The Thesis has changed but I remain Long Axia NetMedia

Last weekend I wrote a nice little piece summarizing the investment thesis for Axia NetMedia (AXX.to). Would have made a great post, was concise, clear, short. Perfect… except that the company came out and sold the asset that I had centered the entire post on.

So the post lost some of its relevance. Still, it presents a good starting point with which to discuss the post-OpenNet version of Axia, so I have included the main body of it below, followed by a discussion of what’s next for Axia.

A big thanks to @17thStCap for this idea. I actually knew of Axia from years ago, my hometown is a recipient of the Alberta Supernet, but I hadn’t looked closely at the company until @17thStCap mentioned it.

Axia trades at an enterprise value of $95 million (Note: actually $70 million post-OpenNet transaction), and yet I think that the assets it owns that provide fibre broadband transport services in France Alberta and Singapore, are worth quite a bit more than that.

Let’s focus on Singapore for the moment, as I believe it is the immediate catalyst. The company owns 30% of a partnership called OpenNet (look here for an overview of OpenNet), which provides fibre to 1.1 million residential and 26,000 commercial premises as of the end of the June quarter. OpenNet grew its top line and EBITDA by just slightly less than 100% in the last year. In the month of June alone, fibre broadband subscribers increased 31,000 to 380,000.

Looking at the second quarter, Axia’s share of EBITDA from OpenNet would have been between $6-$7mm on an annualized basis. Let that sink in for a minute. Consider the growth that OpenNet is experiencing, consider that the Fibre business is mostly a fixed cost business where once a critical mass of customers is achieved, additional customer receipts flow fairly uninterrupted to the bottom line, and consider that OpenNet is not competing with ISP’s, they are providing wholesale transport services that will be used by all Singapore ISP’s that want to offer a fibre solution (currently Nucleus Connect, SingTel, M1, StarHub, ViewQwest BlueTel Networks, NTT Communications World Network, and Tata Communications).Given the growth that OpenNet is experiencing, what kind of multiple would be appropriate?

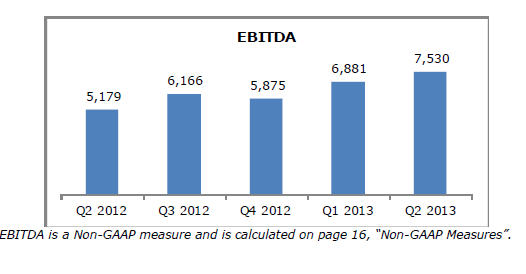

The other units in Alberta and France are together showing growth and delivered EBITDA of $7.5mm in the second quarter. I’ll talk about these units in a later post, but for now consider the historical EBITDA stream shown below and whether an enterprise value of $95mm is justified by these two units alone:

As I mentioned I believe that OpenNet provides a fairly immediate catalyst for the company. On the second quarter conference call I had the distinct impression from CEO Art Price that they are pursuing a sale of their OpenNet ownership. He said they were considering their options and then later, when asked about the potential of the company pursuing a dividend model, said that there were a number of things in the works that were not settled and that would lead to a clearer picture of the potential model going forward once they were settled.

As I mentioned I believe that OpenNet provides a fairly immediate catalyst for the company. On the second quarter conference call I had the distinct impression from CEO Art Price that they are pursuing a sale of their OpenNet ownership. He said they were considering their options and then later, when asked about the potential of the company pursuing a dividend model, said that there were a number of things in the works that were not settled and that would lead to a clearer picture of the potential model going forward once they were settled.

If Axia sells their stake in OpenNet, I think it’s going to be for a surprisingly high number. A 10x EBITDA multiple OpenNet would fetch a majority of the enterprise value of Axia. With the kind of growth that OpenNet is demonstrating, I don’t think that is an unreasonable multiple. It may even be too low.

Well it was event driven. Since last weekend Axia indeed sold OpenNet. So I got that much right. But the price they got was far less than I had hoped for. The company sold its stake for $31 million, which suggests a valuation in the 4x to 5x EBITDA range.

I talked to IR about this. Part of the reason for the lower than expected price tag was that OpenNet was not the sort of company you could sell on the open market with a bidding process. There was one logical buyer and that buyer was SingTel.

The other consideration was political. When the OpenNet partners signed up for the business, there was the expectation that it would be neutral to the end user, providing fiber to all customers without preference. Unfortunately what had begun to evolve was somewhat different as Singtel, which owns the ducts that run the fiber that OpenNet uses, took steps that made it difficult for OpenNet to operate in an independent way, in particular by refusing to honor their agreement to transfer the management of the duct system to an independent entity. The partners appealed to the Singapore government, but the appeal fell on deaf ears, at which time they decided to look for an exit, and that was achieved this week.

Nevertheless the stock price Axia went up on the news – even though I was off by a factor of two on my valuation. Its not a bad thing to have that kind of margin of safety.

What’s Left

While the real home-run type potential may have diminished with the sale of OpenNet, Axia nevertheless presents a good investment opportunity.

On current metrics, Axia has actually become cheaper post-OpenNet. In the last quarter France and Alberta combined to generate $7.5 million in EBITDA last quarter. The enterprise value of the company, after subtracting cash of $31 million that it will get from Singapore and $7 million it will get from Spain, is about $70 million.

On the growth side, I think its reasonable to expect EBITDA to increase in the coming quarters, albeit perhaps not to the degree it would have if they still owned the assets in Singapore.

Alberta Supernet

Alberta EBITDA is likely to be steady to slightly up in the near term. The company derives 75% of revenue from the Alberta government, which is a stable revenue source, and the historical trend has proven to be fairly flat after accounting for the end of a $5 million contract with Bell in 2011.

There is opportunity in Alberta . There are plenty of small businesses outside of the major centers that operate in flourishing small towns driven by oil and gas development that could benefit from fiber. And there are still many of the smaller towns where fiber is delivered to only one or two government centers, but there is yet to be an ISP signed up to offer a last mile consumer product. I thought that this Q&A provided decent background on the opportunity and explanations describing the relationship between Axia, the Provincial Government, service providers and customers.

There is opportunity in Alberta . There are plenty of small businesses outside of the major centers that operate in flourishing small towns driven by oil and gas development that could benefit from fiber. And there are still many of the smaller towns where fiber is delivered to only one or two government centers, but there is yet to be an ISP signed up to offer a last mile consumer product. I thought that this Q&A provided decent background on the opportunity and explanations describing the relationship between Axia, the Provincial Government, service providers and customers.

Longer term growth possibilities are going to depend on the renewal of the Alberta Government contract 2015, and I doubt that Axia will pursue any capital intensive opportunities in Alberta until some clarity is achieved on this contract. Axia leases the fiber in Alberta from the Alberta government, and as part of that leasing agreement they have the right to provide services to the Alberta Government buildings. As I mentioned before, government revenues account for a significant portion of Axia’s Alberta revenues. I’ll discuss the contract in a bit more detail a little later on.

France (Covage)

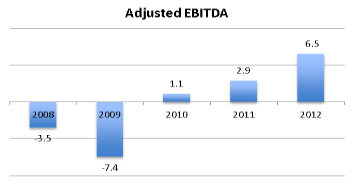

The growth opportunity in France is more compelling than Alberta. Adjusted EBITDA at Covage (name of the France business) has been consistently on the rise since operations started there. In the first 6 months of 2013, EBITDA at Covage rose to a little over $8 million.

According to the second quarter MD&A, Covage had customer penetration of 10.5% in the second quarter. It sounds like penetration should eventually settle at least in the 15%-20% range, with there being an outside chance that it reaches as high as 30% if there is significant adoption. Additional growth will come from extending their network to other communities. Below is an excerpt from the second quarter MD&A that outlines the landscape in France in Covage’s participation in it:

According to the second quarter MD&A, Covage had customer penetration of 10.5% in the second quarter. It sounds like penetration should eventually settle at least in the 15%-20% range, with there being an outside chance that it reaches as high as 30% if there is significant adoption. Additional growth will come from extending their network to other communities. Below is an excerpt from the second quarter MD&A that outlines the landscape in France in Covage’s participation in it:

The goal of this initiative is to have FTTH broadly deployed throughout France within 10 years. The government has segmented the counties in dense areas which are expected to receive investment from private operators, and semi-dense and rural areas which are eligible to federal and local government funding. In order to provide subsidies to those communities that would not naturally benefit from private sector investment, the government will make available €3.0 billion of grants and up to €20.0 billion of loans with maturities of 20 – 40 years. A Government Agency will manage the deployment of federal government funds, the extinction of the legacy copper network and monitor private operators’ deployments. The FTTH framework is prompting a number of FTTH bids to come to market. Covage is well positioned to participate in this growth opportunity and the company is active in a number of pilot projects as previously announced. In addition, Covage has responded to several RFPs that are entirely , or include an element of, FTTH.

Risks

One risk is that Axia is illiquid. For anyone taking a position of more than a few thousand shares, it will take time to get out and if something does go wrong, you won’t be getting out at anywhere near the current price. I took my usual ~4% position, but I will be wary of increasing it too much further unless there is some really good news or some real hidden value that I’ve missed, because I hate being stuck in a stock with no volume.

The other risk is that the Alberta SuperNet government contract, which expires in June 2015, is not extended. An extension with Axia appears to be the path of least resistance and therefore the most likely resolution, but you never know. The barrier to entry against competition is going to be a tricky RFP process. The contract falls under the governance of the Ministry of Service Alberta, but according to my discussion with IR, any RFP put forth by the ministry would only be able to guarantee government contracts directly from them, as other wings, say the Ministry of Education or of Health and Wellness, have their own discretion in how they use budgeted funds for communication. So as a prospective bidder you have to be willing to accept a contract requiring upwards of $15 million of maintenance capital on a yearly basis, but with only guaranteed revenue of around $10 million.

The other element in Axia’s favor is simply that they have done a good job under the current contract. The Supernet was a challenging undertaking, and the company has managed to build and operate it with, from what I have been able to glean, has been relatively few problems.

Nevertheless, it remains a risk. Contracts, especially government contracts, are never sure things. Worth noting is that if there is an RFP it will be public domain (all RFP’s in the province are) and interesting to read. I will be keeping an open eye for it once we move into 2014.

Conclusion

With OpenNet gone Axia probably isn’t going to be a flashy 10-bagger type of investment that I had hoped for a month ago when I got into the stock. Nevertheless, the value proposition at the current price is clear. The catalysts in the near term will be the release of third quarter results, which will hopefully show continued customer and EBITDA growth from Covage, and perhaps a dividend of some form (to distribute some of the cash they have received from Singapore and Spain). Clarification on the Alberta contract may be a bit further off, but if a positive outcome does result, a re-rating of that EBITDA to a much higher multiple would seem appropriate. Until then I will be content to hold on to my shares and see how things unfold.

Thank you for the idea. In 2012, Openet had 29MM (or Axia share 8.7MM) EBITDA. Singtel fees started in 2Q, and I am unsure why there is a charge going forward. From the Q2 MD&A.

“For Q2 the fee was SGD$10.5 million. Going forward, the fee will be the greater of SGD$13.9 million per quarter or 75% of OpenNet’s eligible revenue minus certain deductibles.”

I guess the asset is gone for a (steal) low price but so be it. The other assets make Axia still cheap in my opinion.

EBITDA should improve from revenue/customer growth as well as startup expenses that will end in Massachusetts later this year. The Spain network (a drag in historical financials) was sold. The Q2 MD&A puts the Spain assets in the discontinued operations category.

Axia Announces Agreement to sell its interest in OpenNet. Axia Asia will sell its 29,744,999 ordinary shares of OpenNet representing approximately 30% of the issued and paid-up share capital of OpenNet, to the Purchaser, for aggregate cash consideration of approximately S$38 million

What are some comps people are comparing Axia to?

clint

disc: long

I’m afraid I can’t be of a lot of help on this one. I spent some time researching if there were other provinces in Canada set up with a similar fiber structure but there doesn’t appear to be. There may be companies in the US or worldwide but when I did some googling and article searches I didn’t come across any public name (though admittedly i didn’t spend a lot of time on it). Sorry about that.

no worries

I’m not very familiar with IFRS standards, can anyone tell what their basis in OpenNet is? I can’t tell if it’s $10m, $25m, or $35m (note 9 of the last financials) to figure out potential tax ramifications. thx