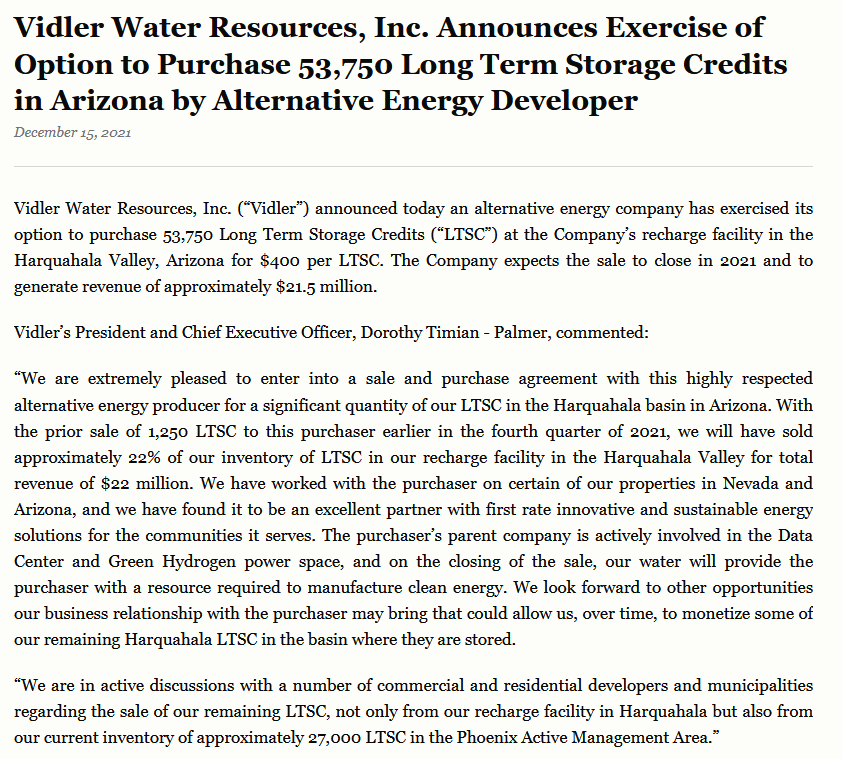

Vidler Sells Some Water

The sale of the Harquahala Valley credits went through last night.

I mentioned that there was a proposed sale a couple months ago. The closing of the sale is a de-risking event. As I said then, the Harquahala credits were probably the weakest link in the whole thesis for me.

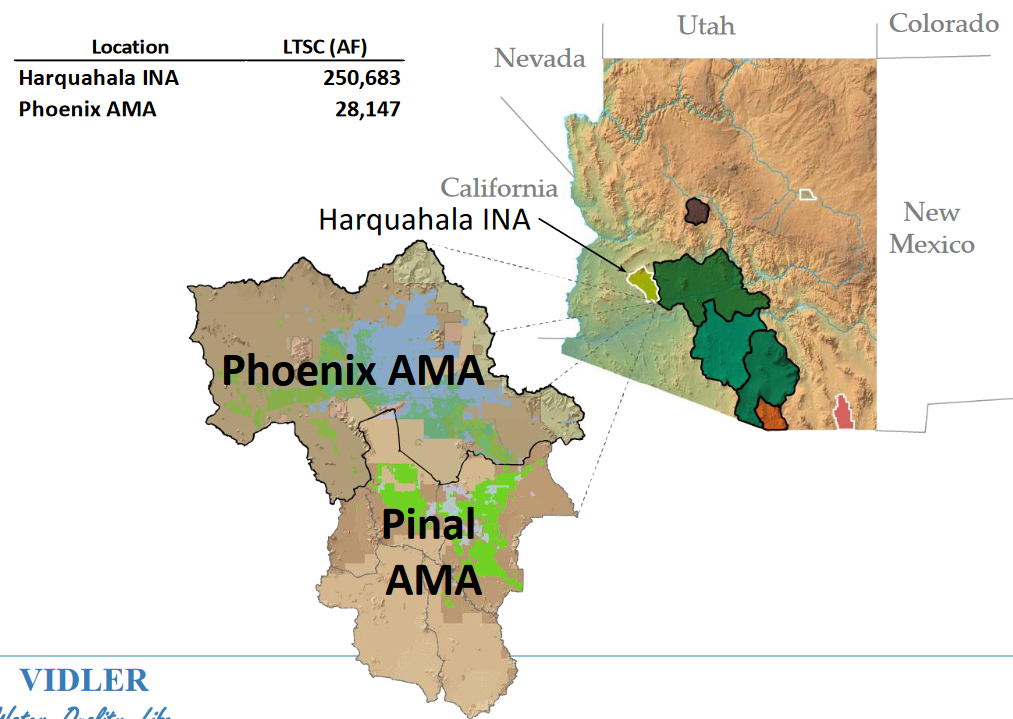

Why? Because these credits are outside of the primary metro Phoenix area and because Vidler had never really had a big sale of Harquahala credits so far. So I was not really sure if they were worth what Vidler said they were worth. I also had read about tribal water being sold on the cheap in Arizona (relatively), and so that gave me some doubts as well.

But this sale reassures me. The sale is for a material amount of credits (53,750 LTSCs, or 21% of the total) and the price tag is higher than I had been anticipating back in June (I figured $350/LTSC – this sale went through at $400/LTSC). I believe there is also the opportunity for another sale (the original press release gave a second option, see below), by end of January.

There are other interested parties. In the press release Vidler said “we are in active discussions with a number of commercial and residential developers and municipalities regarding the sale of our remaining LTSC, not only from our recharge facility in Harquahala but also from our current inventory of approximately 27,000 LTSC in the Phoenix Active Management Area.”

I suspect the amount Vidler gets for subsequent credits will be higher than what they got here (you can see that the January option is at $450/LTSC). But even if they got $400/LTSC for all the remaining Harquahala credits that would be $100 million. The Phoenix one’s have to be worth more, so I’d guess that can bring in another $14 million or so there.

If that pans out, it puts the wobbly leg of the thesis at $114 million. Or about half the market cap. Which is not terrible.

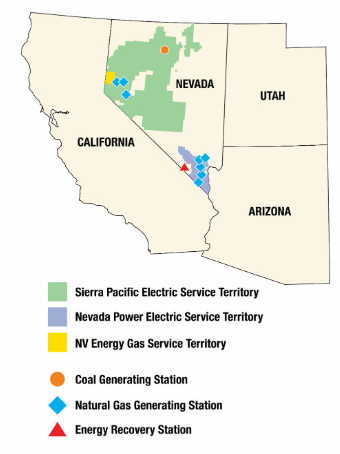

The rumor is that the buyer of these credits is Buffett. Through his owned power producer NV Energy (h/t to @Just_Credo for that rumor). If the rumor is right the parent company they mention in the release, that is “actively involved in the Data Center and Green Hydrogen power space”, would be Berkshire Hathaway’s Energy sub.

NV Energy is building a bunch of solar projects that presumably will need water.

Since 2018, NV Energy has received approval for 12 utility-scale solar projects totaling nearly 2,700 MWs of solar generation and over 1,000 MWs of battery storage which will be in-service by 2024, including the company-owned 150 MW Dry Lake solar photo voltaic project which will be collocated with 100 MWs of integrated battery storage, with the difference procured through power purchase agreements. These projects are in addition to approximately 1,000 MWs of operating solar power for which approval was obtained prior to 2018, of which 15 MW are company-owned

Berkshire just bumped up NV Energy’s capex plans by $1.6 billion.

And what is interesting about that is that the NV stands for Nevada. NV Energy serves Las Vegas and Reno, so where the rest of Vidlers water is.

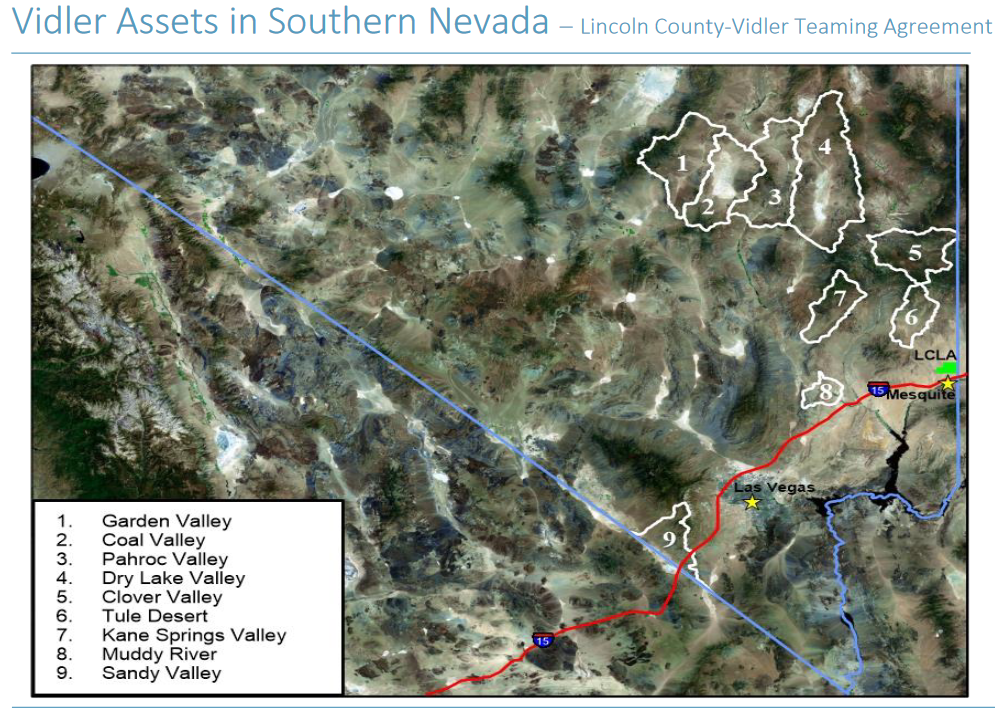

If you take a look at the projects that NV Energy is planning, some line up pretty well with where Vidler has water. The Dry Lake solar project in particular overlaps Vidler’s southern water assets. Vidler said they were in talks with a solar developer wrt their land at Dry Lake at the AGM. Vidler has about 1,000 AF of water rights at Dry Lake in addition to their land position.

And if I really want to go off the grid (in a manner of speaking) I would note that Vidler also has made applications for permits for water from 3 adjacent land packages to Dry Lake: Coal Valley, Garden Valley and Pahroc Valley.

Quite honestly, trying to figure out what is going on with these areas has made my head spin. I had basically ignored them in the past. But this NV Energy angle makes it interesting. There are some tidbits, like this filing on Coal Valley, that suggests there is a lot of water here:

Likewise you can dig around for Pahroc Valley and get some hints there is quite a bit of water there as well.

Now will any of this water be granted to Vidler? That is a whole other question and it still makes these assets pretty much impossible to put a $ value on other than $0. Note that the filing I snipped the Coal Valley paragraph from was a written opposition to a motion to designate that land, which, if granted, I think would limit the water that can be removed, maybe by quite a bit. So if that went through it would limit what Vidler could extract. Overall it’s not at all clear when and if this water will be available to Vidler.

But having disclaimed all that, what has changed with this new relationship with NV Energy is that suddenly I can see a buyer of this water if Vidler can get some of it approved. That in itself is interesting. Especially since I basically mark these assets at $0 right now.

So that’s the southern assets. The last piece of the puzzle is the Fish Springs water up by Reno. And here we had a pretty interesting development too.

The Truckee Meadows Water Authority had their board meeting December 7th (another h/t to @Just_Credo for pointing me to the meeting). You can listen to it here. Around the 25 minute mark they start talking about the American Flat Project, which is a demonstration project for reclaiming sewage water.

Vidler comes up and it’s interesting how it comes up. The board is pretty adamant they don’t want to compete with Vidler, and that they want to make sure this project does not interfere with the Fish Springs water that Vidler is waiting to provide to Reno/Sparks for new developments. There is talk about how the project managers of American Flats are already in discussions with Vidler about how this water would be used.

But most importantly, in the minutes it shows the assumptions used for the project; that they are using at least a $40k per AF number for what that water is worth:

This is essentially another de-risking event. We know that Vidler has been saying their Fish Springs water is worth $40k per AF give or take. But is it really? Well, now we can say with more certainty that yeah, it probably is.

Remember, Vidler owns 7,658 AF of approved water rights and the potential for another 3,000-5,000 more.

At $40k the approved water alone is worth $300 million+. (note: I should be clear on this – Fish Springs is a 51/49 partnership between them and the TMWA. But Vidler gets cost recovery first, which currently is $205 million and accruing at ~4.75% per year. So if it was sold today at $300 million, Vidler would get $256 million of that. More likely though this water is sold over a number of years as land is developed so the accruals will increase Vidler’s chunk. Next year the first $213 million accrues to Vidler, the year after that the first $224 million, and so on… in fact, I think you could argue that if Vidler can continue monetize all its Arizona LTSCs over the next couple years, using the proceeds to buy stock, it would be in shareholder interests to hold Fish Springs and let it continue to accrue to Vidler).

One last interesting point here. Last night when the news was announced, the twitter account @lakemeadput tweeted it out. This guy responded:

Who is Matt Johnston? He is a portfolio manager for Social Capital, Chamath Palihapitiya’s company. I can’t remember if I mentioned it before but the blog ESG Hound did a whole post on Chamath’s comments on water on his All-In podcast.

All kinds of dots connecting here.

You put all these pieces together and this story is de-risked from when I first mentioned it in June. Yet the stock price is about the same.

At some point I think that has to start changing. This $22 million that will be coming from the announced deal yesterday will help. We know a big chunk of it will go into buybacks of the stock. That will hopefully be a start.