Week 155: Still Cautious

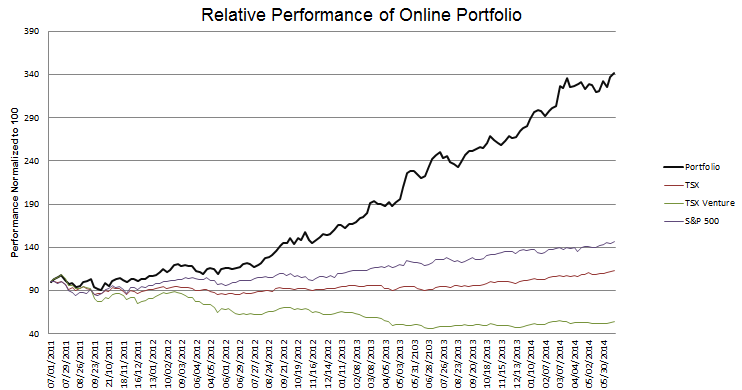

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

In my last update I stated that I had about a 20% cash position and wanted to increase that position heading into the summer. We are now one month further along and my cash position stands at something less than 5%.

Nevertheless I do remain somewhat uneasy about what happens to the market post QE. As I wrote about in my last update:

Twice the quantitative easing policies of the Federal Reserve have ended and twice the market has gone into a tailspin.

I came across what I thought was a very good interview of Richard Duncan on the website Valuewalk. I read his first book, The Dollar Crisis, a number of years ago and I still pull the book out every year or so to go through the concepts another time. I have followed Duncan ever since. The video rather long, but in my opinion Duncan describes what current drives the market right now and summarizes why I am uneasy.

I view a number of the stocks I own right now as shorter term trades with (hopefully) immediate catalysts. I have been reducing positions that I would consider likely to have a lower bottom in an event of a correction. And I have been buying gold stocks. So even though I have added a few positions and reduced my overall cash position, I feel like I am continuing to reduce risk. I tweeted the following about my purchases of gold shares: Read more