Last week was another good week for my portfolio. I tend to perform well in sideways markets. In down markets, especially those like we’ve had recently where the correlation of all asset classes go to one, I tend to underperform on an individual equity basis, because the stocks I own are for the most part small caps and commodity stocks, and they get hit harder than the broader market. I’m trying to mitigate that with my currently high cash position, and it has done its job and dampened the effect.

I would, however, like to reduce my cash position at some point, as it is har d to make money when so much of it is doing nothing. To do that though I would have to see some sort of light at the end of the European tunnel, and that is not likely forthcoming.

The only significant portfolio change I made last week was to sell my position in Jaguar Mining, and using the subsequent cash to increase in my positions in both Aurizon Mines and Atna Resources. There will be more to come on both Atna and Aurizon in a future post. I see Atna in particular as a interesting and soemwhat unique situation. Atna recently received 100% interest in the Pinson deposit. This is a game-changer for the company, and one that is not even close to being priced into the stock price. Because Pinson does not have a full feasibility study complete, or even a PEA, investors are not aware of the economics of this high grade underground project. But more on this later. For now though I want to spend a few minutes talking about Jaguar Mining. Since I have written about the company fairly extensively, I think its worthwhile to review why I have now chosen to go the path of full liquidation.

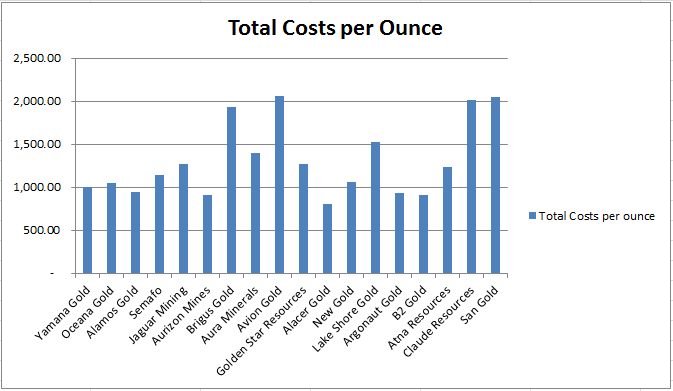

I can point to a number of reasons for getting out of Jaguar Mining. At the top of that list is the company’s inability to generate free cashflow, even though the gold price has risen some 40% over the past 9 months. The way that Jaguar has managed to match any increases in operating cash flow with correpsonding increases in capital outlays is uncanny.

Let’s compare this to another holding of mine, Aurizon Mines.

Aurizon, on the other hand, has done exactly what you’d expect a company to do in a rising gold price environment. They have generated a great deal of cash. The cash position of Aurizon has increased almost $40M since the beginning of the year. Jaguar’s cash position, on the other hand, has actually decreased if you remove the effect of the convertible denbenture issued in the first quarter.

Of the two companies, the one that you would have to say is in a better position for expansion would be Aurizon. But never a management team to be daunted by lack of available funds, Jaguar said in a separate press release that they are going forward with the development of the Gurupi project.

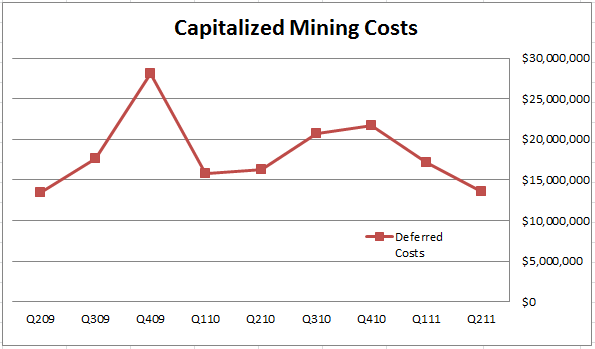

At the beginning of the year Jaguar provided a longer term outlook of what to expect from the company. I’ve provided one of the tables from this outlook below. Pay particular attention to the requirements of Gurupi (which as the table indicates was supposed to start development this year, by the way), an estimate that one analyst on the conference call referred to as outdated and not in the “that number is too high” kind of way.

Jaguar is going to be forced to raise a lot more capital to fund Gurupi.

On top of that, Jaguar plans to refinance their outstanding debentures with senior debt. Between the Gurupi financing and the convertible refinancing Jaguar is looking at a bond offering of $400M+. This seems like a bit of a heroic expectation for a company that is struggling to produce any free cash flow at record high gold prices.

Another analyst on the call pointed out that the market might not be quite as responsive to new debt from the company as Jaguar management seems to think it might be. Quite reasonably, the analyst referred to the existing debentures, which the market is currently valuing at a 13% interest rate. He speculated that the market is suggesting that Jaguar debt would take a 15-17% coupon.

Management said that the offer sheets they had received were in the 9-11% range. Forgetting for a minute that 9-11% interest rates are extremely high, you have to be a bit suspicious of the company’s ability to raise money at this level when there are debentures outstanding that carry the upside conversion option, at a 20-40% discount.

I could go on.

I bought Jaguar because in the low $4’s it was a undervalued NAV play. The projects, if you tally up the value of each, are worth around $6-$7 per share, and maybe more at $1800 gold. But at $6 per share, which is about the average price that I unloaded my position at, that NAV story is replaced by a cashflow story that to be quite frank about it, just isn’t there.

I’ll stick with Aurizon, with Atna, and with the big boys like Newmont and Barrick.

{kind=link}