Week 155: Still Cautious

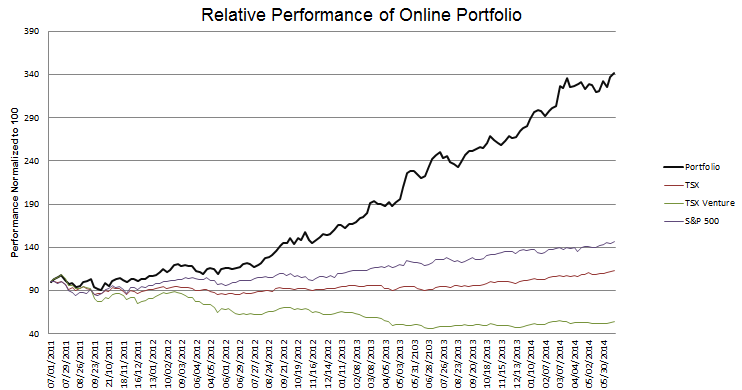

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

In my last update I stated that I had about a 20% cash position and wanted to increase that position heading into the summer. We are now one month further along and my cash position stands at something less than 5%.

Nevertheless I do remain somewhat uneasy about what happens to the market post QE. As I wrote about in my last update:

Twice the quantitative easing policies of the Federal Reserve have ended and twice the market has gone into a tailspin.

I came across what I thought was a very good interview of Richard Duncan on the website Valuewalk. I read his first book, The Dollar Crisis, a number of years ago and I still pull the book out every year or so to go through the concepts another time. I have followed Duncan ever since. The video rather long, but in my opinion Duncan describes what current drives the market right now and summarizes why I am uneasy.

I view a number of the stocks I own right now as shorter term trades with (hopefully) immediate catalysts. I have been reducing positions that I would consider likely to have a lower bottom in an event of a correction. And I have been buying gold stocks. So even though I have added a few positions and reduced my overall cash position, I feel like I am continuing to reduce risk. I tweeted the following about my purchases of gold shares:

With Indian election and hopefully change to import restrictions my thought is gold may move higher into summer. Been adding some gold names

— L.Sigurd (@LSigurd) June 11, 2014

India is the largest consumer of gold. For the last year they have been restricted in their imports. When Indians were last able to import gold, prices were 30% higher. This seems to me to set the stage for a big increase in demand when and if tariffs are lifted.

I didn’t tweet names of companies at the time because I wasn’t really sure which of the gold stocks I bought I would actually hang onto. I bought a basket, five companies on the day of the tweet, with admittedly only a little research, but I have since sold two, and now hold the following with some conviction: Argonaut Gold, Rio Alta Mining, and Endeavour Mining. I will talk about the latter two in this post. My timing of such things is not generally stellar but in this case I was quite bang on. All three companies are up substantially since my purchase, as are most gold shares.

I also beefed up my oil weighting, adding both Mart Resources and Bellatrix Exploration (which I separated into its own post here). Oil prices are on the move up and having spent a lot of time on Iraq over the last couple of weeks, I am quite concerned that the situation gets further out of hand. These positions therefore serve two purposes. First, they expose me to companies with fairly immediate catalysts and exposure to a rising commodity. Second, they provide somewhat of a hedge to the airline stocks I own, as they will not do well if oil continues its ascent.

I did exit two positions this month, Supercom and Hercules Offshore. I will discuss my reasons below. I also lightened up on Chipmos, Swift Energy and Yellow Media to small degrees. Finally, for those who have followed me on twitter, I sold Bimini Capital Management, which I do not own in the portfolio tracked here but had tweeted about a number of times, a couple of weeks ago. I took a rather roller-coaster-like double on it, having bought the stock at 35 cents only to watch it fall as far as 11 cents before rebounding into the mid 70’s, where I sold it.

With that all said, onto the stocks.

Rio Alto Mining

Rio Alto (RIO) has really taken off since I bought the stock. I began to add a position a couple of weeks ago at $1.90, and continued to add when the stock got to $2. Since that time it has climbed all the way to $2.50. I’ve actually started to sell the stock simply because it seems to be in the “too far too fast” category.

Rio Alto has a single oxide deposit in production called La Arena that is in Peru and doesn’t have a long mine life. Under the oxide there is a larger sulphide deposit that is primarily copper. Up until recently the company was actually quite similar to Timmins Gold, which I owned for a couple of months earlier this year – trading at a low multiple (4x EV/EBITDA) with a single mine and without a lot of prospects for growth outside of that mine.

What changed recently, and really piqued my interest in the company was the takeover of Sulliden mines, Sulliden owns a project in Peru that is not yet in development, Shahuindo, that is about 30km away from La Arena. Shahuindo is expected to go into production in late 2015-early 2016. The transaction was dilutive but gives Rio Alto a growth profile. I’m actually surprised the stock traded down as much as it did after the acquisition was announced. It was trading at $2.12 on the day of and as I said I was able to pick up shares well below $2.

With the move up in the stock price Rio Alto trades at about a 7x EV/EBITDA based on the diluted share count post-transaction. Even this isn’t terrible given the newly acquired growth profile. Many of its gold peers are at the 10x level (for example Argonaut Gold is). Still, so much with these gold stocks depends on momentum and the price movement of the commodity that I would be reluctant to take much of a position at it at these levels. Another drop though, perhaps precipitated by one last gasp down by gold, would be an opportunity.

Endeavour Mining

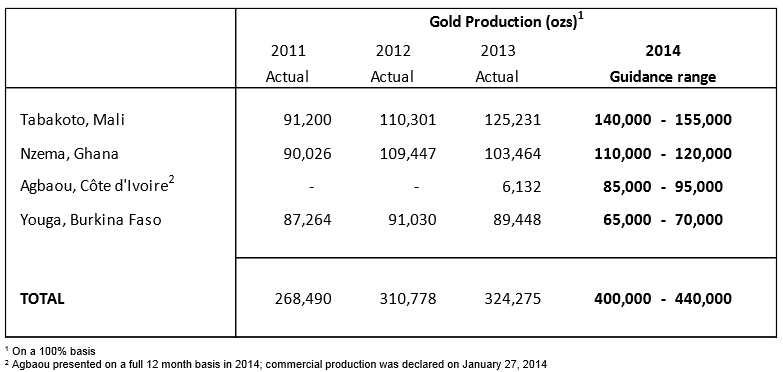

Hat-tip to @VermeulenGold for pointing this one out to me. Endeavour owns a number of mines in West Africa (Cote d’Ivoire, Mali, Ghana, Burkina Faso). They were formed via a number of acquisitions over the last four years, with one of those being the acquisition of Avian Gold, a producer which I owned for a time in 2010 and 2011 and did quite well on.

Endeavour is bringing on-line a new mine this year and is expected to grow production pretty substantially, from 320Koz to 420koz. In the first quarter the results were inline with that objective when they produced 106,000 oz.

To me, this is really a trade on the price of gold. The company had all-in site costs of $1060/oz in the first quarter and is expecting those costs to fall within the range of $985/oz to $1070/oz for the full year. This makes the company’s cash generation quite leveraged to increases in the gold price.

There may be a longer-run story here as they have optimization projects scheduled at one of their mines, Tabakoto (which is one of the mines acquired from Avian), the price probably doesn’t fully reflect the ramp at Agbaou, and they have the potential to increase production further by bringing their Hounde deposit into production, where they would reach 180,000 oz of gold for 8 years at costs of around $800/oz all-in. But I doubt I will be around long enough to see all of that out.

Mart Resources

I took a position in Mart Resources mid-week last week. I did so in part because oil prices are screaming right now and it seemed like having more exposure to oil would be a good idea. But I also did so because there are a lot of catalysts coming up and I thought this was a good time to be in the stock.

I follow Mart quite closely because I actually own a decent amount of it in another account I manage. But as I haven’t owned it in the account I track on this blog for some time and thus I don’t talk about it here. Mart is coming very close to the completion of a pipeline that they have been constructing for over the last year. This is significant as the third party pipeline they are using right now is subject to significant oil theft (averaged a rather astounding 23% of oil carried over the last 12 months and 28.8% in May) and has limited capacity, which has curtailed the company’s ability to drill new wells.

Once the new pipeline is operational, Mart will presumably have more control of the product, which should limit theft, and more importantly, have far more capacity for its own production. It’s long been my expectation that Umusadege, the concession from which Mart produces all of its oil, has many additional prospects that remain untested. Cormark Securities came out with a note this week that said they expected Mart to be able to double production once the new pipeline is operational.

Mart is also in negotiations to purchase interest in another Nigerian oil block (called OML 18) that is being sold by a consortium led by Shell. The details of where this stands are still a bit muddy. From one Nigerian source I read that they have already won the concession, while Mart said in a press release this week that they are the preferred bidder. Maybe that is the same thing, I don’t know, it is Nigeria after all. What we do know is that Mart put up a $56 million deposit that is presumably related to the block. Assuming they are awarded the block, it would likely be a second positive for the company.

Only a few days after I bought my shares the stock was hit by a roller-coaster culminating with a news release that the dividend was being deferred. I have since reviewed the financials in more detail (something I should have done already), and I should have saw this coming. With the drilling at Umusadege to fill the new pipeline and some large expenditures if they are awarded the OML 18 block, it would be hard to continue to dish out $17 million per quarter in dividends. But I don’t really see the dividend deferral as a negative. The catalyst that I hope to drive the stock is growth in production.

Sold out of a couple of stocks

Hercules Offshore

My thesis on Hercules was really built upon two legs. Performance in the Gulf of Mexico that exceeds the rather dismal expectations implied by the stock price, and contract wins for the Triumph and Resilience that sets them up for the long-term.

The news last Friday pulled out the second leg. Now we have to wait and see if management can find other contracts to keep the rigs operating. With oil prices at where they are they might be able to do it, and I might be willing to retake the bet, but I’m not in any rush.

That said, I probably wouldn’t have sold it if it had opened on Friday where it closed. But when the stock opened at $4.60, which was actually above where I purchased my shares last month, I just felt it was too high given the news. I mean, I was buying these same shares at $4.40 on anticipation of a long-term Triumph contract and with the expectation that the company had five of their six international rigs contracted for 2014. Now we have no contract and one more idled rig. The stock had to go lower.

I will look at getting back into the stock once the news is digested, the downgrades downgraded and the stock settled into a trading range.

Supercom

When I bought the stock back in January it was, as I wrote about here, on the expectation of contracts being realized that would send the stock higher. We’ve seen that and the stock is now at nearly $10 per share, which is up some 70% from the price I bought it at.

I hope I’m not being too cute here. My thought is that the market is up and due for a correction, the stock is up and looks toppy, and there is a momentum following that tends to not end well. And I’m simply trying to reduce my exposure to stocks going into the summer. So maybe this is where we see a nice dip. If I miss out on another move up then I will accept the punishment of lost profits. If it does dip back down to $8 though, I will happily buy back my shares again.

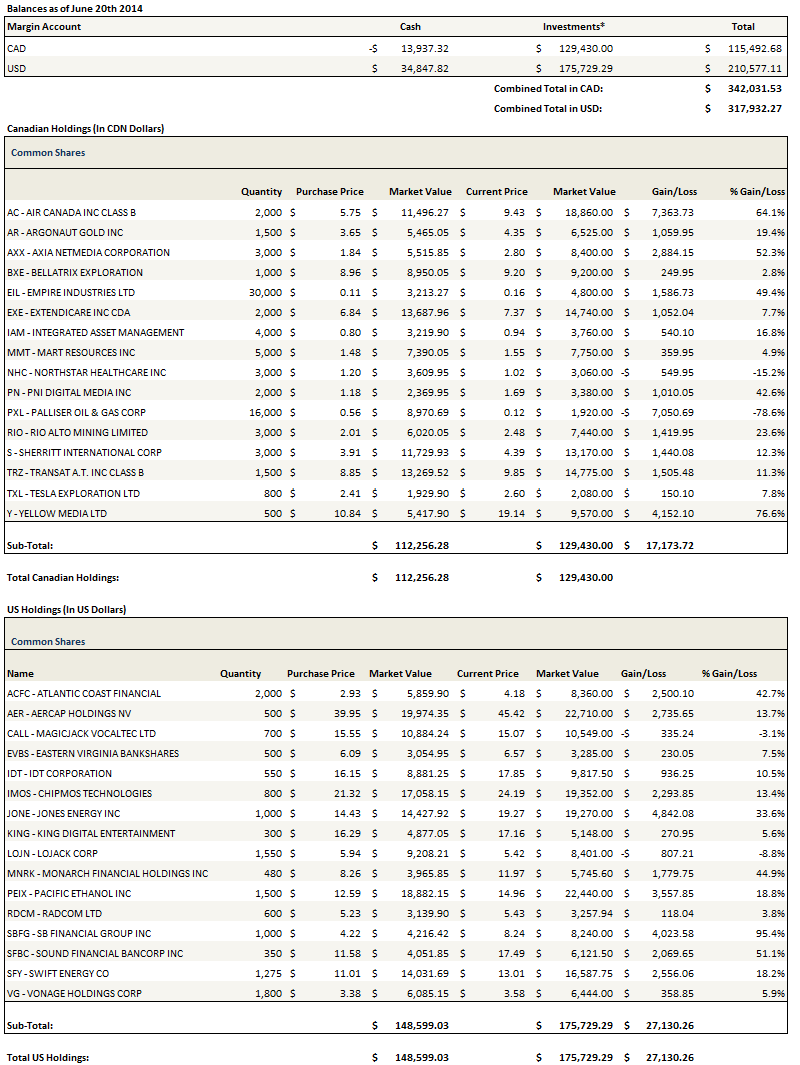

Portfolio Composition

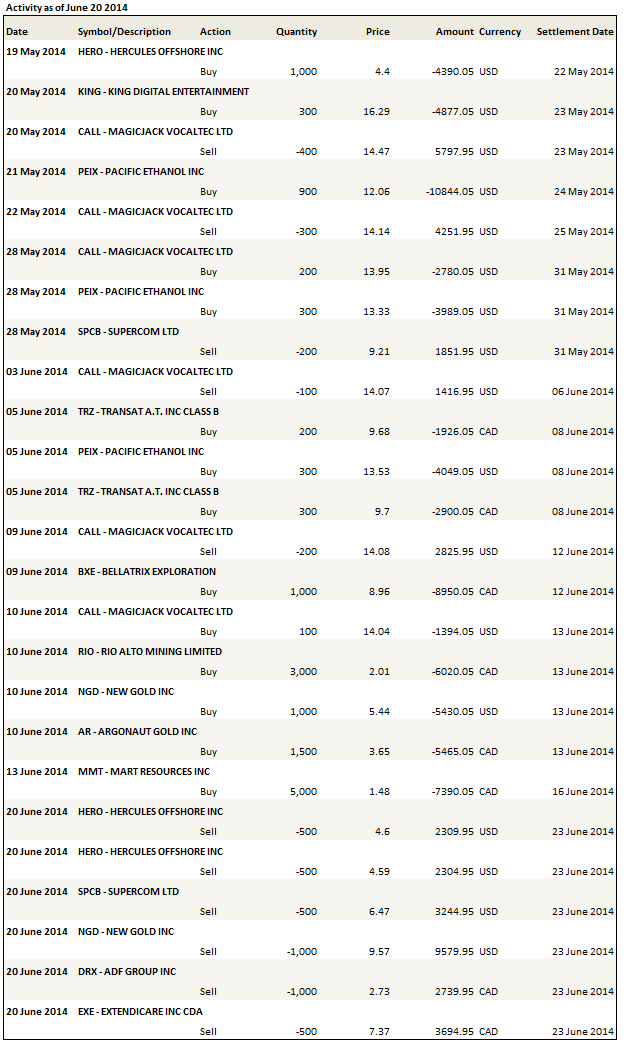

Click here for the last five weeks of trades.

{kind=link}

Trackbacks & Pingbacks