Sito Mobile – Its Complicated

I bought Sito Mobile about the same time I made this tweet about the company.

$SITO is interesting, difficult past but very good guidance/color on call, wonder if they are benefiting from mobile shift to header-bidding

— LSigurd (@LSigurd) May 5, 2017

I was wrong with the header bidding angle, but have been right about the company (so far).

Header bidding is an advertising technology designed to source the best pricing for ad space on webpages. This isn’t the ad space that Sito Mobile operates in. Sito operates in the mobile app ad space. They have an interesting offering. Here is how Sito described what they do at the Cowen Conference last year (I’ve paraphrased a little for brevity).

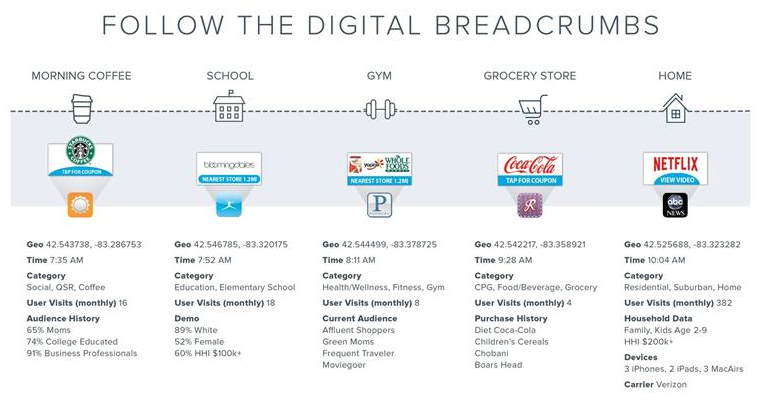

What you see here is a day in the life of a mobile user. Its important to note that when we interact with our phone and click on an app, we are raising our hand and saying serve me an ad. Our platform sees every one of those bid requests. If you look at this user (see timeline above), this person wakes up in the morning and clicks on their weather app. Every time that they click on an app we gather information. We gather a minimum of 3 data points and depending on the app and agreements, up to 30 datapoints. At minimum we gather the geo-location, time stamp, and the device ID. All the data is anonymized. That’s the foundation of how we create something called player cards.

The next time we see this device ID at a geo-location its 7:15AM. It’s an elementary school. The next time we see the device ID its at a geo-location that is a Planet Fitness. So you now see a pattern. Next we see it at a grocery store. Last we see it at 10:04AM is at a location we’ve seen the device 382 times in the last 30 days, so we can infer that this is likely the home address. Then we can get additional data from the Wifi about number of devices and carrier for that home address. We can then layer on third party data from Axiom and DLX and the like to layer on things like household income, demographics around that area, and we start to build a profile. We never know 100% but in this case we have a high degree of probability that this is a Mom, age 35-44, Caucasian, lives in zip code with average household income of $220,000, college educated, likely own their own home, average length of residence is 7 years, married and has average of 2 children ages 2-9.

That now goes into an audience that we create. We then layer in her interests and that resulting player card can then be used to target advertisers who want to speak to this consumer.

Once a user has been targeted with the ad, Sito can follow-up on the path that the user follows. Via it’s Verified Walk-in product Sito can report back whether the user subsequently entered the premises of the ad vendor, thus verifying whether the targeted ad was a success.

While some would legitimately remark that it’s scary how much can be known about you by carrying your smart phone around, the other way to look at it is that it is that the platform should result in more relevant ads being presented to users. The mobile location history that Sito collects allows it to profile the user, understand their interests and routines, and then target an ad that is appropriate and maybe even useful. And because of the real-time location data, the ad is also relevant to their current location. The verified walk-in allows Sito to report back to the advertiser with accurate metrics about the campaigns success. The value proposition makes sense to me.

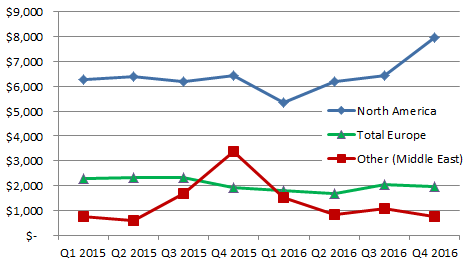

The stock price suffered into the new year for two reasons. First, the company badly missed expectations in the fourth quarter. The fourth quarter should be the best one for advertising. Yet media placement revenue was down from $10.4 million in the third quarter to only $8.3 million in the fourth quarter.

This was compounded by news of malfeasance by the CEO and CFO. Apparently they were making unapproved purchases with company credit cards, debit and withdrawals from payroll funds. In total $330 thousand dollars that were misappropriated. In February these executives resigned.

So there was concern that the companies growth trajectory was failing and concern about the void at the executive level. The stock plummeted down into the $2’s.

I got interested after the company released its first quarter results. In fact I think (I can’t remember for sure) I got the idea after reviewing a list of percent gainers the day that they reported.

The first quarter results were better than the fourth quarter. Revenue was down from the fourth quarter (not unexpected given that January is typically a dead month for advertising) but up 34% year over year. More impressive, the company said that it had its best month ever in April, generating over $4 million in revenue, and they guided to a range of $10 million to $13 million in revenue for the second quarter. This would be far above the $8.3 million of media placement revenue for the prior year.

So I like the offering and I like the recent growth trajectory. When I bought the stock at $3 the market capitalization was a little over $60 million, which meant that it was trading at less than 2x forward revenue, quite cheap if the company has indeed regained its growth mojo. Even now, at $4, its still only 2x revenue, which is not an expensive price tag if 30% revenue growth is really in the cards.

So it’s a simple story. Growth business, product/service that makes sense, they even have a wealth of data that they have archived over the past couple of years that they are beginning to monetize as data as a service and that will provide an additional revenue stream. Simple.

Except its not. The complicating factor comes from two activist groups that are looking to replace the board, replace the new CEO and CFO and I think put the company up for sale.

The two groups are the Baksa Group and TAR Holdings. The latter company is owned by Karen Singer, wife of Gary Singer, who had this interesting article written about them a few years ago. I didn’t know anything about either of these groups before investing in Sito. Singer and TAR own over 10% of Sito while the Baksa Group own a little less than 7%.

The groups say that they are not affiliated, though they seem to support each others claims and want essentially the same thing. What they want is the removal of the executive team (the CEO and and CFO) and replacement of 4 of the 5 directors. In this filing (one of many) the Baksa Group describes their position and what they are looking to change.

There are lots of complicating and curious angles here. Just to throw out a bunch of facts: Stephen Baksa was a director of Sito from 2011 to 2014. The Baksa group appears to be supported on the board by one of the Sito Directors Brent Rosenthal (the only director they don’t want to replace). One of the Baksa nominees purportedly has a “working relationship” with the Singers. Some of the Baksa nominees sit on the board or are affiliated with a company called Evolving Systems. Karen Singer owns 21% of Evolving Systems. A couple of Singer’s relatives work with Evolving Systems. And it seems like all of this activism started shortly after a March meeting between Sito management and Thomas Thekkethala, who is the CEO of Evolving Systems and was to become one of Baksa’s board nominees, where they met to “discuss a potential licensing arrangement that would allow the Company to market its products to Evolving Systems’ customers outside the United States”. It was 4 days after that meeting, on April 4th, that Sito adopted a poison pill and the activist ball got rolling.

I don’t really know what to make of the activist angle. Maybe this is all a way for Evolving Systems to take over Sito, maybe there is something else going on. I really have no idea. I’ve read through all the filings and I honestly couldn’t pick out any tidbits that gave me certainty about the outcome. Where we stand now is that the Baksa group has delivered a proxy signed by 58% of common shareholders supporting their proposals to remove the current executive and directors and replace them with the Baksa slate. Sito has responded that they are having a third party do a count and validate the results and will report back next week.

While I am really not sure about the outcome, it seems to me that its at least possible that this ends in some sort of acquisition of the company. Management has their backs against the wall with the recent proxy. The easiest way out of the corner is a takeover, either by Evolving Systems or some other white knight. And if it doesn’t happen, there are always the fundamentals to fall back on, which is the real reason I bought the stock.