Week 53: Betting on a Housing Bottom

Portfolio Performance

Portfolio Composition

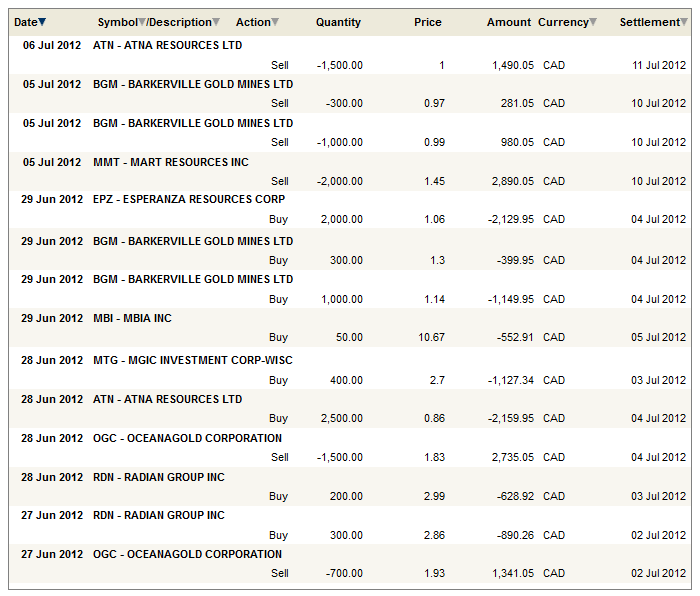

The trades that took place in the last two weeks can be viewed here.

Summary of Portfolio

There were a couple of positions that had big moves over the last few weeks. The first is Nationstar Mortgage Holdings (NSM). Nationstar is now more than a double from my original purchase and up over 75% for the entire position. Both Nationstar and Newcastle Investments (NCT) have been strong of late, and I think that’s likely due to the expectation that they will win the ResCap bidding war. According to an 8-K filing that Nationstar made on Thursday, their bid for ResCap was raised $125M. At this point the risk is that they don’t win the bid and that the stock falls back. However, I bought the stock well before the Rescap sale and I still believe that there is some upside even ignoring Rescap. Even without the Rescap deal, Nationstar has grown substantially through the purchase of the Aurora portfolio and Bank of America’s servicing assets. I’m reluctant to sell any shares yet.

Another stock that has had quite a run is Rurban Financial (RBNF). The last time that I talked about Rurban was mid-May, and I haven’t mentioned them since because, well, nothing has happened. The stock is boring and goes up. I like that. However if you had asked me back when the stock was $5 when I would consider selling I probably would have said around $8. We are getting close to that number now.

As I wrote about earlier this week, I added positions in two monolines, Radian Group (RDN) and MGIC (MTG). Of the two, I am most inclined to add to Radian on any pull back. I’ve been reading whatever I can get my hands on about the mortgage insurance industry over the last week and I think I have wrapped my head around most of it. The regulatory landscape is really quite mind-boggling, the changes that have taken place since 2008 quite tectonic and there are about a million acronyms used with many of their definitions not easily found.

Nevertheless, out of chaos come opportunity.

I really like what I see in the insurers; the leverage to a housing bottom (just a bottom, not a barn-burning recovery), the cheap price (close to being priced for bankruptcy), insuring what are probably some of the best quality mortgages they have ever insured, margins increasing as their government owned competition, the Federal Housing Authority (FHA) raises their prices in an attempt to limit the government market share, and the insurers stand to benefit from the general stance that seems to have evolved that government should limit their role in the housing industry and that private insurance should take more of a role.

What holds me back from making these insurers larger positions is the economy itself. A recession would not be good for housing. Nevertheless, I am somewhat emboldened by the fact that the stocks I own that are dependent on the US economy (in addition to those discussed already I would put Community Bankers Trust (BTC) , MBIA (MBI) and PHH Corp (PHH) into this bucket as well) have held up quite well in this latest downdraft.

What I sold

I sold Mart Resources (CA:MMT) this week (note that while I sold the stock in the portfolio I track here, I do still own a position in other portfolios). When I originally bought Mart four weeks ago I wrote the following

The company has two news events that I suspect are going to occur shortly. The first is the potential for an announcement of a dividend. I believe that such an announcement could result in a significant pop in the stock, as it gives credibility to what is otherwise looked on warily as a Nigerian story. The second is a pipeline deal with Shell, which would allow Mart to increase their production, perhaps substantially, and allow the brokerages that follow the story to up their targets based on larger 2013 volumes. Again, I am looking for an event to occur in somewhat short order, but I am not holding this stock for the long run.

Mart released news earlier this week that they were going to provide a quarterly dividend of 5 cents a share and a special dividend of 10 cents. They announced the pipeline deal a week before that. The stock is still cheap; it trades at maybe 4x cash flow (which does not consider the production expansion that will come in the next year) and at a rather silly 14% yield. I’ll probably buy back in at some point, maybe even soon. I just don’t love the way the market is behaving, in particular the way that Spanish bonds have jumped back to nearly 7% and so I am reluctant to . I also don’t rally buy this oil rally; it seems prefaced on Middle East tensions and that is fickle mate. Mart, having moved so much higher so fast, seems like it would be likely candidate for portfolio trimming if oil drops again below $80. I’ll wait this out and see what happens over the next couple of weeks.

I sold some OceanaGold (CA:OGC) in the last two weeks. Part of what I sold was because I thought that Atna Resources (CA:ATN) had gotten too cheap again at $0.85 and so I moved money from OceanaGold to Atna. I have also been researching Esperanza Resources (CA:EPZ) and I thought that they, having been hit from selling after a share offering but now having plenty of cash and owning my preferred heap leach deposit that will be low capital expenditures and low cash costs, were in a better position in this uncertain environment. The other reason behind the selling was that these gold stocks just aren’t working. The jobs report on Friday should have sent gold flying, but it didn’t. The thesis I have expected isn’t playing out. Whether that is because the Rupee is so low that Indian demand is sluggish, because investors aren’t willing to think of gold as a safehaven just yet, or because there is a nefarious plot to undermine gold being played out in smoky dim lit rooms on the outskirts of Washington, the bottomline is that it hasn’t been working. And I always try to do more of what works and less of what doesn’t.

Finally, my adventures with Barkerville ended on Thursday when I sold out. The deciding factors were that the stock wasn’t behaving like a stock should if it truly had a 10 million ounce deposit (though the alternative explanation that the weakness is being caused by warrant holders cashing out could be contributing), and that the data that is available from the company just doesn’t look like 10 million ounce material (if you look at the 7 sections that Barkerville has on their website, it looks like Cow Mountain has a number of narrow (albeit potentially high grade) veins. It also looks like the veins are somewhat sparsely populated across the length of the intercepts.

I honestly have no idea what Barkerville does or doesn’t have and so I have decided to make discretion the better part of valor until such time that I do.

{kind=link}