I came up with this title because my daughter is sick and I’ve spent the morning reading her a Dear Canada book about the Second World War. Reminds you things could be much worse!

Right now, things could be much worse. In fact, my problem is that things are not quite bad enough but they aren’t near good enough either.

I’m really torn about what I should be doing right now. While I can see that things are bad I can also see how they are not so bad, or that they could quite easily get better. But before they do they might get suddenly worse.

I went into the weekend a little more long than I usually am. This was mostly because I had taken a few positions in the large money center banks, Bank of America and Citigroup.

Why did I buy these banks? Well it was partly what I wrote about last week, about how they should have some good earnings with increased net interest margin and maybe even be able to take share from the regional banks struggling with their security portfolios.

But it was also partly because I had spent a bunch of time reading through transcripts of bank executives at the recent Barclays and Bank of America banking conferences.

I read through what the big banks said, so BAC, C, JPM, etc. And I read through what a number of regional banks like Regions, First Third, Comerica, MTB and a few others had to say. Most of these banks, in fact almost all, were really quite positive. They aren’t seeing the slowdown yet. They aren’t seeing consumers pull back much. They aren’t seeing reduced loan demand (other than in obvious places like finance) and aren’t seeing increased distressed credits.

This put the idea in my head that maybe the slowdown in Europe and China might be enough to slow inflation and put the Fed at ease, without having to slow the economy too much in the US.

So it made sense to take a position in a few banks.

That still makes sense to me. But over a longer time horizon, one measured in months.

For today, I sold the bank stocks I bought a few days ago. It was very frustrating because A. I had to take a small loss and B. I really feel like the market should be close to a bottom soon.

But I still did it. What spooked me are the moves in a number of currencies that happened Sunday night and Monday morning. The pound. The yen. The Canadian dollar.

It is not that these moves give me something specific to worry about. I am not really sure what I should be worrying about. And that is kind of the point. I don’t know what is going on that would cause such huge moves in big currencies that typically don’t move much at all.

All I know is that when the moves are big in big, liquid markets I have to wait it out just in case. This is especially the case with banks, where risk-off situations can manifest themselves pretty fast.

I am aware I might regret it. The other side of it is that big moves like we are seeing usually mean a turn is near.

But usually those turns come because of a pivot or perceived pivot by central banks. And this time, I’m not so sure how that will manifest.

For 14 years it has been a fools game to assume that each panic does not mark a bottom for the next move up. Today was the first day it felt a little panicky. Every other time it started to feel like this, the bottom was close at hand and so today not a time to sell.

But without the Fed or ECB or whatever other central bank ready to backtrack, could this be the time that doesn’t happen?

I just don’t know. Like I said I’m torn. Because part of me thinks we are really, really close to a bottom and there are big bargains out there in stocks. And the other part of me thinks this time conditions are such that it could actually be different.

That puts me square in no mans land. One where I can’t own the banks I really want to own. And also one where I probably miss the turn and kick myself a month or two from now because the market moved and my portfolio did not.

I haven’t written for a while. Summer is a hard time to find time.

This summer, that was compounded by a lack of things to write about. We rallied, the rally failed, we rallied, the rally failed again. I bought a couple stocks. I sold a couple stocks. I held nothing with a particular conviction that would compel me to write about it. My portfolio did nothing, which means, as it importantly implies, it did not go down.

The last time I wrote (mid-July) I was talking about going back to my default position. Putting back on hedges, putting back on shorts and trying to squeak out a few gains while not taking any big chances. That is pretty much what I did and pretty much where I am now.

While I remain nominally net long I am, in terms of my portfolio’s response to market moves, a little net short. Witness that on big up days during the summer I lost money (this is also due to my “natural short” of being long US stocks with a Canadian dollar account, otherwise known as my “edge”). On down days, I made a bit. Overall I am very slightly better off than where I started the summer.

The reason my portfolio acts as if it is net short is because I don’t own much in the way of small cap stocks. Yet the stocks I am short are the somewhat shitty one’s that tend to go down a lot when the market goes down (though vice versa as well).

The moves in the portfolio overall are small and the exposures are as well. That’s okay. The time will come again to take a large line. That time does not feel quite here. While many portfolios are down big double digit percentages from highs set in 2021, I am not and that is good enough for me.

I do feel like change is coming. This bear market is getting long in the tooth. Yes, there are plenty of things to worry about, but there are always plenty of things to worry about.

My approach this time around may be different. I am not looking to place bets on small-cap shooting stars.

Quite the opposite. My portfolio today (which I know I haven’t updated in a while, I will do that in the next couple days) is full of very large businesses and, for the most part, somewhat boring businesses.

My largest positions today are in stocks like Vertex Pharmaceuticals, Dole Foods, Hewlett Packard Enterprise, Verizon Communications, Meta Platforms and Alphabet.

Why the shift? Right now many very large companies trade at valuations that seem pretty reasonable to me.

In addition to these large cap names, I’ve bought some bank stocks. This is maybe crazy if we are indeed on the cusp of a recession. But I’m also short the Canadian banks, and short some other parts of the market that I believe will go down more, so I’m trying to cover my downside here.

My reasoning on a bank stock long is that if this recession is not deep, the banks have a lot going for them. What I heard on the Q2 earnings calls were banks talking excitedly (for a bank that is) about their net interest margin expansion. They were passing the floors on their variable rate loans, meaning they could hike rates on loans in concert with Fed hikes, and yet the deposit betas (meaning how much they had to raise deposit rates for their customers) was coming in muted.

Banks remain very cheap on trailing earnings that don’t reflect this expanding margin. The banks I am buying are generally below 10x PE.

But you have to be careful about what you buy right now. While the rise in interest rates has been good for income, there are some banks that have seen their book value slashed by paper losses on the securities they hold.

I am seeing some banks taking huge mark-to-market losses on treasuries and mortgage backed securities. These securities are going down as rates go up.

I’m not really sure what to make of these losses, because they are just paper losses, but they are also real in so far as they impact the banks tangible book calculation and therefore the capital ratios. Which means they will also impact the banks ability to grow.

These losses, which are called “other comprehensive income” (OCI) losses, don’t show up on the income statement. They feed through on that next page, called “Comprehensive Income”. I have noticed that most of the banks with the biggest OCI hits have kind of glossed over it like it doesn’t exist.

But they do exist and OCI losses are very big for some banks. Take Keycorp for example. I bought them and owned them for a few days until I figured out what was going on with their comprehensive income. Once I did I sold. Because Keycorp took an OCI hit of 37% of their tangible book in the first half of the year. That’s huge! They aren’t the only one – Fifth Third Bancorp, another bank I was looking seriously at until I ran into this OCI issue with them, took a hit of 31% of TBV.

Again, I don’t know what to make of these OCI hits. Do they matter? I’m not sure. They certainly make the bank look more expensive on a book value basis. Post the OCI hit, the bank is closer to running into regulatory trouble if something goes wrong with its loan book. OCI hits don’t impact earnings, though as I said they might impact the ability to grow earnings in the future.

Just to be safe, I’ve stayed away from banks with big securities portfolios that are taking big OCI hits. Funnily, its either the very small banks or very large banks that aren’t having to do that. The small banks don’t own a lot of securities. the largest one’s (like C, BAC or JPM) seem to be better at hedging their exposure.

The other big question is whether the banks will get creamed on loan losses brought on by a recession. A lot of that will depend on how bad the recession is. It will also depend on the nuances of each bank – where they made the loans, who they made them to, and what are the loan-to-values. So again, you just have to be careful.

The thing is, banks went through a pretty strict rationalization of their loan book with Covid. We are barely two years past that. It is not like there are years of excess baked in.

While I could get smacked on real credit driven downturn (I mean if credit goes south no bank is immune), if this is a mild-ish recession, I think bank stocks are going to do okay and maybe even well.

I have also done something that I never thought possible. I made the move into a few SaaS and tech names. I own Datadog, Monday.com and Zoom. Pigs fly.

These stocks aren’t really “cheap”. But they are a lot cheaper than they have ever been since I’ve followed them. Take Datadog. I have followed it for a few years now. I make this little discounted cash flow model for it that I update every quarter or two. The details of that model aren’t super important, but what is important is that I always use the same assumptions.

Using the same assumptions means that I can track how Datadog is valued against my own crude valuation over time and get a sense of when it seems quite reasonable.

At $90 Datadog trades at a 20% discount to this fair value. It hasn’t traded at that level before (other than in June when it was $90). I read through the Q2 call, I read through their talk at the Goldman conference. The business still is what it is.

The thing about Datadog is that yes, its growing very fast, but it is also a free cash generating business. Their FCF margin was 18% in 2021. It probably goes about 20% this year. They are doing this while growing 60-70%. Yeah it looks expensive on a PE. But on a DCF basis with even conservative assumptions, it doesn’t.

So that’s Datadog. You can kind of make similar comments about Monday.com, though they are maybe 2 years earlier on in the process and the free cash flow barrier hasn’t been cracked just yet.

Zoom is a different beast. They aren’t growing right now. They grew too much during Covid and now they have stopped. The stock is being whacked because they aren’t growing and because Teams is free.

That’s fine and it seems well-founded. My thoughts with Zoom are that A. It is hated and yet seems to be bottoming, B. It is not all that expensive at 11x EBITDA and a 5% FCF yield, C. It may start growing again some day and most importantly D. Zoom is on everybody’s desktop, everyone’s smartphone and I don’t think the value of that is priced into the stock.

But Zoom gives me the most pause. They could pull out an awful Q3 and I get stopped out of the stock.

You have to remember that my style is not to do a conviction-building deep dive into Zoom (or any other name) that most likely turns out to be wrong anyway and just keeps me from selling the stock when I should be. It works better for me to come up with a cautious, heavily caveat-ed, thesis, that has some merit and if the stock acts right I’ll assume I might be onto something.

I sold my oil stocks. I sold a lot of the gold stocks. I only own a small position in Newmont and Alamos Gold. I have been buying a couple copper stocks – Hudbay Mining and Taseko. These miners have been whacked pretty bad, they discount $3.50 copper at the current price and the longer term outlook for copper looks quite good to me. I’ve read a number of analyst reports that make the case that we don’t have enough copper for the renewables transition and that we will (eventually) need higher copper prices to get those projects built.

I also have sold almost all my biotechs. I moved up the food chain with the purchase of Vertex. Though I still own Eiger. I did sell a some of my Eiger in my less risk tolerant accounts (RRSPs) but I kept it in my own account, where I was okay having a bit more risk and also able to have more hedges via shorts (like an XBI short for example).

Eiger as a Covid play seems less likely to pan out than a few months ago. But Eiger’s stock has been surprisingly strong. The HDV results will be coming up in a month or two, which will make or break the stock. CEO David Cory also hinted at the Baird conference that they might have other countries interested.

So that is the kind of catch-up, catch-all summary. I’ll try to write something more specific about a name or two in the next few weeks.

I did not make very many changes to my portfolio last week. Yet it felt like a busy week because I did so much thinking about it.

It was a good week for thinking. Our family finally succumbed to COVID. My daughters had it during the week. My wife has it this weekend. I think I had it last week as well, I was ridiculously tired and headache-y, had weird neck and shoulder stiffness, had a worrisome (at the time) tingly feeling down my arms for a couple days, but I never tested positive, never had fever, never had a runny nose. So I don’t know.

Market-wise, there are so many things going on right now in so many directions. It is really tricky.

Let’s start with what we know. Biotech is going up. Finally. The question I am starting to ask is when do I sell some of these names? I think its a real balancing act.

On the one hand, I need to reduce my positions and take at least some profits. I have to, regardless of what my suspicions are about where we are going (I kinda think biotech goes higher). But I have to because I just don’t know. No one knows. Biotechs could flip and go back down for any number of reasons.

But at the same time, I did not go through that miserable biotech winter just to sell out for a 20% gain. Many of these stocks are up a lot from the lows. But they are still a double away from where they began the year and in many cases a triple or more away from the high. Its the same business. Just a different market. And markets change.

So like I said, its a balance. I have to trim in places. Sell down a little when a stock really takes off. But I can’t bring myself to a wholesale liquidation, even though the gains this last week have been significant.

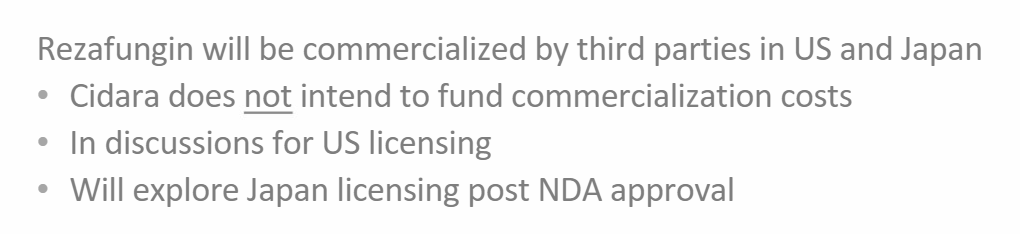

I did add one new biotech position this week. Cidara Therapeutics. Its a decent story with a story in a story so here it goes.

Cidara’s lead program is Rezafungin, which is an anti-fungal that treats Candidemia and invasive Candiasis.

These are usually hospital acquired infections. The patients get very sick and many of them die. There is an existing treatment, but its old and, with a mortality of 35%, it doesn’t work that well.

Rezafungin finished a Phase 3 trial with results published in December. They were good results. Good enough to file an NDA (new drug application) with the FDA, which they expect to happen shortly.

I don’t really remember who told me about Cidara. It was back in December and I do remember it was someone telling it to me via a Twitter DM. But that DM isn’t there any more so whoever it was must have left Twitter.

Anyway, at the time I passed because Cidara didn’t have a lot of cash, they weren’t a negative enterprise value (I was all about having more cash than market cap back then if you remember) and I didn’t really know how they were going to get the money to commercialize Rezafungin, which seemed like a hurdle.

Flash forward to last week and I saw they did a Research and Development day. I went through their presentation, not really thinking much of it, when I saw this slide:

And that is like, Oh, well that’s interesting.

One thing I didn’t mention is that Rezafungin is already partnered for ROW ex-US and Japan. They had a partnership with a firm called mundipharma, which is where they got the cash to get this far:

So now Cidara is thinking that they will partner the rest of it. I listened to the Research Day call and they said they have had a lot of incoming interest in a partnership since the Ph3 results. Interesting. They say they think they will have something in place by the time they file the NDA. Interesting. They also say they will be filing the NDA shortly. Interesting.

But nothing here is a sure thing. I could get totally screwed on this by some sort of crummy financing that comes with the partnership. In fact, this is just what happened to me with another stock – Precision Biosciences – a few weeks ago.

Let me digress this story into another story that illustrates the caveat.

So I hold this other little biotech, Precision Biosciences. It’s kind of a crappy company. They do something like CRISPR but its probably not as good, the clinical results are promising but at the same time not promising, they do the same CAR-T stuff Caribou does and have the same problem with durability. And up until very recently the stock has been a complete disaster.

The stock was down at like a buck-20 a few weeks ago. It was finally trading less than cash. I was tempted, but I also didn’t know how they were going to make it as a going concern given the cash burn and the low cash levels. It seemed like they just might go bankrupt.

So I was like, oh, that’s interesting. And I bought DTIL.

About 8 days later DTIL announces a partnership with Novartis. For sickle cell, because every gene editing company needs a sickle cell program. But whatevs, its cash, $75 million, and that will keep them afloat and put another program in their pocket and all those shorts betting the company is going to go bankrupt are going to have to cover.

The market realizes this and the stock SOARS in after hours. I mean SOARS! It goes from $1.30 to $3. I’m rich! (well, not really because I don’t own that much, but nevertheless, its a win).

But then, BUT THEN – half an hour later – half an hour – they announce a bought deal financing. AT $1.39!!!!!

What a mess. The stock comes right back down. It trades at $1.50-ish the next day, a far cry from $3. I still hold my shares and they are doing pretty well because of the biotech resurgence, but still, it was a total gong-show.

So back to Cidara. Its kinda the same situation. You have a cash strapped company that just hinted they may come up with a deal that gives them some cash. If they get that cash, the market will flip from ‘this company ain’t going to make it’ to ‘this company can live to fight another day’.

But like DTIL, Cidara also could decide to completely screw over their shareholders in the process.

Neverthless I took a small position in Cidara on Friday. Small because of all of the above reasons and also small because I don’t really understand the molecules they are pivoting too. Its something called their Cloudbreak platform, they are going after oncology, its a big switch. I need to dig into that to make sure there is actually something there.

So that’s biotech. Oh, and Eiger had news of sort. Something is happening. We don’t know what. But at least we have a date to work with.

Onto SaaS. I did lighten up a bit on the SaaS stocks I bought (OKTA, AYX, DDOG, CRWD and ZM, which I added more recently). They have had a nice move but I’m not sure how long it will last. They have a few headwinds.

First, interest rates aren’t exactly heading straight down and in many ways these stocks are little, micro interest rate bets. Rates go down, future earnings go up and the stocks with them.

I don’t know what to make of rates. On the one hand I get that a lot of this inflation should be transitory and the market is probably finally caring about it just at the time it should stop caring about it.

On the other hand, I’m not sure. And when I’m not sure, I don’t have to be long the stocks that express that idea.

Second, I can’t help but shake the feeling that this is a little like telecom in 2000. Back then, there were all these telecom companies that were booming and then all of a sudden they weren’t booming. It stopped on a dime largely because they were all booming on the backs of one another. Everybody was buying from everyone else.

I have a feeling some of that has been going on with SaaS. And I really wonder if some of this “secular growth” is going to turn out to be less secular then we thought because of it. So I don’t want to be too long and I may sell the rest this week before earnings start to hit.

Finally oil and gas. I spent the first couple days last week frustrated that my oil stocks kept going down. So I kept buying them. Then I spent the last two days of the week selling what I bought as they came right back up again.

I made the case for owning some oil stocks in my last post. I tweeted that I thought it was getting a little silly on Wednesday.

Crescent Point had a nice pop the next day after they increased their dividend. So that’s great. But, I don’t want to be too long oil stocks here.

There is still this whole recession thing that seems quite plausible. And then there is Biden’s visit to Saudi Arabia. A good point was made on one of the Gulf Intelligence podcasts last week. I can’t remember which guest, but they pointed out that Biden would only be going to Saudi Arabia if he already has some sort of deal in the works. It would be too embarrassing otherwise.

I thought that made sense. I’m not sure exactly what Saudi Arabia can do, but they may be able to at least put on a show by making it look like they increasing production.

See the thing with Saudi Arabia is that they ALWAYS increase exports in the fall once their own domestic consumption (for air conditioning) begins to slow down. So that, and some releases from their strategic reserve and what-not could make for a big announcement and fan fare that makes it look like they are coming to the rescue. That makes me a bit nervous being too long oil here. I’ll keep my positions reasonably small.

Last, last thing. I put back on some of my index shorts again. I’m not unhedged any more. The market is well off the bottom now. It could verily easily keep going up. But I’m not really getting paid for heroics so I thought I’d feel better knowing that I’m not making a strictly one way bet.

I think that the most frustrating weeks in the market are the one’s where you actually get quite a bit right, but you don’t do particularly well because of it.

That is what happened to me this last week.

This was by far one of the most difficult weeks of the year for me. I have no problem with being wrong. I’m wrong A LOT. I can correct it when I’m wrong. Reevaluate, change course. But when I’m right and it doesn’t matter, that is when it is SUPREMELY frustrating. I must have said the words ‘how the hell am I not going up?’ about two dozen times this week.

As I wrote in my last post, I was finding it hard to be bearish at the end of the last week. Sentiment was awful. Everyone was acting like the world was falling apart and all I saw was some tightening and a continuation of the momentum collapse. As such, I had covered most of my shorts. While no one was calling for a rally, that is how I positioned myself.

And we got it! Exactly as I thought.

But here’s the problem. My portfolio is hardly any better off now than then. My wife’s account, where I’m a little more conservative and take smaller long positions, was actually down a bit on the week!

THAT is frustrating. It is one thing to be wrong. But it is another to be right and still be wrong.

So what happened?

Well first, there was one thing I wasn’t right about. Gold stocks. No surprise there. They kept going down. And so I lost money there and have already reduced these positions somewhat.

But my foray into gold stocks was not completely without merit. I was prescient enough to have a revelation on Tuesday. I’ve written a couple of times about how gold and SaaS move with one another with some correlation because both like low real rates. It is not a perfect correlation and other factors impact it, but there is a kernel of truth to it.

This occurred to me on Tuesday, as it also occurred to me that if we were actually going to rally, these bombed out names should do well, so I bought SaaS. I took positions in DDOG, OKTA, CRWD, SNOW and AYX. I have since sold CRWD after it took off 15% the next 3 days.

Imagine if I hadn’t. How much would I have been DOWN on the week?

This is a trade for now. I’m not really convinced this is the bottom for these stocks. I’ve been reading about A. layoffs and hiring freezes around Silicon Valley and B. declining digital ad spend. These two things make SaaS treacherous because of knock-on effects. For example – are companies going to need more JIRA licenses (that is Atlassian) if they aren’t hiring? How about Datadog – this is infrastructure monitoring where pricing is per host – are we going to see as many hosts signed up (hosts are servers or applications that need to be monitored) if companies are cutting back on spend and trying to get profitable?

So buyer beware I think. This is a trade, a bear market trade, and one I don’t want to overstay my welcome on.

Let’s see, what else. Well there was the Canadian dollar, which always works against me on an up week like this, but that is expected. And I also had a couple of single stock hiccups. Rada Electronics got acquired and the stock tanked. CRISPR Therapeutics tanked on their Innovation Day (and I made it worse by selling into the tank, buying back, selling again – indecision is killing me right now).

And then I had this damn Russell rebalancing. I HATE the Russell rebalancing. The number of times I’ve gotten hosed by the Russell rebalancing is too many to count.

Consider BCB Bancorp. This is a stock that is lucky to trade 10,000 shares in a day. You can put a bid out there and it will sit for days without getting filled. Yet on Friday BCBP traded almost 2 million shares and the stock tanked to $16.50 on a day when the market was up 100 points and the KRE (the banking index) was showing a big white candle. There was no news. I am positive it was all Russell funds selling an illiquid stock to balance out their holdings with the new index make-up.

Well at least BCB Bancorp didn’t drop 30% in the last 5 minutes of trading. That happened to Corvus Pharmaceuticals and a number of other biotechs (IFRX was the worst I saw – it went from $1.30 to 78c in the last 5 minutes).

With Corvus, because my luck is complete garbage right now, I actually started a tiny position early Friday (I mean, come on!). I talked about Corvus a while back. It is far from the perfect investment but everything has a price. It is trading under cash, has a stock position in Angel Pharmaceuticals worth $30 million, they have an anti CD-73 molecule that I think could see a partner at some point, and there is enough cash there that I don’t think a crazy dilutive raise is imminent. And most important, it has a chart that is perking up nicely.

I should say had a chart. On Friday at 1:55 Corvus completely fell out of bed as Russell rebalancing sellers sold indiscriminately. The stock went from $1.10 to 80c in maybe 2 minutes.

Look, I don’t like to add to losing positions. It is a rule I try to stick by. That goes doubly for losing positions I just initiated that day. But with Corvus, I think the frustration of the week got to me. I was fortunate (unfortunate?) to get an email alert right away saying Corvus had hit a 52-week low. Then I did a quick check to see if news had come out (it hadn’t), and I suspected this was Russell shenanigans. I knew Corvus had no data pending and I knew there was plenty of cash on handso the chance of a highly dilutive offering seemed unlikely. So I just said screw it, if you are going to give me this stock at 80c I am going to buy whatever you give me.

And that is how I became the largest shareholder of Corvus Pharmaceuticals.

LOL, I’m JOKING, JOKING, kidding, kidding. I couldn’t resist the set-up.

But I did buy some more Corvus, its a 2% position for me now, which is larger than the 0.5% position I had intended to hold earlier in the day. I am hoping to be able to reduce it back down to a more reasonable level this coming week, now that the rebalancing is over and hopefully some sanity returns.

There was one other instance Friday where Russell rebalancing gave me an opportunity that I could not pass up. I tweeted about this one.

As you know, I own Bioceres – BIOX. Its an ag tech name, they genetically engineer seeds, they engineer better fertilizer, better adjuvants. I think it is a very interesting little company that the market overlooks because its in Argentina and trades by appointment.

BIOX has a merger agreement with another company Marrone Bio. I own some Marrone Bio as well because it trades at a discount to the merger value and over the next month or two that should close.

I don’t believe there is any reason to think this merger doesn’t close. It seems to be progressing as expected. Marrone Bio has traded at about a 5-6% discount to its implied merger value for the last while, which is pretty typical stuff.

But on Friday that all went to hell. BIOX went up about 30c to $13 while Marrone Bio went down as much as 7%. Marrone Bio did it on 10 million shares traded, a ridiculously high amount.

Usually any trade with Russell rebalancing comes with the nagging uncertainty of – what if this isn’t because of the Russell? What if the timing is coincidence, what if the stock is going down just because its going down?

Well with Marrone Bio you actually had a benchmark of where the stock should trade. BIOX at $13 means fair value for Marrone Bio, given a 0.088 share exchange, is $1.144. So when Marrone Bio is trading at 97c, that is getting to be quite the discount.

As you might expect I added to my Marrone Bio position.

So those are my Russell rebalancing stories. On none of these stories was I up on the week. I lost money on BCB Bancorp, on Corvus, and on Marrone Bio. I also had a couple other biotechs that had been up with the market on Friday give up all their gains in the last 2-3 minutes of trading. Fun times.

Final topic of conservation – oil. Going into this week I had no intention of buying back any of my oil stocks. I thought I was done for good. I had sold them all back in May, then I fooled around buying them back a couple weeks ago as I was sucked in by FOMO against my own better judgement only to quickly sell them again for what I thought was for good.

But then this week the oil stocks went down, and down some more and down some more. By the end of Thursday Obsidian Energy and Crescent Point were back to levels of mid-February. Pipestone was all the way back to where it was last November!

The only reason that these stocks should be that far down is if you think this is a redux of 2008. And there is a cohort of guys on Twitter calling this 2008. But I do not think this is 2008. I think this is more like a 2001-2002 Triple Waterfall. It is going to take time, it is not going to flush out the excesses in a single swoop, it will continue to ebb and flow until all hope is gone. And this isn’t an oil triple waterfall. its a SaaS/momentum Triple waterfall.

Given that premise, I’m of the mind that this was a little over done for the oil stocks. So I bought back all 3 of the above names. And I bought back PBF Energy as well.

Just to illustrate my thinking here. Crescent Point at its low of $8.50 was, by my calculations, trading at 3x FCF on $100 Canadian dollar oil. That is getting kind of crazy I think.

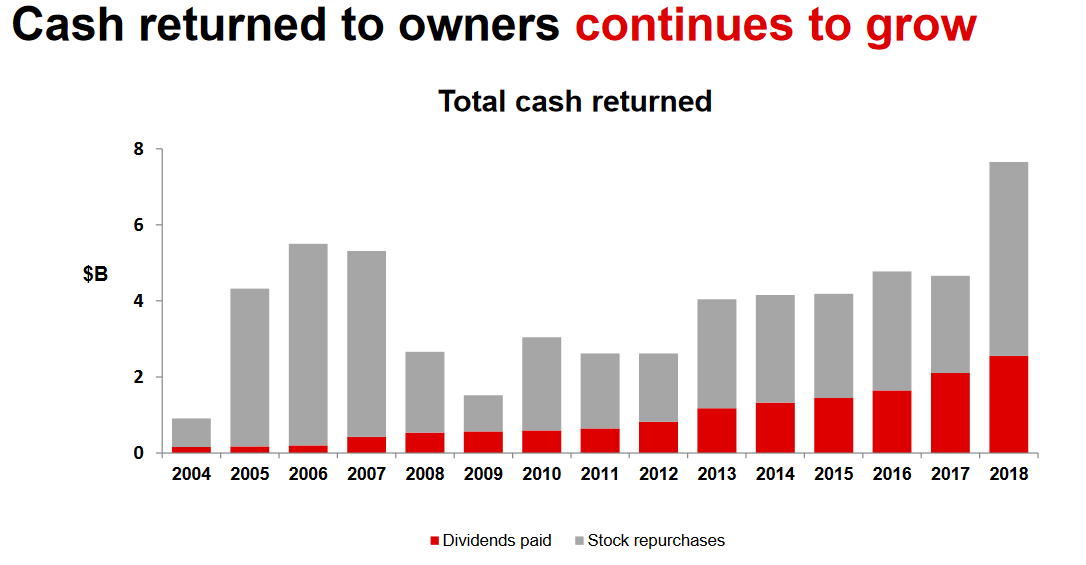

A few years ago I wrote this post where I talked about Texas Instruments and compared it to what I thought with the oil stocks.

Texas Instruments trades at a 4.8% free cash flow yield, so basically 21x free cash flow. They don’t get the valuation because their business is growing at leaps and bounds. In fact, revenue is expected to decline from $15.8 billion to $14.7 billion in 2019. Even looking longer-term, revenue was close to $14 billion back in 2010, which means growth since that time has been minimal. At best this looks like a 5% growth business over the long-run.

But Texas Instruments gets a reasonably strong valuation because the company has been very good at returning cash to shareholders. In particular, Texas Instruments is excellent at repurchasing stock.

I realize that the comparison is far from perfect. Oil is not technology. But see my point. The Canadian oil producers have transitioned to a business model that emphasizes free cash flow. Now they are beginning to return that free cash back to shareholders by buying up their shares.

That kind of sums up my thoughts here again. Crescent Point has a $150 million buyback for the first half of 2022. I betcha that is going to be higher in the second half. Remember that Texas Instruments had a flat to declining revenue business but a great performing stock for years. This was because the company buoyed its stock price by repurchasing shares and investors and traders made this a virtuous circle because they saw the shares were supported.

That is what I expected back in 2019 with the oil stocks and it is what I still expect today. Now that we have the excesses knocked out and all the Fintwit oil bulls back on their heels, I think it is worth taking a position on these stocks again.