Week 111 Portfolio Update: When Things Aren’t Working…

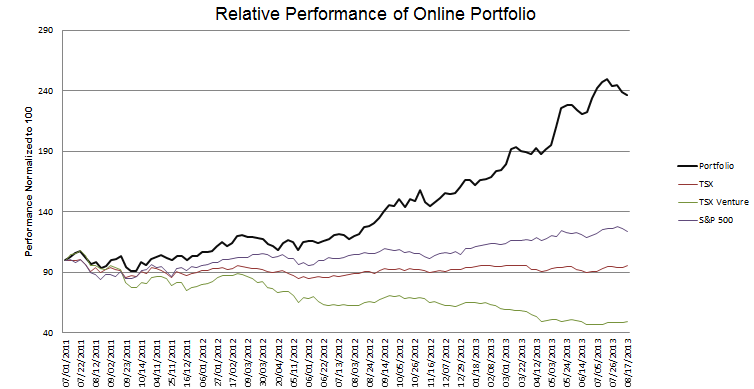

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Shake-up

In a previous post about Walker & Dunlop I described the consequence of being on vacation while the company announced poor results, which was that I was not able to take advantage of a clear selling situation. The same was the case for Dex Media.

In the past I used the term “good enough investing” to describe what I’m trying to do with my portfolio. I work a full time job, have a life and need a break now and then, and all that means I just can’t be on top of everything. I try my best but I have found it necessary to employ techniques to mitigate this. In particular, I sell stocks when things aren’t working out.

While I’ve had my share of winners over the past month and a half (AIQ, NVS, NCT, NRF, IQNT to name a few), I’ve also had my share of losers (NKO, EXE, VTNC, and the above mentioned duo) with the result being that my portfolio has done not much of anything. While I remain hopeful that both Niko Resources and Extendicare eventually pan out, the fact is that thus far they haven’t.

So the list of what is not working has grown. While its not like I have taken a huge drawdown (about 5% from the top), the mental capital that I am consuming has been significant and I am feeling less confident as the market goes up without me but comes back down with me.

What I typically do at times like this is sell until my perspective improves. Usually once I have reduced the number of names and capital at risk, a greater of level of clarity follows.

I tweeted the following earlier this week:

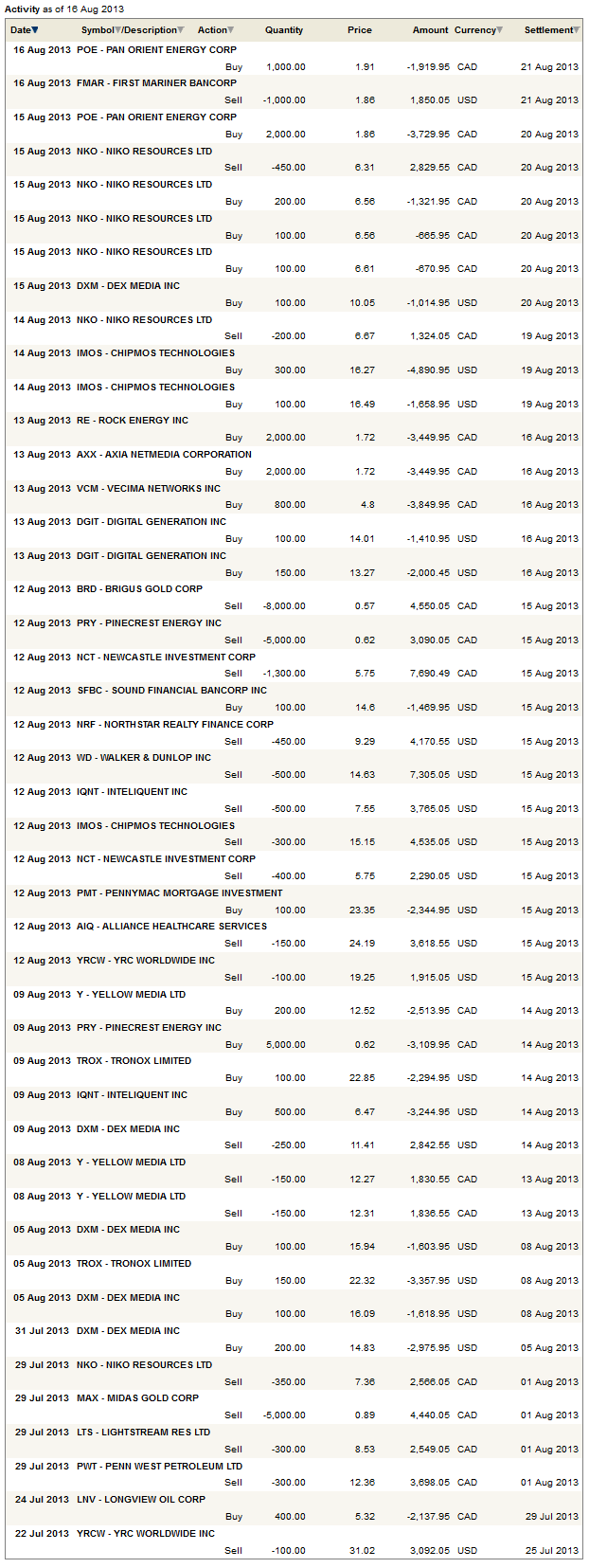

These were stocks I had sold in my real portfolio the prior week, and had tweeted as such, but as sometimes happens, I didn’t make the trade in the practice portfolio. Other sales in the last month were Northstar Realty (thankfully before the share offering), what was left of YRC Worldwide (thankfully before the second quarter results), a significant reduction in my position in Dex Media (brought upon simply by the fact that I have been horribly wrong) and the sale of First Mariner Bancorp, which has been a great little stock for me (more than tripled since I bought) but has had trouble posting profits as mortgage refinancings dry up and still has unresolved issues with TrUPs securities that will come due at year end.

So lots of sales. The clarity I bought was this:

Out and in of ChipMos

I quickly realized it was a mistake to sell ChipMos. The stock is trading at less than 3x EBITDA, without significant net debt, and there are potential catalysts in the way of new business from Micron, via their merger with Ephidia, potentially Apple (though its just a rumor) and a listing on the major Taiwanese exchange. I bought it back the next day, but lost about $0.75 before I did. Such is the cost of insight.

One thing that is working: Canadian Oil

One thing that’s working are my oil and gas stocks (Niko excluded). Last month I began to I suspect that the Canadian junior oil and gas stocks might be in for a turn and that has proven to be correct. While always uncertain, usually these moves last a number of months so I think we are still in early innings.

Extending this idea, I added a new position in Rock Energy (RE.to) a little over a week ago. Rock is a really cheap heavy oil producer in Saskatchewan. At the price I was buying ($1.60-$1.65) the stock was less than 2.5x EBITDA, and at the current price its only slightly more. They have minimal debt and what looks to be a solid development project in Mantario.

I also added a position in Longview Oil and Gas, which I already discussed in some length as an aside in my post about Novus, and Pan Orient, which while not typically thought of as a Canadian oil stock, as most of their exploration is done overseas, nevertheless has an oil sand deposit with SAGD potential called Sawn Lake that I think could prove interesting over the next few months. I got the idea for Pan Orient from a subscription service, but that was a couple weeks ago so hopefully there is no ill-will from discussing the idea here. The research discussed herein is all my own. Its also being discussed on message boards so its no secret.

Pan Orient’s neighbour and (I believe) joint venture partner at Sawn Lake, Deep Well Oil and Gas, entered into a pretty impressive private placement with Maurel et Prom. The placement was done at 48 cents while the stock had been sitting at under 10 cents (though the agreement stipulated other conditions that allow Maurel et Prom to buy in further in the future) . Deep Well Oil and Gas has a very informative website that discusses Sawn Lake, and this post summarizes the land package of Pan Orient and Deep Well in sufficient detail:

For those not familiar with the details. Andora’s(POE) main lands are immediately to the south of the Deep Well lands referred to in the news release. Furthermore, Andora owns a 10% interest plus 3% royalty on 24.5 sections of the Deep Well lands, plus 100% interest on 9 sections immediately to the north of it. Not sure on what portion of Deep Well’s land their demonstration project will be undertaken, but obviously it is very close to POE’s and the timetable is almost identical for the two projects.

I think that this bodes well for Pan Orient. Given Pan Orient’s market capitalization of $100 million, no debt, $88 million of cash after working capital adjustments, and assets elsewhere, it seems like some success at Sawn Lake could prove to be quite a boost to the stock. According to the press release drilling is commencing at Sawn Lake and first production is expected in the first months of 2014. If Sawn Lake works (and its a big if), Pan Orient has pointed to a pre-tax NPV10 of between $300-$500 million, so multiples of the current enterprise value (which by the ways is nearly zero after netting out the cash). Of course the cash is going to disappear on projects like Sawn Lake (and more Indonesian drilling, as Pan Orient has the same dry hole affliction as does Niko). Its not the sort of position I would bet the house on, but taking a small 2% speculation on it seems reasonable.

I sold out of Penn West and Lightstream as I suggested I would, to move on to Rock, Longview and Pan Orient.

Higher rates are not a good thing for dividend stocks

While the glacial speed with which the thought came may lead one to question my capacity, it did finally don on me that higher rates are going to cap commercial mortgage plays like Walker & Dunlop and put pressure on REITs. This rather obvious realization came to me a bit late in the case of Walker & Dunlop, but it did help me get out of Newcastle Investments, Northstar Realty, and to a lessor extent MGIC before each fell significantly at the end of this week.

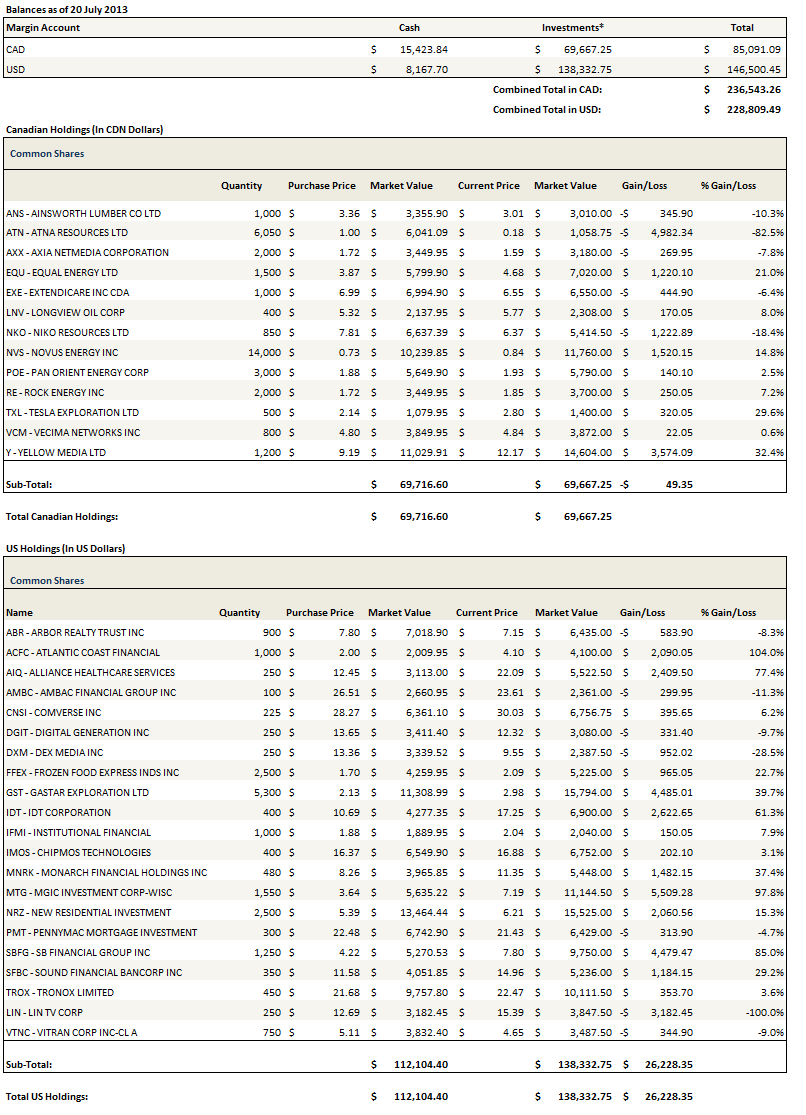

Frustratingly, I grouped New Residential in a different bucket because its mortgage servicing rights should actually benefit from higher rates, yet the market continues to regard New Residential as a run-of-the-mill REIT, so I’ve taken a hit on that one. It is the largest position in my portfolio so the hits hurt.

New Positions in Cheap Stocks

I used the capital from the sales to invest in a number of new non-oil opportunities. These are Digital Generation (DGIT), Axia NetMedia (AXX.to) and Vecima Networks (VCM.to).

I have a post that I’m nearly ready to publish on Axia NetMedia, which a company I really like, and while I took a small position in Vecima I am still getting comfortable with the name so I’m not ready to say too much there.

Digital Generation

With Digital Generation, last week the company announced the sale of their TV ad business for a price tag that eliminates the all of the company debt and will provide a special dividend to shareholders of $3 per share. Dedwardssays had a good blog piece on the company that explains the situation well, and an excellent spreadsheet that explores the various scenarios.

When I did some quick work the morning after the transaction was announced, I found that the remaining digital business was probably worth more than what the stock opened for. Below are my estimates of Digital segment EBITDA for the first and second quarter. The company breaks down their revenue and operating costs on a per segment basis, but I had to estimate that sales and marketing, research and development, and G&A costs would be the same fractional percentage as digital revenue to total revenue.

***NOTE: It has since been pointed out in the comments that in the 10-Q Digital Generation provides detailed segment information and breaks down EBITDA by segment and that using this information the segment EBITDA of Digital is around $40mm annualized. In light of this I will have to give this some more thought and re-evaluate***

When I was writing this up and comparing results, I was pleased to see that my own numbers aligned with the spreadsheet Dedwardssays provided.

When I was writing this up and comparing results, I was pleased to see that my own numbers aligned with the spreadsheet Dedwardssays provided.

Digital Generation grew on-line revenue by 19% year over year in the second quarter, and by 14% in the first half of the year. Extrapolating an annual EBITDA of $50 million, I think that the current enterprise value of the business post-sale of about $200 million is simply too low. Thus I took a position on the name.

If the Drawdowns Continue…

My portfolio is down about 5% from its highs in mid-July. The toughest thing to do after a quick drawdown like this is to admit that things are wrong and take money off the table. You just want to get back up to the highs and then call it a day. Of course this is a fantasy, if my portfolio rallied back 5% my outlook would be entirely different, and I would probably be looking for ways of adding risk rather than mitigating it.

It is so important, and so hard, to let go of what was, deal with what is, and accept things for what they are. For me this is a more valuable skill than all the analytical tools combined. You have to know when to walk away.

I’m not ready to walk away quite yet, but I’m getting close. If I continue to see deterioration of my portfolio you are going to see a pretty big shake-up at some point. Thus far, the shaking has been mostly reallocation, with the cash position being steady. But if I say lose another 5% next week, that cash position is going to go up significantly. As tough as it is to sell away from the highs, it is what I have learned works for me.

High on the list of targets would be Arbor Realty, Ambac Financial, Vitran, and MGIC. On the other hand I am looking at a number of technology companies, including DSP Group, Immersion Corp, Radcom and Radware. If anyone has thoughts on any of these names please drop me a note.

And then there’s Niko…

I typically have at least one stock in my portfolio causing me outsized consternation. Right now that stock is Niko. If you have been reading my twitter feed, you’d think Niko was a 20% position and not a 2% position. Admittedly is was originally 5% reduced to 4% on price declines and then 2% on capitulation. But the mental capital it has exhumed is an order of magnitude of that.

My trading of this stock has been embarrassing. I have sold then bought back then sold then bought back portions of my position at least 4 times in the last two weeks. And this isn’t trading. Its indecision. On the one hand I am enticed by the potential of the new MJ-1 discovery. The company said in its latest press release that the reservoir has an aerial extent of 65 square kilometers. BP recently put a 3TCF estimate on the deposit. Everything is pointing to a very large find. And the deposit is directly below the existing D6 production so much of the development is already there.

But the company needs development cash, and the sources of this cash remain to be announced. Asset sales announced in March are still yet to close. Bank lines expected August 1st are now delayed to September, and there is some talk on the call that seemed to suggest that the bank lines may not be increased at all, and even reduced. There are apparently ongoing discussions with Indian banks but again, we wait and wait. The company says it has a lot of balls in the air. I think you could easily take that phrase ironically.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

For DGIT, can you explain how you got EBITDA for Q1 and Q2 and the $50M extrapolation? From latest 10Q, I got $9.8M EBITDA (Q2) and assuming 50% overhead expense (~$12M) the annualized EBITDA would be ~$28M.

To be more conservative using FCF, my guess is Online capex is at least $10M and company still has cash taxes. So FCF less than $18M. Still interesting but not as attractive as you put it.

I used the numbers I provided in the table and the method I described in the post. I mean its pretty easy to reproduce what I did by taking the income statement in the 10-Q and isolating digital the way I did. Let me know if there is something wrong with this but I think I was pretty clear with what I did.

Oooooh. I see. I didn’t realize the company provided segment by segment EBITDA in the 10-Q so I was trying to extrapolate it from the income statement. You are right. I might be over-estimating EBITDA. I am surprised though that the television segment is only accounting for $8mm of non-corporate G&A, S&M and R&D costs. That seems very low. Nevertheless, thanks for the heads-up.

This is Anonymous from original comment.

Yea not trying to poke holes but just sharing my thoughts since I’m familiar with DGIT. The EBITDA margin of Online segment has been much lower vs. TV; although that appears to be improving quickly with positive leverage. I’m fortunate to have accumulated a significant (20%+) position in DGIT at much lower cost basis. I’ve thought hard about whether to take some profits and decided to stay put. My rationale:

– 10x EV/EBITDA, 10x FCF (forward basis) seems reasonable for growing online advertising company

– MediaMind was publicly traded and using prior market cap implies upside over $15; probably higher given subsequent growth and addition of other acquisitions

– $3 dividend will provide some return of capital anyways

– Upside depending on how the buyer financing goes and liquidation of TV working capital

But the risks:

– small chance the sale does not complete due to financing or regulator

– deal closes in Q1 2014, still a long time off; stock probably range bound for a while

– Clinton Group is selling => Is there something I’m missing?

I’m still not quite comfortable and stock is tanking as I’m writing this… Honestly I’m quite surprised. I thought stock would go over $15 after the sale.

Btw, I’m a recent reader and really enjoyed your blog. Different style, which helps me to view things from another perspective.