Adding more Mortgage Insurers

I have already written about how I stumbled upon MBIA Inc. (MBI) as I was researching mortgage insurance companies and in particular MGIC. My interest in the mortgage insurers has been brought about by my desire to seek out companies that might benefit from a turn in the housing market.

I am not looking for a hockey-stick-like turnaround in housing. I don’t expect to see prices or new constructions having a significant rise any time soon. But I do think its plausible that we are at a point where things no longer get worse.

How to play the bottom

Thus far, I’ve looked to play this bottom in a couple of different ways.

My foray into the servicers has been an attempt to capitalize on the premise. Nationstar Mortgage (NSM), Newcastle Investment Corp (NCT), Home Loan Lending Services (HLSS), PHH Corp (PHH); all are examples of companies that should benefit from a stabilization in the mortgage market. So far the thesis has paid off and I am up (since my purchases at the beginning of the year) well over 50% on Nationstar, about 30% on PHH Corp, and 15% on Newcastle (not counting the dividend).

I have also been able to capitalize on the trend by jumping into select regional banks that had exposure to the mortgage market turnaround. Both Rurban Financial (RBNF) and Community Bankers Trust (BTC) have been big winners for me here, returning thus far 50%+ since the beginning of the year.

I now have have a third business for playing the housing bottom. The insurers. In addition to MBIA, last week I bought a fair position in Radian Group (RDN) and a lessor position in MGIC (MTG). I also added a little to my position in MBIA (MBI). In the case of Radian I unfortunately didn’t catch the bottom in the stock, but at least was fortunat enough to have gotten in well before the week long run ended, and I am actually seeing quite a profit on the position already. Trades in my practice account that I track here are shown below:

Why Insurers?

I tend to have a lot of significant thoughts on my bike ride home. It must be something about the state of semi-awareness that biking down major thorough fares in rush hour does to one’s brain. On the one hand, what with cars whizzing by you and changing lanes and pulling out you are always on alert. On the other hand, its the same ride you have done hundreds of times and so it is easy to day-dream yourself into a whole other world of thoughts.

It was about a month ago that I was biking home from work and thinking about what other businesses could benefit if the housing market in the United States just stopped getting worse when it occurred to me that I really should be looking at the mortgage insurers. If ever there was a business whose livelihood was dependent not on a robust recovery in housing but instead an end to the continual decline, it was the insurance business. As a mortgage insurer, you are less concerned if prices rise or new sales increase than you are that people don’t default on their loans. Clearly, people not defaulting on their loans is the necessary condition to any housing recovery.

This appears to be happening.

The most recent Home Price Index (HPI) report, put out by CoreLogic, said the following:

“We see the consistent month-over-month increases within our HPI and Pending HPI as one sign that the housing market is stabilizing,” said Anand Nallathambi, president and chief executive officer of CoreLogic. “Home prices are responding to a restricted supply that will likely exist for some time to come—an optimistic sign for the future of our industry.”

Meanwhile, according the CoreLogic Shadow Inventory report, serious delinquencies in some of the hardest hit areas are showing big year over year declines:

Serious delinquencies, which are the main driver of the shadow inventory, declined the most in Arizona (-37.0 percent), California (-28.0 percent), Nevada (-27.4 percent), Michigan (-23.7 percent) and Minnesota (-18.1 percent).

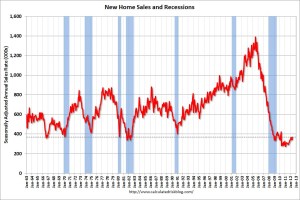

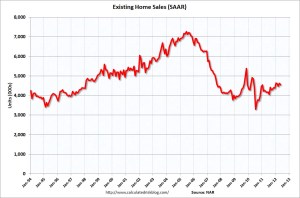

A look at charts of new home sales and existing home sales (taken from CalculatedRiskBlog) show a pretty clear bottom.

My thesis was echoed by Radian management on their Q1 conference call.

We believe our core mortgage insurance business is attractive with strong returns, outstanding credit quality and sound pricing.We continue to capture a much larger share of new mortgage insurance business today than ever before in our history in an extremely competitive but high quality market.

Radian further echoed the sentiment that defaults are declining at the KBW Mortgage Finance conference:

You saw our press release this morning. In addition to the strong level of NIW, delinquencies continued to decline. So in May they declined again. Primary delinquencies fell below 100,000 for the first time in quite some time. In addition, the new default line, which really drives the incurred losses, was down 25% from May 2011. So year-over-year on a monthly basis down 25%, and that is a greater reduction than our projections have shown.

Insurers like Radian and MGIC stand to benefit from another trend that I called out in my post Pounding the Table on Mortgage Servicing Rights a few months ago.

Now we have the opposite scenario. Lending standards are so tight that only the most fool-proof borrowers are able to get loans. The risk of default should be greatly reduced. The result again is for the MSR to stay on the books, paying out cash, for longer.

When I had looked at Radian and MGIC last year, one thing that made be skeptical was that they weren’t writing enough new business. The same can’t be said any more. In particular in the case of Radian,they are writing significant new insurance:

In fact, our market share of this profitable new business is double what it was in the challenging underwriting years of 2005 through 2008 and this increased volume is improving the overall credit profile of our MI portfolio. In the first quarter, we again wrote $6.5 billion of new mortgage insurance business and our pipeline remains strong with new insurance written (NIW) reaching approximately $2.6 billion in April.

Again at the KBW Mortgage Finance Conference, Radian provided at update that in May saw an additional $2.7B of NIW. They also put some numbers to the exposure to the legacy book of insurance, versus the newer insurance written:

With our increasing market share we have grown the composition of the higher-quality books 2009 and subsequent at a much greater level than some of the other MIs that have legacy exposure. So as of March 31, we are up to 31% of our risk in force. That is from the 2009 and subsequent books. And, importantly, the 2006 and 2007 vintages, those poorer vintages, are down to 31%. By the end of 2012 at the rate we are going, the 2009 and subsequent are likely to be in the 40% range of our risk in force.

More to Come

These are complicated businesses and it is going to take me some time to fully wrap my head around the potential. My positions thus far are reasonably small because of this. As is often the case for me, my initial investment provides the incentive to investigate further, and if I like what I see I buy more. I just hope that the stocks don’t run away from me before that happens. I expect to come up with more detailed write-ups about both Radian and MGIC in the near future.