Week 278: Shorter Posts and thoughts on Credentials

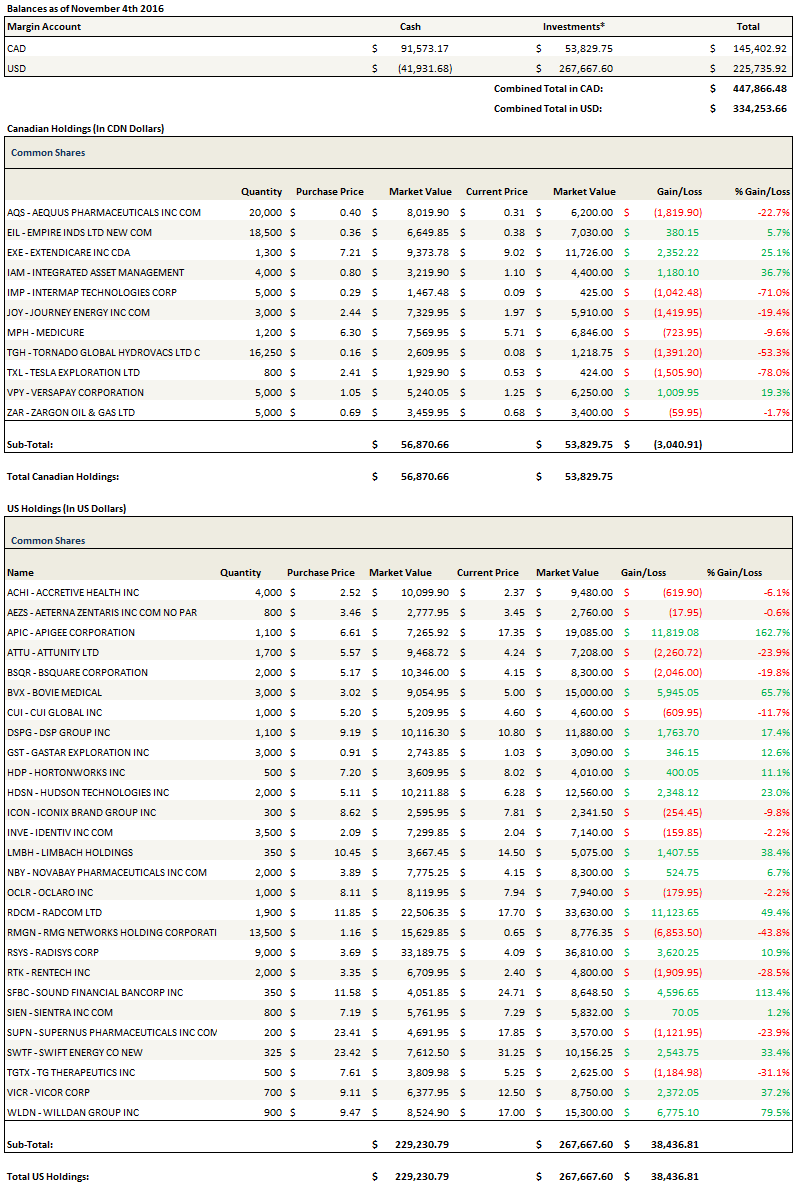

Portfolio Performance

Top 10 Holdings

See the end of the post for my full portfolio breakdown and the last four weeks of trades.

Thoughts and Review

I had such a good response from my post on Radisys that I decided to change things up for the blog. Rather than posting monthly letters summing up all my thoughts, I am going to deliver updates in a more traditional blog format. I will write as things come up. So this update will be more brief, and will not cover any lengthy company updates.

I had a pullback in the last month. I guess it shouldn’t be unexpected. The previous three months were almost parabolic. Having a portfolio that is weighted only to a few stocks, any kind of lull in the performance of those stocks can cause big fluctuations. Right now my portfolio is heavily dependent on the performance of Radcom and Radisys. Both stocks had corrections leading into and following their third quarter earnings.

The good news is that nothing has occurred with either to warrant a change in mind. While I expressed some concerns about Radcom in my earlier post, I felt a lot better about the stock after their Needham conference presentation. I even bought some back over the last couple days.

I sold out of a number of oil stocks. I still hold positions in Swift Energy, Journey Energy, Zargon Oil and Gas and a very tiny position in Gastar Exploration. Other than Swift Energy, none of my positions are very big. I started by selling Granite Oil after these comments on InvestorsVillage (here and here). Looks like I was wrong there. Later, as the price of oil began to break down I sold Jones Energy and Resolute Energy. Both of these are levered plays and I expect out-sized moves as oil corrects.

I added a couple of new starter positions under the theme of Big Data: Attunity and Hortonworks. The latter has begun to work out but the former has not at all. I’m doing some more work to understand if I just made a mistake on Attunity. With the new blog format I will write-up the positions and my thoughts on the Hadoop market (which led to my investments) in separate posts.

I also added a position in Nimble Storage. The company has some good technology, can compete with Pure Storage and take market share away from incumbents like NetApp. Again I’ll give more details in a later post.

Finally I mentioned in my last post that I had taken a very small position in Supernus Pharmaceuticals. I’ve held that position over the last month and watched the stock correct downwards almost every day. This is a big biotech sell-off and I don’t think the move has much to do with the company itself. Supernus is growing very fast, there appears to be plenty of opportunity for further growth, and the pipeline of new drugs seems to be quite robust. I’m seriously considering adding a big chunk to this one.

Credentials

One final thought on the topic of credentials. As I have written in the past, I manage my own family’s money. Recently I had an opportunity to expand that to a number of friends. But before going too far down that path I wanted to understand the regulatory requirements.

It turns out that in Canada at least, managing money and taking any sort of payment for it is very regulated. It requires a number of courses, which is reasonable, but also years of very specific experience under the tutorage of a dealer.

Clearly I am not going to take 3 or 4 years to work as an understudy just so I can start a small part-time business on the side for a few friends.

My frustration is that there is no distinction between someone trying to scale into a large fund, soliciting money from the general investing populace, and someone who wants to do what I was looking into; basically help out some buddies and get paid on performance to do it. These two activities do not seem equivalent in terms of public risk. But in the eyes of the regulator there is no distinction.

I’m not a conservative in most ways but this certainly gives me sympathy to the position that abhors regulation. I’m in a region that is suffering, I have a ready-made opportunity to create a small business, and the government has basically said no you can’t do that, because we know best. Because as anyone who has read this blog for the past 6 years knows, I am clearly not qualified to pick stocks.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}