Evolent Update

It is not a lot of fun writing updates when things aren’t going well. So, let’s get this over with.

There have been 3 unforeseen events that have befallen my portfolio in the last month. Hopefully the old saying holds true.

In all honesty I don’t know if I’ve had a string of luck like this before. I’ve had lots of bad calls of course, it just goes with the territory, but to have 3 event driven moves, all of which your could argue were on the low side of probabilities, in such a short time, well I think that is a new one for me.

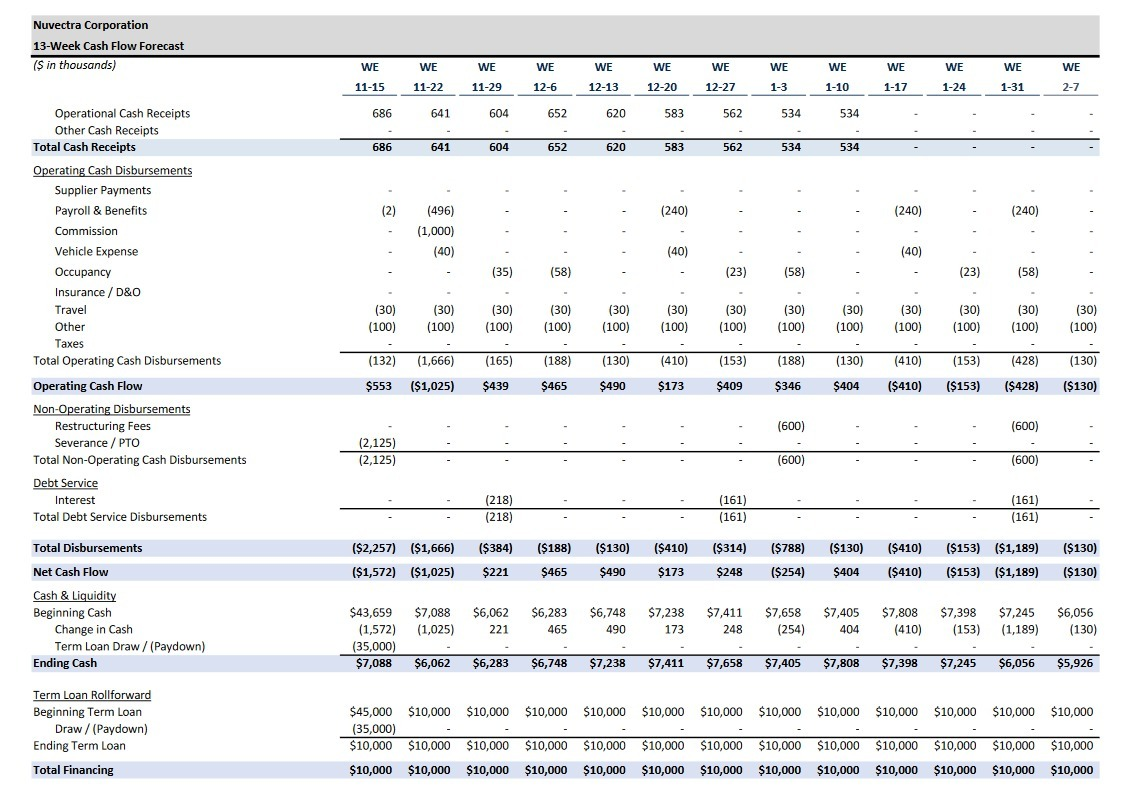

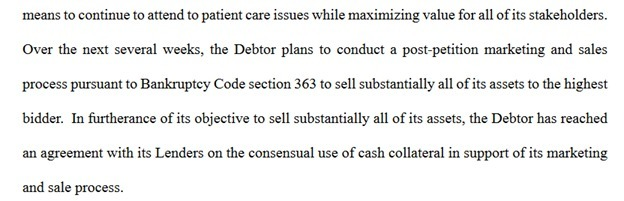

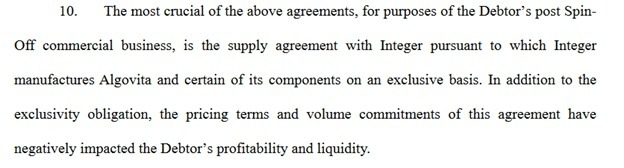

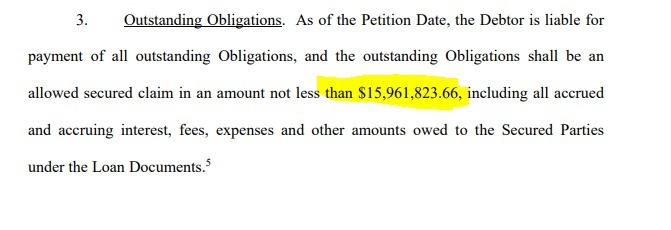

The first event, which I have already talked about at length, is the Nuvectra bankruptcy. I won’t discuss this one much except to say that of the three events, this was easily the most predictable.

I knew there was a chance that Nuvectra wouldn’t make it. They were losing lots of money and they needed a buyer. I thought that the probabilities were in my favor that they would find a buyer given all I had read about the products and potential, but it wasn’t really all that unlikely that they wouldn’t.

The other two events were less likely. The Evolent Passport renewal and the Mission Ready TLS inclusion.

I’ll leave the Mission Ready discussion for another time. Suffice to say that at least for now, I do not see a positive way to look at this. Sometimes you just have to admit defeat and move on.

Evolent, on the other hand, is more nuanced. Like Nuvectra, the negative event can be construed as an opportunity, albeit a risky one.

What happened was straightforward enough: Evolent’s subsidiary Passport Health Plan didn’t get renewed by the state of Kentucky as a Medicaid provider for the upcoming 5-year term.

Based on all the work I had done, heading into the renewal this seemed like a pretty unlikely event. Passport had been a provider for 20+ years. They had a reasonably good track-record with patients. They weren’t even ranked at the bottom of the 5 existing providers (Humana was, and fwiw they were renewed, while Anthem, I better ranked plan, was not).

What’s more, since Evolent took Passport over, their financial performance had done a 180. Passport had gone from loss-making to profit making. Their operating margins had met Evolent’s 1-2% target as of the fourth quarter.

To think that the state of Kentucky would disrupt their Medicaid citizens by pulling the plug on Passport seemed unlikely.

Yet that is what happened.

Of course, we don’t know the reasons, but I really suspect that politics are in play here. I also think this is the unusual case where there is a good probability that the ruling is overturned.

Consider the following

- The administration that made the decision (the Bevins administration) had an ongoing beef with Passport

- Passport actually sued the Bevins administration earlier this year before Evolent got involved

- The Bevins administration lost the election and is out of power on December 10th, which means they made this decision with 11 days left in their term

Now consider these comments from members of the incoming Beshear administration and other Kentucky politicians.

From this article:

“I am very hopeful that as soon as he (Beshear) takes office, he will look into this situation and try to adjust accordingly to affect the lives of the citizens of Jefferson County, because this is really a slap in the face to the citizens of Jefferson County,” said Metro Council President David James.

“Awarding $8 billion in contracts with just 11 days left in this administration is concerning,” wrote J. Michael Brown, incoming executive cabinet secretary and chair of the Beshear transition team. “As we move through the transition and ultimately the change of the administration, we will be taking a close look at this action.”

From this article:

Louisville Metro Council President David James said in a statement that Passport’s 20 years of providing health care to “people who would not otherwise be able to afford health care” is necessary for the community.

“Now at the beginning of the holiday season, Gov. Bevin has decided to take away this security for those members of Passport not only for themselves but their families,” James said. “It is a cold, callous decision done purely for political reasons.”

From this article, comments from Republican Jason Nemes, which gives a bi-partisan flavor to the pro-Passport side:

“While I have great respect for the current administration … it concerns me that 8 billion dollars in contracts were awarded in the last days of the current administration,” Nemes wrote.

“Of more concern to me is that two incumbents with a proven track record in Kentucky were ousted. Passport, in particular, has been serving the Commonwealth for 22 years. Passport supports many community agencies that help people in need and many of these individuals improve their health outcomes and quality of life because of that.”

From this article:

Beshear, who takes office on Dec. 10, said it would be “premature” to discuss his administration’s options to address the Passport situation, citing the legal formalities involved with awarding state contracts.

“There’s a lot of rules and regulations that will be in play, but my commitment is to do the right thing once we have all the information,” Beshear said in an interview with WDRB’s Lawrence Smith.

The incoming governor added that it was “concerning” that the Bevin administration decided to award “$8 billion in contracts with 11 days to go” in office.

Beshear also said he is “committed” to getting Passport’s stalled construction project for a headquarters building in west Louisville back on track, “whether it is through this project or another.”

“That building symbolizes so much hope, but we can’t let it become false hope,” Beshear said. “… It is time to bring real jobs and real economic progress to west Louisville.”

What is particularly interesting about the last quote is that Beshear won’t say what he is going to do with Passport because of “legal formalities” but he’s committed to getting Passport’s headquarters built?

There is a lot I don’t know here but I’ll tell you one thing I know for sure – if Passport doesn’t get renewed that headquarters doesn’t get built – because Passport isn’t going to exist.

What’s more, Evolent reiterated on their post-announcement conference call that if Passport doesn’t get renewed, the wind down that would occur in the second half of the year would return cash to Evolent that would pay off their investment. So, its not a total disaster for the company.

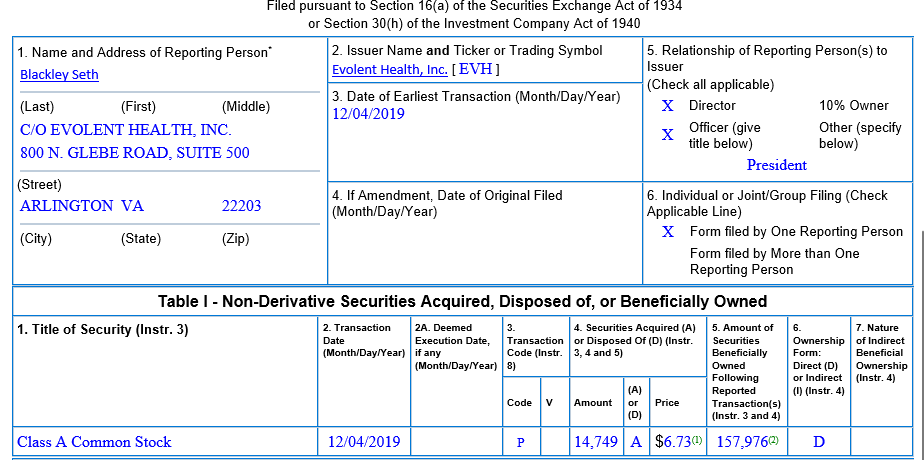

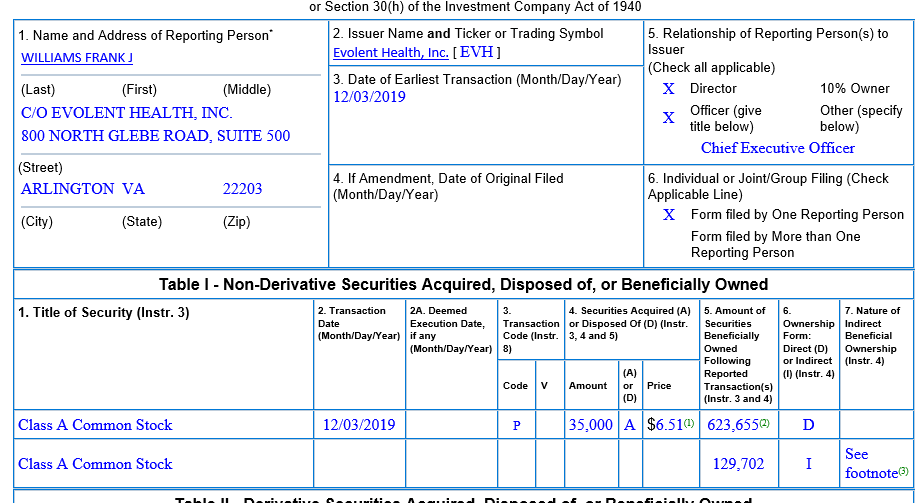

The last data point is this. On Thursday there were two insider buys. The first by Frank Williams, the CEO, and the second by Seth Blackley, the President.

These aren’t token insider purchases. they were six-figure buys – $225,000 in the case of Robinson. They show confidence by the management team and, maybe more importantly, they imply that the company won’t be raising cheap equity to pay for Passport, which is something a few analysts have worried about.

The Evolent story is even more complicated now then when I first bought the stock. But apart from the Passport debacle, the company has been moving in the right direction.

This is on of those cases where my gut reaction was to sell the stock on the Passport news, which I did. But after understanding the details I described above, I decided to buy it back and then some.

Note: I wrote this on the weekend and last night this came out, which further cements my expectations.