A New Bet on Hercules Offshore

I have owned Hercules Offshore (HERO) for a couple of weeks now. I tweeted about my position right after I bought the stock. I think the stock has been hit too hard on concerns about drilling rig supply/demand and that a change in sentiment could send the stock back up to the $6 to $8 range.

Hercules performs drilling services in the offshore market. Their focus is shallow water drilling; their marketed fleet consists of 27 jackup rigs and 23 liftboats. Fifteen of their jackup rigs are contracted in the Gulf of Mexico with the rest located internationally in the Middle East, Southeast Asia and Africa. In 2013 jackups made up 83% of revenue, with the liftboats taking the rest.

Why I took a position

I took a position in Hercules based on the following:

- The stock was hit pretty hard at the beginning of the year because of concerns about supply/demand of new build jackup rigs and the impact this could have on Gulf of Mexico day rates

- Those concerns have some validity but are not immediate. For 2014 the new supply (32 rigs total, 24 rigs that aren’t contracted) will be absorbed by the market.

- Looking out to 2015 there is significant supply of new builds but much of the supply is being ordered on spec and by buyers who are not established operators. It remains to be seen how much is built or who will operate it if it is built.

- The Gulf of Mexico is also not the most profitable destination for a new build, which should help insulate Hercules from the new builds to some degree

- The current price of the stock (I add at $4.50 but its now a bit higher at $4.80) reflects the concern about supply/demand and very little optimism that day rates will remain strong in 2014 and continue to hold up for 2015

- Hercules is quite levered (their market capitalization is around $700 million and they have $1 billion of net debt) so a small change in sentiment about the company (either via a reappraisal of the Gulf of Mexico situation or one of the other catalysts I will get to shortly) can have a big effect on the stock.

- Based on the first quarter results the stock is trading at a reasonable 4.5x EV/EBITDA multiple

Other Considerations

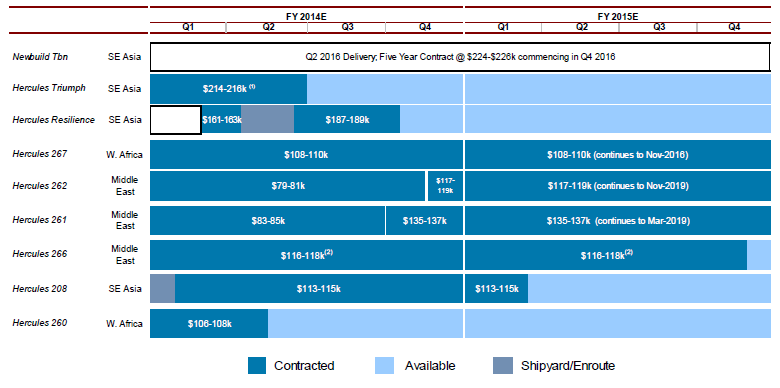

In addition to the above another near-term catalyst would be the agreement of a long-term contract for two higher end jackups, the Resilience and the Triumph.

Currently both of these rigs are operating on short-term contracts at lower-margin rates. The Triumph is on contract in India, while the Resilience is in Southeast Asia. Hercules has already said they have a multi-year opportunity on the table for the Triumph. The contract would be at a higher day rate, expected to be in the low $200,000 per day, versus $180,000 currently. The company says the contract has been agreed to, with the remaining hurdle being compliance issues with the host country. News that its finalized would be a positive catalyst.

Apart from the Resilience and the Triumph, Hercules has five of their six remaining international rigs contracted for 2014 with four of them contracted for 2015. It looks like the 2015 day rates are on average higher than 2014.

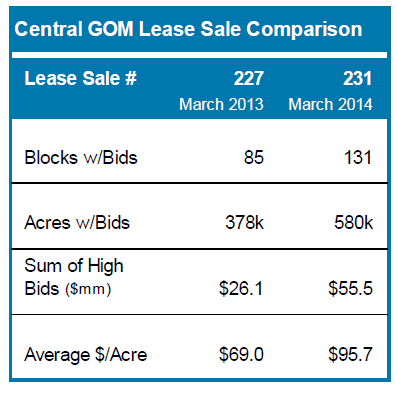

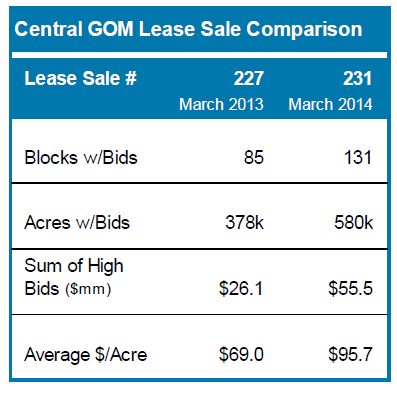

The rest of Hercules rigs are operating in the Gulf of Mexico. Rigs in the Gulf are typically on short term contracts, only 3-4 months, so the visibility there is always limited. I already have discussed the state of GoM supply and demand in my points above. Drilling in the shallow gulf is expected to increase in the coming quarters. The company provided the following comparison of lease sales in 2013 versus 2014 to illustrate the increase in interest.

New build in the North Sea

New build in the North Sea

Hercules broadened its revenue base further into the higher end jackup market with the recent long-term contract in the North Sea. It’s a 5 year deal with Maersk for a new build jack-up at a $225,000 day rate for total contract value of $420 million. The cost of the rig will be $236 million.

The contract is significant in size relative to the company; it increased the company’s backlog to $1.4 billion and further extends Hercules into the higher end jackup market. The contract will begin to generate revenues in 2016 so it will begin to be factored more heavily into the analyst models towards the end of this year.

A tough business but still a good opportunity in the short run

While there is a lot I like about Hercules, I recognize that this is a tough business. It requires heavy capital expenditures up-front, demand relies on oil and natural gas, which makes it cyclical, and the barriers to entry are not that high; witness the number of new rigs being built by unknown participants. Like many of my positions, the business is good for a trade off of unjustified pessimism but not necessarily something I would sock away money in for years to come.

Offshore drilling seems to be one of those businesses where its hard to pinpoint what free cash is actually being generated. You are either at the bottom of the cycle and struggling to get by or at the top and shoveling money into new rig expenditures. The rigs have very long lives; some of Hercules rigs are 40+ years old. The actual cash generated by each rig depends on so many things over such a long horizon that I find it difficult to make a call on long term sustainability.

But in the short-run, which is my concern here, the catalysts and the leverage are there. I’ll continue to monitor the risk: that rig supply overwhelms demand, but in the meantime a couple of quarters with day rates current level and a lock-up of one or both of the Triumph and Resilience with a long-term contract and its not hard to see the stock trading at $6 or even $8.

No go on the contract for the Triumph. Setback for the company: http://www.sec.gov/Archives/edgar/data/1330849/000133084914000039/jun14fsr8k.htm

I bought Noble Corp at about $31.00 and am happy with that so far. Sounds like you have a much more informed perspective on this industry than I,but was wondering if you had considered it.

Sorry for being so slow to reply. I did look at Noble when I looked at HERO and its a bit different play since they are also into the floaters. I havent done as much work on the floaters and where supply/demand is there. They didn’t strike me as being as priced for failure as HERO is. But I’ve been thinking about company’s like Noble and Transocean as other options; these stocks are not participating in the bull market and so a swing in sentiment could lead them up quickly. Do you have any thoughts on the floating market?

I got out of HERO after the news but then jumped in again a couple days ago at $4. I’m still waffling what I want to do with the stock. Since I wrote this I’ve done a lot more work on the jack-up market and I’m really not sure what happens in 2H 2015 when the new builds start to come on-line. So many of them are built on spec and with 5-10% down payment where the buyer could just walk away.