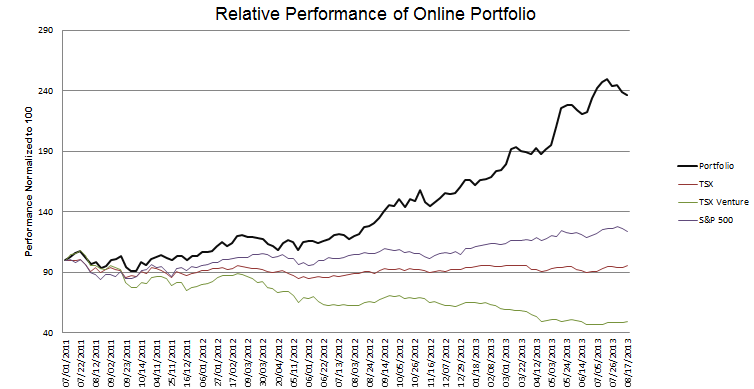

The Thesis has changed but I remain Long Axia NetMedia

Last weekend I wrote a nice little piece summarizing the investment thesis for Axia NetMedia (AXX.to). Would have made a great post, was concise, clear, short. Perfect… except that the company came out and sold the asset that I had centered the entire post on.

So the post lost some of its relevance. Still, it presents a good starting point with which to discuss the post-OpenNet version of Axia, so I have included the main body of it below, followed by a discussion of what’s next for Axia.

A big thanks to @17thStCap for this idea. I actually knew of Axia from years ago, my hometown is a recipient of the Alberta Supernet, but I hadn’t looked closely at the company until @17thStCap mentioned it.

Axia trades at an enterprise value of $95 million (Note: actually $70 million post-OpenNet transaction), and yet I think that the assets it owns that provide fibre broadband transport services in France Alberta and Singapore, are worth quite a bit more than that.

Let’s focus on Singapore for the moment, as I believe it is the immediate catalyst. The company owns 30% of a partnership called OpenNet (look here for an overview of OpenNet), which provides fibre to 1.1 million residential and 26,000 commercial premises as of the end of the June quarter. OpenNet grew its top line and EBITDA by just slightly less than 100% in the last year. In the month of June alone, fibre broadband subscribers increased 31,000 to 380,000. Read more