Week 76: A Few New Directions

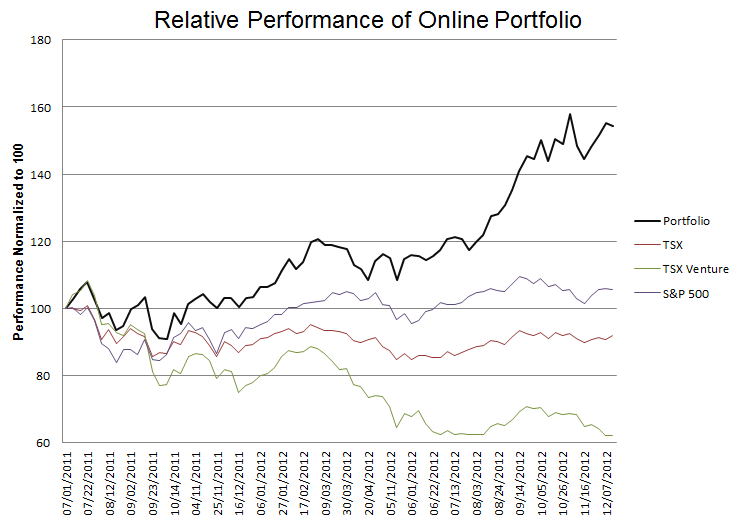

Portfolio Performance

Update: New Positions and My Method

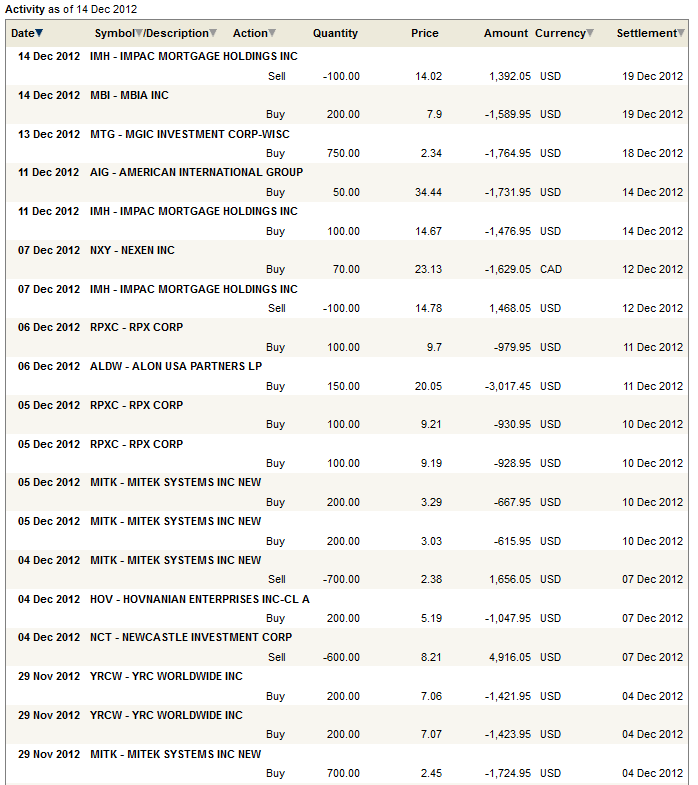

I added starter positions in a few new names in the last three weeks. A couple of these (RPX Corp and Mitek) I have already written about. The other four positions that I started were in YRC Worldwide, AIG, Alon Energy Partner and Nexen.

Apart from Nexen, which was a special situation, the other stock positions are small, and were initiated because I thought the stocks warranted further review. This is my process. I like to add stocks that look promising, which incentivizes me to look at them closer. This technique might not be for everyone, but it works for me.

It’s difficult to explain why the process works for me. When I have some money on the line I tend to churn the idea in the back of my mind, and over time my opinion on the position becomes clarified. I begin to like it more or not at all. If I don’t take a position, I tend to forget about the stock altogether, and my analysis ends without any real conclusion.

Of course in the mean time I do have money on the line, so there is the chance for real gains or losses. But usually these aren’t significant, and anyways, I only do this with names that I have done some initial digging on and have deemed have som promise. I may lose a few dollar or make a few dollars on these positions over time, but any losses I would chalk up to the cost of doing business.

I have since taken a closer look at three of the six.

RPX Corp

I am not that enthused with RPX Corp (RPXC) and Mitek (MITK); I will probably jettison those picks in the next week or so. You might have been able to guess as much by the tune of my posts on each company (here and here respectively). In the case of RPX Corp, I struggle to see the catalyst that would move the share price higher, the earnings are not high enough to put it in the “insanely cheap” category, and the insiders, who have been selling a lot of shares, still have a lot left to sell at strikes significantly lower than the current price.

Mitek

As for Mitek, its too hard to figure out whether the banks they’ve signed up will translate into revenue and earnings. I just can’t quantify the business model. This may become more clear in another quarter. I realize that by the time it does the stock may be significantly higher. But I think I’d find it easier to enter at a higher price if there was more certainty about the outlook.

YRC Worldwide

I am, however, enthused about YRC Worldwide (YRCW). The stock is no sure thing, but the upside is compelling. I’m about 80% through a write-up on the company. Its taken some time to get through; the debt, union and pension liabilities have made an analysis tricky and my learning curve steep. Its an interesting opportunity because it isn’t a name that I would come out and say I’m confident its going to work out and go higher. What I am comfortable saying that if it does work out, its going much, much higher. And that counts for something.

Nexen

The Nexen (NXY) idea was admittedly a bit of a spec impulse. But not entirely. I mean, I live in Calgary, I work in the industry, I have been reading and breathing all things Nexen since the CNOOC bid was announced. I also know the Conservative government, their roots are under this very city. I just couldn’t see them letting this deal fall through. But I also couldn’t justify buying Nexen at $25 just to make a couple bucks. But when it dropped below $23 on the announcement of the announcement, I couldn’t resist.

AIG

What can I say about AIG (AIG) that hasn’t already been said? I’ve read a lot about the company, including an excellent book called “Fatal Risk” that described the rise and fall of the company under Herb Greenberg. Last year I missed the run-up from $20 to $30 and ever since that time I have been on one of those never-satisfied journeys for the perfect entry point. When I saw that the government was selling out of its holdings completely, I decided that may never happen, and I took on an initial position. This is one I am going to add to as it goes up.

Alon Energy Partners

I’m actually looking at two companies here, both Alon Energy Partners (ALDW) and its parent, Alon USA Energy (ALJ). The idea started with Alon Energy Partners, which is a single refinery MLP that is making tremendous margins right now because of crude differentials and should be providing a tremendous dividend next year (somewhere on the far side of 20%). I started my research on both names this week and while I am getting more comfortable with the idea, I have more work to do before I will come out and say that either is a steal. But there certainly might be a steal here; maybe two. The refinery that Alon Energy Partners owns (called Big Springs) is in Northern Texas and is ideally positioned to pick up crude from the Permian and other inland Texas plays. The differentials on Midland crude to Cushing WTO has widened out into the double digits. They also are benefiting from the differential between Brent and WTI, creating a double whammy that is leading to extremely high margins. Alon Energy has an 84% ownership as a general partner in Alon Partners. In addition they own 3 other refineries, one located inland Louisiana, and two others, both unprofitable at the moment, in California.

The main jewel for both companies is the Big Springs refinery. While I realize that the current level of margins, which were $28 per barrel in Q3, aren’t sustainable, I like the idea that they are less unsustainable than people think. There is a lot of crude coming on-line from shales and tight oils in Texas, and there may be more coming from new developing plays like the Cline Shale. And given the election results, building pipeline infrastructure is going to continue to be difficult, which should support differentials between Cushing WTI and Brent.

What I have not yet done however, and what I really need to do to get comfortable with the play, is take those general ideas and puts some details to them. I need to answer questions like, what pipelines are being built and where, how much is Midlands production expected to grow and as a consequence of these factors, just how long are these margins sustainable.

There is an extremely good article on Seeking Alpha about Alon that will give you a lot of the background needed to understand the company.

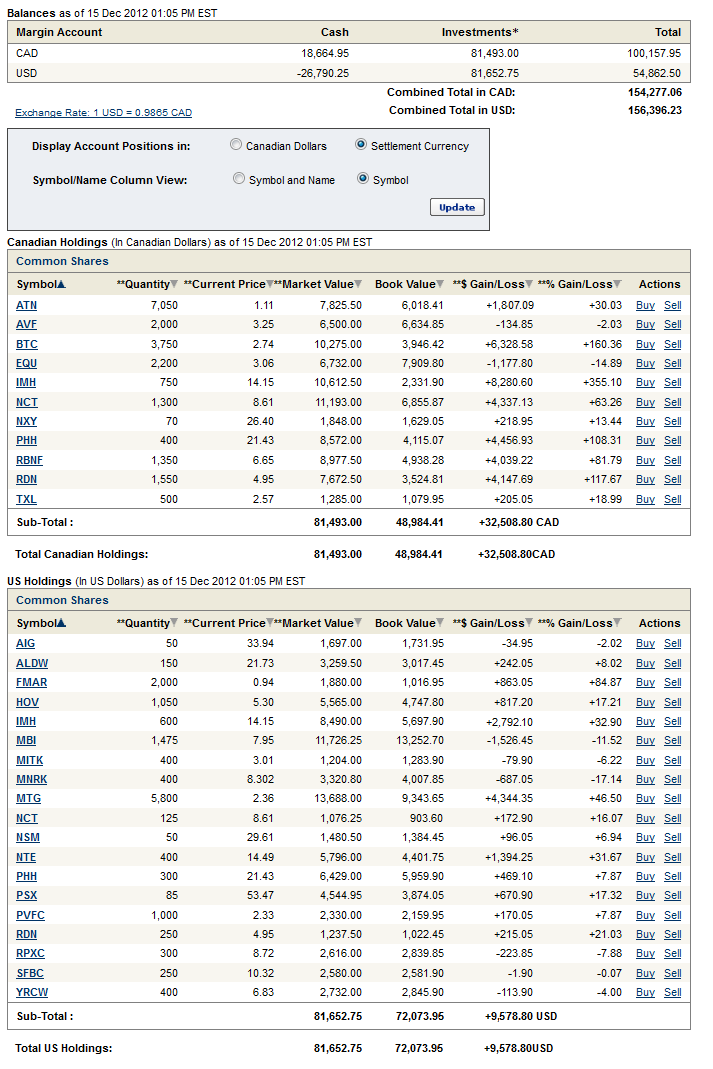

Adding to MGIC

Apart from these new additions, I made some of the typical portfolio adjustments, adding to some positions and subtracting from others. Of all of these, I want to focus on my purchase of MGIC earlier this week. MGIC is now my second largest position, which admittedly might seem like a somewhat crazy thing to do.

But keep in mind that this was a $2.50-$3.00 stock prior to when the second quarter Freddie Mac dispute was announced. And it was only last April that this was a $5 stock. With Freddie Mac ending in a positive resolution, and with the housing market continuing to show life, MGIC continues to work past its legacy issues. If (and this remains a big if) the fiscal cliff is avoided, MGIC could end up being one of those companies that shoots higher as a result. Of course if it isn’t, and 2013 becomes the year of the recession, well… I’m going to be doing a lot of fleet footed portfolio changes early in the new year.

A Few Other Moves

Finally, I lightened up on my position in Newcastle Investments, and man was I wrong to. When Newcastle got down to $7 last month I really loaded up on the stock (it was, for a time, my second largest position), and as it moved back above $8 two weeks ago I took some of that off. I thought that the stock would continue to see pressure into year-end because of dividend tax worries. Not the case. Oh well, my remaining position is still substantial so I’m not going to complain.

On one last note I like to highlight some of the stocks I have only started to look at, and to which I can’t yet say very much but of which I may be writing about in the future. These include Niko Resources, which is an idea I got from Will on twitter, Mitel, which I picked up on a stock screen a few weeks back, Tricon Capital, an idea I got from a correspondence I made from this blog, and Gravity, a software company that was recommended by Benji Gallander on Market Call this week.

Portfolio Composition

Click here for the last three weeks of trades.

{kind=link}

Are you interested in YRCW bonds? If you think that perhaps they’ll go BK then you definitely don’t want their equity. If you think they’ll survive then go for the bonds. Don’t own equity, the lowest class, when yield are that high on their bonds.

I’ve looked into this. I think this could be a very good way to play YRCW. Unfortunately they are going to be a real pain for me to buy. Being Canadian, none of the brokerages I deal with make them available so I have to set up another account somewhere else where I can. My laziness has so far set in on this… at any rate while the stock has more downside then bonds, it also has more upside to a recovery at YRCW.

NXY is now based on a US CFIUS review. Although I agree w premise and NXY CNOOC have said us gulf platforms could be divested, this isn’t over. Look for some comment from U S war hawk to scare the f outta u and me and push one last dip before marriage. This has always been about CFIUS tried and still is today as USA military bases and China don’t mix. Enjoy.

J

I’m not sure if the US assets are material enough to be worried about this. If the CFIUS denied the sale would’t CNOOC just sell those assets? They aren’t the reason CNOOC is buying Nexen

I think you have the wrong link up there for the Seeking Alpha story.

Steve

You’re definitely right about the potential crude in the Cline Shale. At an estimated *30 billion barrels* of recoverable oil, it would dwarf every play going today. http://bit.ly/SztnVy