Letter 27: My Deutsche Bank Short, Increasing my Gramercy Capital Long, and trading in OceanaGold for Golden Minerals

Why I am Short Deutsche Bank

Its been a while since I talked about my shorts.

I typically wouldn’t have much in the way of shorts. At the most they would make up a couple percent. I don’t have a great track record of predicting when companies are going to fall.

I tend to pick them too early. I think its a classic trap of a value investor; you see an overvalued company and you conclude that it has to go down. Unfortunately that is not the way the market works; until there is a catalyst a stock can continue to become more overvalued to the point where you as an investor have no value.

Right now, however, shorts make up a fairly significant percentage of my account. About 15% (though not the practice account I post here because shorting is not supported by RBC). These are extraordinary times.

I have a small short in Argonaut Gold that I mentioned last week. I continue to have a short in Salesforce.com that has done quite well as the cloud computing phenomenon has come back down to earth. I have a short on Tourmaline, an albeit well managed but highly valued natural gas producer in an environment of dismal natural gas prices.

The biggest short I have is in Deutsche Bank. It makes up about 8% of my overall portfolio. I added to it over the last week as DB made yet another failed attempt to stay above $40. Together with a smaller short in UBS, it makes up my “at some point Europe is going to go down the toilet” bet.

Why Deutsche Bank? Simple thesis – it is insanely levered. Here is a snapshot of the European banks common equity to assets. Note the location of Deutsche Bank on the x-axis.

Since that time Dexia blown up.

Jim Grant makes the same point on Deutsche Bank about half way into this interview on CNBC.

Wholesale Funding

The other thing about Deutsche Bank, and to a lessor extent UBS, is that they are not strong depository institutions. What that means is that they do not have a large base of deposits to fund their assets. Particularly in the case of Deutsche Bank they go to the market and borrow money from other banks, from money markets, from pretty much anybody who is willing to lend it, and this is the money they use to fund their lending. When times are good this is a great strategy. Deposits are a more expensive (higher interest rate) form of funding then these wholesale channels (wholesale is kind of the catch-all term that defines all these short term lending sources). But when times are bad, these channels dry up a lot faster then deposits. They can be called quickly in the event of a loss of confidence.

A good proxy for the degree of reliance on wholesale funding is the net stable funding ratio. FT presented the ratio, along with the following graph, in an article a few months back.

One good proxy for this reliance is the net stable funding ratio (NSFR) we have regularly discussed in all our recent sector and company reports. Currently, CASA and SG are among the Euro banks with the lowest NSFR, together with Bankia, UniCredit, Commerzbank + Intesa.

While Deutsche Bank isn’t the worst of the bunch, it is far from the best. Combine that with high leverage and you have a recipe for instability.

All the Devils are at Deutsche Bank

I mentioned last week that I was reading “All the Devils are Here”. Towards the end of the book there is a chapter on the demise of Countrywide. Countrywide, like Deutsche Bank, was not a depository institution. As a result, like Deutsche Bank, Countrywide depended on the wholesale funding markets to fund their assets (in their case mortage loans). It was pointed out by Kenneth Bruce, the Merrill Lynch analyst that followed the company at the time, that “liquidity Is the Achilles Heel” of Countrywide. Said Bruce:

“We cannot understate the importance of liquidity for a specialty finance company like CFC. If enough financial pressure is placed on CFC, or if the market loses confidence in its ability to function properly, then the model can break.”

The difference, at least so far, between what happened to Countrywide and what has happened to Deutsche Bank is that Countrywide went to the Federal Reserve and pleaded with them to use their emergency lending authority. The Fed refused, perhaps because months earlier CFC had switched away from the Fed’s regulatory oversight to the Office of Thrift Supervision (OTS) because they saw greater advantages (read: less strict rules).

Thus far Deutsche Bank has been saved by the unlimited lending arm of the ECB. They certainly would be struggling to fund themselves through their traditional wholesale channels. We know that liquidity has dried up in Europe. We know that the wholesale funding markets (money markets, collateralized repo’s) are getting harder to access and are acceptable less and less forms of collateral (read: German bonds are the new holy grail).

Meanwhile while DB has reduced leverage to the peripheral sovereigns over the last year, they still have fairly significant gross exposure. This gets lost in the shuffle however, because the news tends to focus strictly on the sovereign exposure. For example, this WSJ article points out that:

Deutsche Bank has a relatively low total of €4.4 billion in exposure to the sovereign debt of the troubled euro-zone nations. Its exposure to Italy grew to €2.3 billion at the end of the third quarter from €1 billion at the end of the second quarter…Deutsche Bank has largely hedged its Italian exposure, much of which was inherited as a result of its Postbank acquisition, from €8 billion at the beginning of the year.

True… but gross exposure to the region is significantly higher. You have to look past the sovereign. Below are estimates of DB’s gross exposure to credit in the periphery. DB equity is about E53B for comparison.

Having significant exposure to financials, corporates and retail in Italy, Ireland and Spain is not a good thing right now. Given the austerity measures being imposed how bad do you think the inevitable recession is going to be in these countries? I think its going to be pretty bad.

You might also ask a question about what othe exposure DB has. Given that assets total around E2.2t and periphery exposure is around E100B, clearly there are other things on the balance sheet. Well as it turns out they have a fair bit of exposure to something nebulously called “credit market debt”.

As per a WSJ called “Old Debts Dog Europe’s Banks”:

Four years after instruments like “collateralized debt obligations” and “leveraged loans” became dirty words because of the massive losses they inflicted on holders, European banks still own tens of billions of euros of such assets. They also have sizable portfolios of U.S. commercial real-estate loans and subprime mortgages that could remain under pressure until the global economy recovers.

The Journal provided the following comparison of this “credit market debt” exposure for the various European banks:

Again to the Journal, this time speaking specifically about the make-up of Deutsche’s credit market assets:

Legacy assets are also haunting Deutsche Bank AG. The Frankfurt-based bank is holding €2.9 billion in U.S. residential mortgage assets, including subprime loans. It has an additional €20.2 billion tied up in commercial mortgages and whole loans. The bank says it has hedged nearly all of its residential mortgage exposure.

Analysts at Mediobanca estimate that Deutsche’s exposure to such assets amounts to more than 150% of its tangible equity—a key measure of its ability to absorb unexpected losses.

Deutsche Bank said it plans to let most of its legacy assets mature, so it won’t face losses selling them at discounted prices.

And don’t forget the fact that the main business of Deutsche Bank is investment banking. With the seizing up of credit in Europe, that business has to be feeling some pain. Indeed, after reporting 3rd quarter results the CEO Josef Ackerman said:

“During the third quarter, the operating environment was more difficult than at any time since the end of 2008,” adding that the bank’s performance was “inevitably” hit.

Management Matters

One final point. Deutsche Bank announced back in July that their long time CEO (Ackerman) was stepping down and would be replaced by co-CEO’s. now getting back to the book All the Devils are Here, if there was a common trait that pervaded all of the worst of Wall Street in the years leading up to the 2008 crisis, it was turmoil within upper management. Maybe the change over at DB will go swimmingly. But co-CEO’s sounds like a recipe for secrecy and oneupmanship to me. As the WSJ reported:

The bank is resorting to a dual CEO structure for the fourth time in its history, despite the potential for conflict and even a power struggle between the two, because handing the reins to Mr. Jain alone was seen as too much of a culture shock, according to people familiar with the matter...The bank has been working to diversify its earnings mix away from investment banking, which has recently accounted for about 70% of its profit. In the third quarter, investment banking accounted for less than 10% of total profit.

In the end…

Look I don’t have crystal ball that says that Deutsche Bank is inevitably going to fail. I’m sure there are plenty of analysts out there that understand the in’s and out’s of the company’s business better than I have time to do. What I do know is that the evidence points to the conclusion that Deutsche Bank is a bank very dependent on the ECB. The whole bet on Europe is, in my opinion, a bet of whether the ECB eventually steps up to the plate and starts bailing out the sovereigns (and either directly or indirectly the banks) or they don’t. If they don’t, DB, being very dependent on ECB largesse, has to do poorly. Thus, the hedge.

The Confusing Balance Sheet of Gramercy Capital (and yet I’m still buying more)

Gramercy has been in a bit of a free fall of late.

The decline in the stock price to the $2.30 area made me want to re-evaluate my position in the stock. Not so much with the intention of liquidating my position mind you. I was far more interested in whether I should buy more.

I began by stepping through the Gramercy third quarter 10-Q, followed by the recent filings, in particular the 8-K filing made on December 8th that detailed the pro-forma financials ex-realty. Unfortunately, as tends to be the case with Gramercy, the review left me with as many questions as answers.

I have to say that Gramercy has some of the most difficult financial statements that I have ever seen. I spent two years researching Dynegy and even with all their SPE’s and off-balance sheet transactions it was still easier to understand what they were up to then it is with Gramercy. The problem with Gramercy is a combination of

- it being difficult to determine what is held at corporate and what is held in the CDO’s and until recently realty

- there being overlap between the holdings of corporate and the CDO’s and realty and so some items are netted out even though their liability is non-recourse to corporate

- the fact that the CDO’s are basically a black box unless you have access to the managers report and that is not public knowledge (I am still using the only publicly available report which is from March and so therefore somewhat dated)

- the company really doesn’t make much of an effort to clarify any of the above.

Anyways, with all that in mind, lets try to draw some conclusions.

Net Asset Value vs. Book Value

One positive of late is that for the first time it is relatively easy to determine the book value of Gramercy corporate. Up until now the mess of CDO and Realty divisions made it a nightmare. With Realty gone, proforma statements were released in mid-December and stated clearly that there are $260M in assets, $40M in liabilities, and $88M in preferred.

Book is $132M or $2.60 per share. Done deal right?

Wrong. Everything is more complicated then it seems with Gramercy.

The first complication is that Gramercy corporate owns a number of reasonably senior securities from their CDO. Because these securities are also liabilities (in the CDO) they are netted out and disappear on the balance sheet.

“In addition, as of September 30, 2011, the Company holds an aggregate of $54.0 million of par value Class A-1, A-2 and B securities previously issued by the Company’s CDOs that are available for re-issuance. The fair value of the repurchased CDO bonds is approximately $40.3 million as of September 30, 2011.”

However the liability in the CDO is, like all else in the CDO, non-recourse, and so the asset on corporate is legitimately accreditive to book. So even though the value of the notes are not on the balance sheet, they should be.

The next thing that is terribly confusing is what is included in the real estate investments. According to the pro-forma those investments total about $80M at cost:

And maybe that’s the end of the story. The problem is that the company said in their last 10-Q (which is for the same period as these pro-forma results) that real estate assets after the transfer of the realty division was complete would total $121.3M with corresponding mortgages held in the CDOs:

And maybe that’s the end of the story. The problem is that the company said in their last 10-Q (which is for the same period as these pro-forma results) that real estate assets after the transfer of the realty division was complete would total $121.3M with corresponding mortgages held in the CDOs:

“The Company anticipates that all transfers will be completed by December 31, 2011, after which, the Company expects to retain a portfolio of commercial real estate with an aggregate book value of approximately $121.3 million, encumbered by non-recourse mortgage debt held by the Company’s CDOs totaling $94.3 million, which mortgage debt is eliminated on the Company’s consolidated financial statements.”

The (unanswered) question that I have is whether the netting out of the assets and liabilities of these real estate assets includes is included in the above $80M? My guess is that it doesn’t; that because the asset and liability are both on the balance sheet (with the liability being within the CDO) they are netted out just like the CDO notes. But I’m not sure. If I’m right, then the true book should reflect the extra $27M of the commercial real estate portfolio above and beyond the mortgage debt.

But what’s it worth?

The last, and perhaps most ambiguous question about the balance sheet is what the assets are actually worth if they are sold. As noted above, the real estate investments are recorded at cost. I assume the $121.3M is a number also recorded at cost, though that is not clear. But what could this real estate fetch today? Is it substantially less then cost? It wasn’t clear in the pro-forma whether Gramercy chose cost because it was the lessor of cost/fair value, or because they just had to value them at cost.

As for the CDO’s, the notes are recorded at fair value, which means they are being valued at quoted market prices. In reality the CDO debt is either worth all or nothing. Either the CDOs have the cash in run-off to pay back the A-1, the A-2 and the B or they don’t, so its more likely the number is either $54M as they are fairly senior notes and so they are likely to get paid off.

To help make my point with the real estate investments take a look at one of Gramercy’s investments that you do have the information to analyze to some depth.

The joint venture 200 Franklin Square Drive, Somerset, New Jersey is carried at $558,000. Yet income from the property was $29,000 in Q3 and $90,000 for the first 3 quarters. So based on its book value it is returning 20%. I think the book value needs to be higher.

Now this is a case where the book is on the low side. There could just as easily be cases where the asset is booked on the high side. The point is, this whole valuing Gramercy is a ballpark game at best.

What is the deal with CDO-2005?

The deal is that CDO-2005 failed its over-collateralization test again in October after having passed it the previous quarter.

Presumably the main catalyst in the failure was the write down of whole loans to Las Vegas Hilton and Jameson Inns. Together these loans were carried at $42.5M on the CDO books.

The question now is just how far underwater is CDO-2005 and will that CDO be able to cure itself and begin to paying out money to Gramercy again? Well while I don’t have the most up to date data, I can still take a stab at answering that.

As of March 2011 CO-2005 had an outstanding note balance of about $741M. Presumably in curing that balance the first time round (it was cured in July), the note balance was reduced somewhat, to lets say $700M. Based on the current over-collateralization of 115.53%, that would mean current assets in the CDO are around $810M. In order to pass the test with $810M of assets, the outstanding note balance has to be reduced to $686M. In other words the company needs to see a $14M cash infusion to get the CDO passing again and begin seeing cash flow to corporate.

Where is that cash going to come from? From the interest that is diverted to paying down principle for as long as the CDO is not in compliance. As shown below, that interest, which was paid out in the previous quarter as the CDO was in compliance, is a little less than $5.5M per quarter.

The other possibility is that as loans within the CDO are paid off both the numerator and the denominator of the over-collateralization test drop (the assets decline as well as the notes that are paid off with the proceeds). Eventually this would cure the CDO though it would take a lot more run-off, about $90M by my calculation.

The conclusion here is that CDO-2005 is not dead by any means, but that we should not expect to see cash flow from it for another couple of quarters.

Management Incentive

One of the concerns with any of these REIT’s is whether the interests of management are aligned with shareholders. The concern is generally that management wants to keep getting paid and so they won’t necessarily jump at the chance to sell the company, instead preferring to live of the cashflow (and in a worse case the cash) to pay their salaries and bonuses. I think this is the concern of Indaba, who as a large preferred shareholder is attempting to add a board member to get that cash used in share holders interests.

Along those lines though, it looks to me like recent efforts have aligned management fairly well. The have been provided with incentive to sell the company by the end of June 2011. Below is a list of significant shareholders of the company published as part of a 14C on December 19th. Executive Officers as a group own 2.3M common shares in the company, including over 700,000 shares owned by Cozzi.

What I Think

Adding it up, there is no question that there is a lot of question marks here in the numbers. It is difficult to determine the true value of the real estate owned. It is difficult to determine when and if CDO-2005 will cure. It is difficult to know with confidence whether there are loans in CDO-2006 that may fail, causing it to fail its over-collateralization test and thus putting the company in the position where there really is minimal cash flow coming into corporate.

The best I can do is to take the fact that the book is $2.40/share, that $150M of that book is cash, that there is another $50M off balance sheet that is invested in higher end securities in CDO-2005 and CDO -2006 that are almost certain to pay off at par eventually, and that given that the US economy appears to be stabilizing and not falling back into a severe recession, it is reasonable to presume that CDO-2006 will continue to pay out $7M of cash to corporate every quarter for the forseeable future.

Given all of this, I added to my position in Gramercy this week, and I will continue to add as long as the stock trades below the $2.40 level. I was sad to see that we had a bump up in the price on Friday. We will have to see if it sticks. If not I will be ready to buy more.

Gold (and now Silver!) Stock Update

Apart from Gramercy, I made a few small changes to my portfolio this week. I sold out of OceanaGold at $2.45. I had planned on holding the stock until the $2.60 range again but I saw better opportunities but was reluctant to become even more leveraged into gold stocks at this point.

That better opportunity that I saw was Golden Minerals. My broker told me to get in on a private placement of AUM back in the fall of 2010. Nah, I don’t think so I said. I think that placement was at $18. The stock got as high as $24. I bought it this week for $6.25. Pays to wait.

Golden Minerals is another one of these junior explorers (though they do have a small silver mining operation in Mexico now) that has gotten obliterated in the last year. The stock is down 75% off its high. Luckily for the company, that private placement went through with some other poor bastards taking the brunt of it, and so the company is flush with cash. With AUM you are paying $6 and getting a company with a little over $2/share in cash and an indicated and inferred resource of a little over 6Moz ounces of gold equivalent at a 50:1 silver to gold ratio.

The company’s producing mine in Mexico, Velardena, looks promising, but it remains to be seen if they can ramp up production as expected (they want to be producing 4,000oz of gold and 214,000oz of silver by Q4 2012). More interesting to me is the project in Argentina, where they have a fairly high grade (300g/t) silver deposit that sits at 60Moz right now and looks like it has lots of room to grow.

At any rate, its another example of a beaten up junior that was worth a heck of a lot more a year ago then it is now. It seems like a reasonable speculation that it will recover at least some of that value this year if gold and silver prices don’t crater.

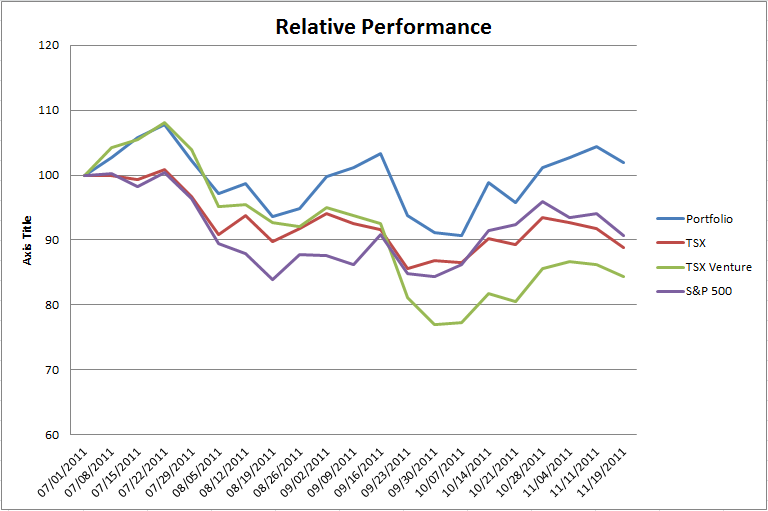

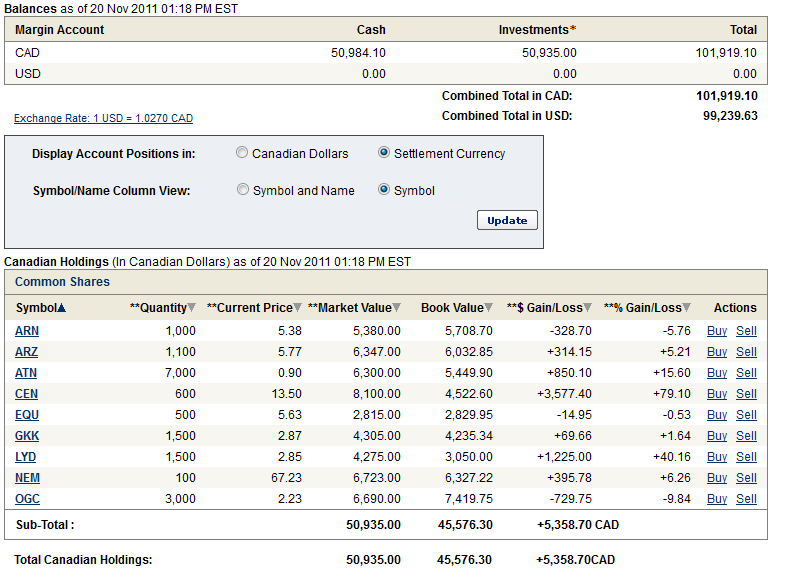

Portfolio