Research: Callinex Mines

- only 11mm shares outstanding, $33mm market cap

- targeting zinc rich deposits

- these guys were founded out of Callinan mines, which discovered 777 mine

- targeting VMS deposits

- two mining districts Bathhurst and Flin Flon, also have a property in NFLD – Bichans district

- Even though I talk Bathhurst first, its the Flin Flon property that is the interesting one:

Bathhurst – New Brunswick

- 3 properties: Nash, Headway, Superjack

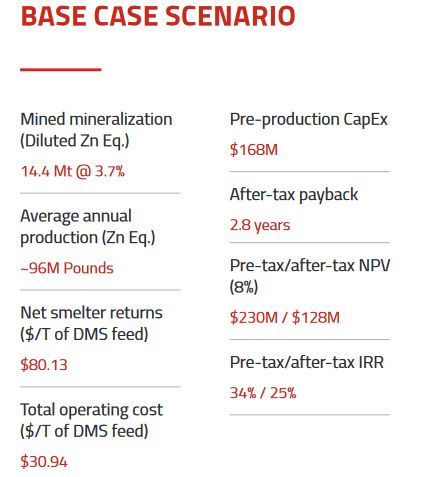

- they have a PEA at Nash Creek

- 10 year 3,900 tpd open pit mine

- 963 million lbs of Zn Eq

- would use existing Brunswick smelter

- it wasn’t a huge mine, but not terrible either:

- unfortunately it looks like it is a Zn/Pb deposit which isn’t super exciting

- from what I can tell zinc is going to be in surplus for a while

- but latest results seem to be finding silver

- NC 20-313 intersected 28.6m of 57 g/t silver at a vertical depth of 120m including 16.5m of 94 g/t silver and NC19-306 which intersected 19m of 36.53 g/t silver, 0.52% lead and 0.38% zinc at a starting depth of 34m

- the silver could be on to something but who knows

- overall I’d give this project an – “ehh”

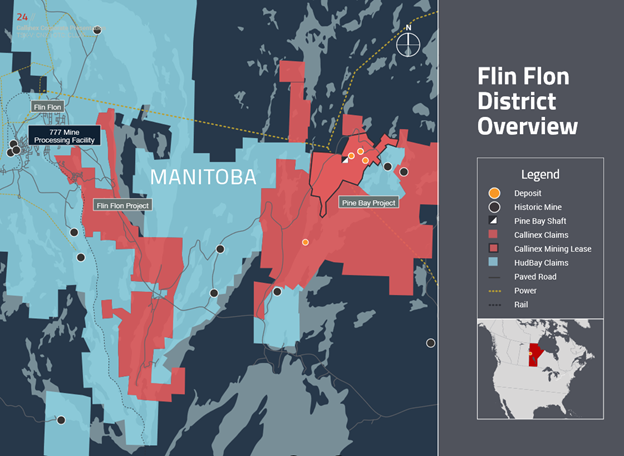

Flin Flon

- right around historic mines

- Callinex claims are right around the Hudbay 777 mine – they are maybe 10km to the east of Flin Flon

- just like generally, it is kinda crazy that a $30mm company has this much land leased right around Flin Flon:

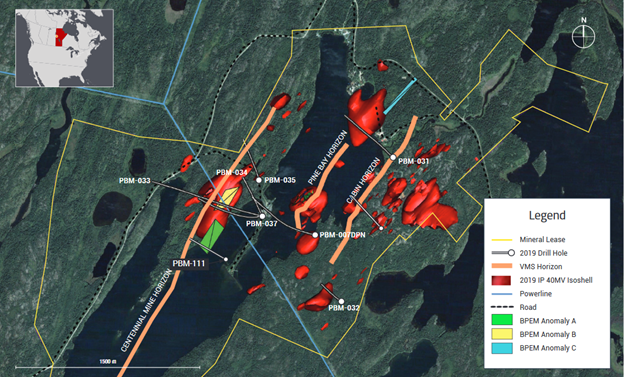

- they call recent discovery Rainbow – it is at Pine Bay project (to the east)

- targeting 3 anomolies they’ve found:

- within a larger VMS corridor with a number of other mines

- in Sept announced some high-grade but narrow intercepts:

- PBM-111 – 3.09% copper, 0.75 g/t gold, 13.35 g/t silver, 1.88% zinc over 2.96m

- and: 4.12% copper, 0.22 g/t gold, 2.21 g/t silver, 0.06% zinc over 4.31m

- So that doesn’t look that interesting, pretty narrow, who cares right?

- but this is interesting:

- the geology suggests something much bigger – they cut across a 260m by 600m anomoly

- this walk-through of the Rainbow discovery is pretty interesting, look at the anomaly and where the drill intercepts went: https://vrify.com/embed/decks/9497

- It really looks like they sliced across something that potentially could be very big

- new release Tuesday that they have drilled two more holes 112 and 113 and they both have hit on something – going to lab and will know more with results then

- 113 is right into the anomoly, 112 is above anomoly but into massive sulphide core

- We should have results on these two holes in the next couple of weeks

- So basically, they are in elephant country, they just sliced across something that looks like an elephant

- One more thing, after they released the news that they sliced across something that looks like an elephant, the CEO went and bought a bunch more shares at a 52 week high:

I don’t talk exploration stories much on the blog because I usually get them from newsletters and so they aren’t my original ideas. But this one I found from the insider buys and it seems interesting enough to take a position. But these next two holes could miss and the stock could tank, so high risk. The drilling so far caught my attention and just the idea that this dinky little venture company has such a big land package right around Flin Flon and surrounded by Hudbay claims.