There are a few folks that I would put in the smart guy category. These are market participants that I assume have far greater knowledge and access to information than I do. And many of them have been tweeting about how supply chain issues resolving themselves.

Comments like this:

And I could add a bunch of others. In fact, there is a real drumbeat on fintwit that is downplaying whether the supply chain issues are passed.

I have been taking a cautious view for a while now. Not an ‘all cash’ view but more cautiously positioned. More bearish index positions, smaller sized longs, some energy longs, some inverse ETFs in China and shorts of SaaS companies (that maybe are reaching the point I should take them off) and shorts some other names sensitive to China.

If fintwit is right and supply chain issues are about to end then I probably need to reevaluate this.

I always assume I am the mark at the table. There are so many market participants that have greater access to data, greater resources and more insight than I do. If my own views are different from those I assume have greater knowledge, I want to start with the assumption that I’m wrong.

So let’s go over my position until now. My caution has been based on two legs.

First, whether China is going to slow considerably from a fallout of their property sector.

Second, whether energy supply issues are going to slow economies around the globe considerably.

There is a third leg – that we’ve gone so long without a decent correction – but that only really matters if one of the first two play out.

This is all about the second leg. Which really boils down to energy supply issues. How they impact manufacturing, prices and profits.

What I am surprised by is that so many are sure that these issues are in the rear view mirror?

Implicit in supply chain issues being behind us is that energy markets are about to heal. That oil and natural gas and coal prices are about to head back down.

Try as I might, I can’t quite see how we can know this.

I can see how it might be. Because to a large degree this is all weather-driven. If there is a warm winter across the board the problems go away and by the time the next winter hits the market could be much higher.

But how can we know what the winter holds? Particularly when it is not just one region but a whole bunch of regions that seem on the precipice of an energy crunch.

I just don’t know. I do know that if energy prices are about to slide and the supply chain heal then I’m probably not that well positioned. My energy stocks aren’t going to do well. And my SaaS shorts are going to go against me.

I’m not ready to do something about this yet. I’m not convinced I am wrong. But I am aware that people that are likely more knowledgeable than me are saying the opposite, so I better keep a very close eye on it.

I’ve been on a commodity kick since sometime in April. Back then I started talking about the greening of commodities and what that might do to prices. I bought some stocks at the time on that premise.

These picks have been a mixed bag. My investment in Stelco has worked out well, but Legato Merger Corp (Algoma) has not really done much. My copper stock (Atico) has not worked out at all. My tin stocks (Cornish and Alphamin – the latter I forgot to buy for the tracking portfolio so it isn’t there) have done okay but not great.

I think though that my biggest mistake has not been sticking with aluminum.

In May when I was whole hog into the idea that green initiatives were going to drive up metal prices, I targeted steel and aluminum as the two main beneficiaries. I bought two stocks – Stelco for steel and Alcoa for aluminum.

Aluminum was interesting because aluminum is not really the same as other metals. Don Coxe used to call aluminum congealed electricity. Which is to say that aluminum does not feel the scarcities of mining (bauxite is plentiful) and (up until recently) electricity has always been abundant.

Nevertheless I was taken by comments like the following, which comes from Alcoa’s Q1 conference call. I thought that maybe this time would be different:

After I bought both of these stocks subsequently went down. I got a little nervous and decided my conviction lay more in steel than aluminum. In large part I was spooked by aluminum’s history of not really participating in commodity bull markets. So I sold Alcoa.

That was a mistake.

I sold Alcoa at $35 (I bought it at $40). While it did go down further (to around $32 at the bottom), it since has risen right back up to $48.

What is a little frustrating about that move is it has been exactly for the reason I suspected.

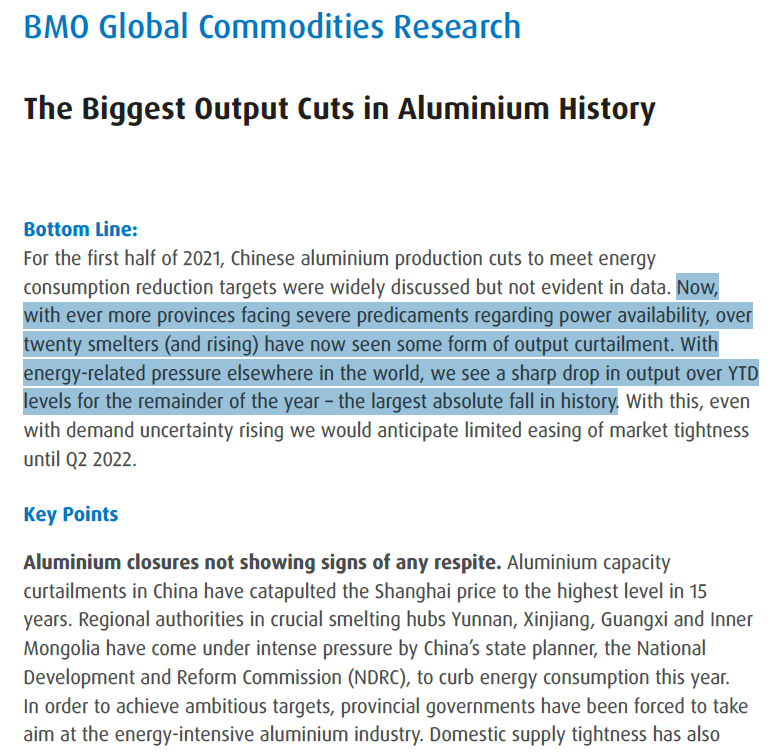

Witness the following BMO report from a couple weeks ago:

Steel has gone up too. In fact here in North America steel has stayed very strong. But steel stocks – not so much. I attribute that to Evergrande.

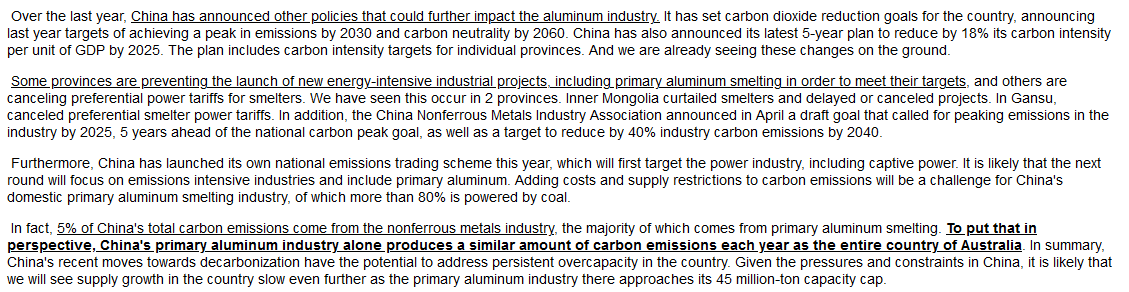

I have continued to post relevant stories on commodities on the RNO board. There are some pretty mixed to negative signals about China. Chinese real estate is up in the air and then on top of this we are finally seeing the impact of China’s carbon policy.

On the real estate/Evergrande front, as far as steel goes, I am torn. Obviously a slowdown in construction in China is not good for steel demand. But at the same time, I know that steel is 12% of China’s carbon emissions and China wants to cut carbon. So is China just going to use this as an opportunity to close high-carbon emission steel mills? I can’t really see China flooding the world with excess steel if one of their primary goals is to cut emissions.

A lot of the articles and research I post on RNO have to do with China’s carbon initiatives. Back in May these were rumblings – that China meant business and that they would be clamping down on dirty industry.

Now it seems to be happening. I’m reading about the closure of aluminum smelters and steel mills as provinces look to limit energy consumption to meet the green goals the government has put in place.

It is also impacting your run-of-the-mill mom and pop factories that manufacture all the crap you get at the dollar store, Walmart and the like. That is particularly interesting in terms of what it means for inflation in the short-run.

As for Evergrande, I stand by my initial assessment that A. no one really knows how this turns out, and B. Evergrande is more symptom than cause (a phrase that I have now heard from both Hedgeeye and Larry Summers since I wrote it – I don’t think they read the blog).

But what I will say is that everyone that is a generalist observing Evergrande seems to dismiss it as overblown. And everyone who is closely involved with Chinese business and investment says this is complicated and tricky. I’ll go with the latter here.

I didn’t buy Alcoa but I bought some Century Aluminum yesterday at the open. I also added to my position in Spartan Delta, my main natural gas play, yesterday and took a position in Cardinal Energy last week.

But other than that, I’m just sitting pretty cautiously positioned. If it had not been for a big move in Aehr last week I would not have participated in the rally last week at all.

I’ve gone short a few China related stocks (one is NOAH, the other OTIS). I’m still short some China indexes, though that has not worked out so far.

And I am short a few SaaS names.

I looked at SaaS two weeks ago and honestly, even for SaaS it seemed insane to me.

I have a consistent method that uses discounted cash flow to value the basket of SaaS names I follow. I just plug in new numbers and the new estimates and see what I get. While I don’t think DCF is very useful quantitatively with these names (I mean they always trade way above the number I get) it is useful for historical comparison. If I use the same model over and over I can see how the SaaS names are valued compared to how they were before.

What I was blown away with was how most of these companies (TEAM, HUBS, OKTA, PAYC, SQ, etc – all the usual suspects) are more highly valued than I have ever seen them. It is crazy. It was the first time I was getting DCF numbers that were less than half the share price. I mean, I always get numbers that are 20%, 30% or so less, but 50%+?

I shorted some of these last week and by Friday I was wondering if maybe they just won’t ever go down again. But yesterday’s move gave me hope again.

I am reminded of that Super Mugatu Real Vision interview from a few years ago. He was saying you have to know what you own with SaaS. And what you are now owning is largely a levered bet on rates.

These companies are all valued on the terminal value of their business. That means the value of the business years out, once growth is a bit slower and they are making oodles of cash on their customers, is what drives the value of the stock.

The value of earnings that are a long way out depend the discount rate that you use to bring those earnings back to present day value. When interest rates go down, the value of those way-out earnings go up. The argument has been made by others that some or much of the SaaS move is simply because interest rates have fallen so much.

But this also works in reverse. Now we have natural gas prices going up, energy costs of all sorts really going up, China doing things that could send other prices up at the same time SaaS valuations are the highest I have ever seen them. Oh, and rates have almost never been lower.

Hmmm… SaaS is never one to overstay your welcome with on the short side, but every dog has their day.

Markets look to be up for the second day straight. Crisis over?

Fintwit thinks so – the mocking of the Evergrande posse is well underway. The VIX is almost back to where it started. I listened to the first 10 minutes of Cramer last night and he said that the moves by Xi took the Evergrande worry “off the table”.

me? Well, I’m going to keep my cautious stance a little longer, even as right now it is wrong.

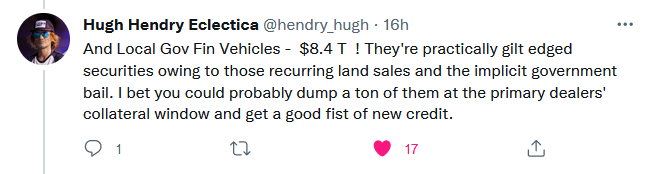

I read a thread from Hugh Hendry last night. It was – as always – cryptic.

But I get about half way through and Hendry mentions this:

And I’m like – wait, what?

So… I do not profess to know much, but one thing I know is that $8.4t is a lot of money.

It caught my attention. So I start digging.

This is primarily going to be a cut and paste excerpts/charts from FT. Please don’t forward because FT doesn’t like people using excerpts and I don’t want to get in trouble.

My take, which is evolving, is that Evergrande is kinda a sideshow here. Maybe a better description would be a symptom. But there is an underlying ailment that seems to be gaining steam and I’m not all that sure how that plays out.

Start with the basics. Property prices in China have gone up a lot, much like the rest of the world:

Today, China has a lot of unsold housing inventory:

On top of that unsold inventory, China has another 90mm of empty property:

China seems to recognize this has become a problem. In addition to all the usual consequences of a property bubble, China has the additional issue that their 1-child policy means a smaller population in about 10 years. I think the government realizes they have to deal with this now before it gets even more out of hand in 10 years.

China is unquestionably squeezing developers to try to reduce the investment made in new properties. China drafted rules in the summer of 2020 – so not that long ago – that constrained how much leverage developer could take on.

They called this 3 red lines. It limited borrowing to developers/financials based on ceilings they apply to 3 metrics: debt to cash, debt to equity and debt to assets.

One detail of this that I got from a Youtube video is that China gave developers 3 years to comply with these limits. The Youtuber pointed out this implied that many developers were likely far over these limits right now.

Not surprisingly Evergrande stock began to slip at around that same time. And financing to developers has gone negative the last 12 months.

But developers and Evergrande aren’t the headliner here. They are like the cog in the gear system that is stuck. The engine seems to come from the regional and local governments (more on that in a second) and that could be a problem. It has to do with the end-source of the financing new infrastructure development in China.

So…. there are these sources of capital for Chinese local and regional governments called local government financing vehicles (LGFVs).

LGFVs are an off-balance sheet way for local governments in China to raise money. The money they raise is mostly used to fund infrastructure (ie. what you need for property development). FT calls them the “main lenders behind China’s infrastructure building boom”.

Why do local and regional governments use these “vehicles”? To get around the limits put to local government borrowing. They are “off-balance sheet” so they mean a government can lend without looking like its lending.

Way back in 2019, so before Evergrande was on anybody’s radar, China “hit the brakes” on LGFVs, saying they could only refinance existing debt in the second half of the year.

But then Covid hit and the brakes came off.

Now the brakes are on again. And not surprisingly, Evergrande and other developers that depend on development (and thus LGFVs) are back on a downward path.

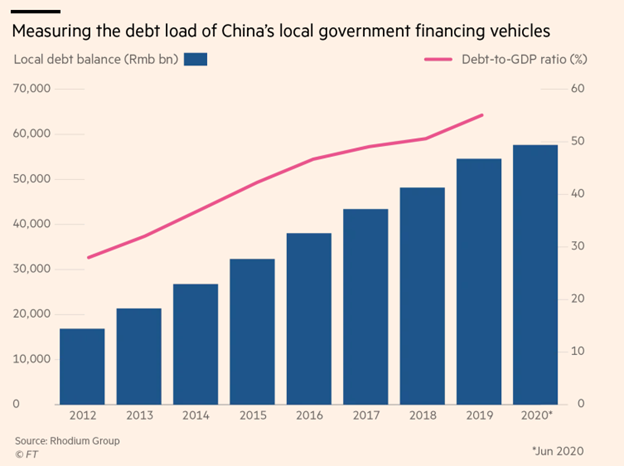

So LGFVs fund infrastructure and infrastructure is a big part of China’s economy. 43% of GDP was fixed asset investment last year.

Here’s the thing about the LGFVs. They have a shitload of debt. And I mean a shitload. Here is where Hendry almost assuredly got his number from:

$60t Renminbi of debt is over $8t USD. That is real money.

And here is, IMO, the big reveal:

Hmmm – that sounds an awful lot like the “house prices don’t have to go down, they just have to stop going up so fast” argument of the Great Financial Crisis.

So there is all this debt outstanding at the local and regional levels. It is kept afloat by land sales. But land sales are collapsing because the big developers like Evergrande have been squeezed and are in trouble.

I don’t know… I’m not smart enough to say how this plays out. But I am cautious enough to think there is somthing more tectonic at play than a property developer going bust.

First of all, my primary reason for writing this post is that I really like the title. I was thinking about Evergrande last week and it just popped into my head and so now I have to write something to go along with it.

I wanted to get this out on the weekend but I didn’t really know how to say it. Then Monday happened and I didn’t want to say something bearish with the market down so much. But now we have had a nice turnaround-Tuesday and my thoughts have stewed enough to percolate so it seems like as good of a time as any.

The story behind the title is that I always sell first and ask questions later. I’ve written about it before. This time I am writing about how most of the time I am wrong to do so.

This was not always my instinct. When I was a novice investor I had a conditioning that I think all human beings have – the want to hold on to hope.

Unfortunately, when you are investing, and in particular when you are investing in small cap shitcos for the most part, hope is more your enemy then your friend.

My experience is that if you hold on to hope you will be more often than not disappointed. The reality is that 9 times out of 10 (that is not a scientific estimate) you can buy back at roughly the same price anyway a few weeks later.

So whenever I smell even the hint of a crisis I go into defense mode.

As the title suggests, usually this is wrong. The crisis blows over as nothing.

But every once in a while, it becomes a full-blow 10%+ correction. Which can be a 20%+ correction for the crappy little stocks I own.

But more importantly – every once in a blue moon, it becomes a real bear market.

When I am wrong, I miss out on the fire sale selloff and usually the first few days of market recovery.

That is too bad. But when I am right, particularly when it is that blue moon event, it more than makes up for it.

Consider my posts from back in February 2020 (including my comments at the time). Just think – in February 2020 I did not really know if this ensuing “pandemic” was going to amount to anything!!! I was selling and shorting and at the same time cautiously admitting I might be horribly wrong for stepping aside and if the market took off I was “okay with that”.

LOL!

I didn’t have a freaking clue what was about to hit the market. In fact even though everyone says otherwise now, I doubt that more than a few did. Those that suspected were more like I was – feeling uncomfortable but not all that sure how things would play out.

But because I followed my rules and “sold the crises” – which meant buying inverse ETFs, selling some shorts where I think they might be particularly vulnerable to the crisis flavor of the day, and buying a little bit of VIX for leverage – I can happily recollect that my portfolio was up 3% on the year when the market hit its low of 2,100 and change – even as my remaining small cap positions were obliterated.

Now of course that first move up from 2,100 to 2,500 was not something I participated in. C’est la vie. I lost no sleep from my portfolio through a horrible time for everyone and that is worth way more than a few points of performance.

So is Evergrande the next Lehmans? Eh. Probably not. But it could be the next 10% correction if the cards fall right. There is a lot of debt off the balance sheet, there is apparently some $500 billion in new build buybacks that they are on the hook for, and there are some strange ties to private equity and even to tether which just seem odd.

And there is also another one of my axioms, which is that no one really knows what the F&*$ is going on in China.

Last week I started to take precautions. I peeled back some risk in stocks I have less conviction in, added a couple short China ETFs (just the 1x CHAD and YXI), and added a little VXX.

I’m still far from “short” the market, but it was enough that during yesterday’s bloodbath I was pretty much flat on the day, which is basically my goal during periods of turbulence.

If the market takes off from here, the playbook says that I will underperform for 5 or so days. I will pull my hair out during that time as I see indexes rise, the VIX fall, but all the stupid little microcaps I own do nothing. Oh well, I am getting used to that, it is just the circle of life.

It is imperative, maybe as much because of my own particular psychology as anything, that I prepare for the worst each time, even as I know it is a poor-odds bet.