A very leveraged bet on trucking: YRC Worldwide

YRC Worldwide is a small position for me and, barring a significant move up, it is going to remain a small position. Nevertheless, its such an interesting idea that I want to go into some detail to explain my thinking here.

YRC Worldwide is the amalgam of two nationwide trucking companies, Yellow Transportation and Roadway, and three regional companies, New Penn, Holland, and USF Reddaway.

The business combination of the Yellow and Roadway nationwide was completed in July of 2003. It was followed by the acquisitions of regional truckers New Penn, Holland and USF Reddaway between 2003 and 2005. Along with the acquisitions came a heavy debt load, of which about $300 million unfortunately came due at perhaps the worst time possible, during the economic collapse of 2008.

Since that time the company has been in a battle to dig itself out of the debt hole; it has gone through a couple of workforce restructurings, a restructuring of its labor contracts and pension contributions, and a restructuring of its debt (which diluted existing equity to almost nothing).

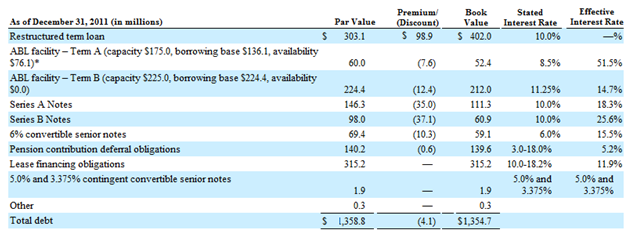

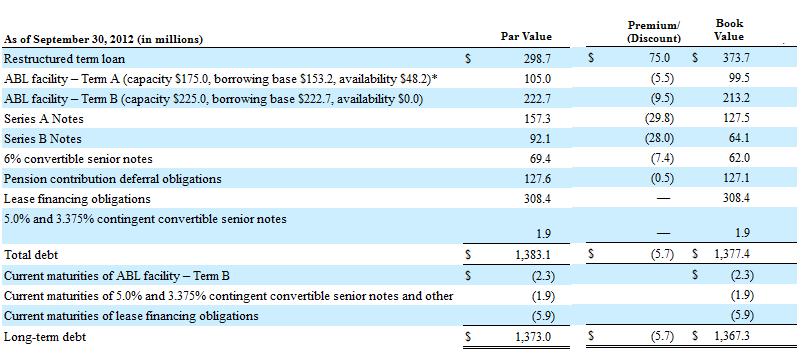

Even after all of this, the balance sheet remains ugly. Below are the company’s on-balance sheet liabilities.

There are also off-balance sheet liabilities associated with the company’s pension plans. The company has both a pension plan that they run themselves (they refer to this as their single employer pension plan) and other union run plans that they contribute to along with other unionized employers (referred to as the multi-employer pension plan). All of their plans have significant net liabilities.

A closer look at the pension plans

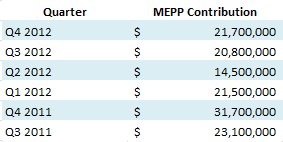

The single-employer plan covers about 14,000 employees. The funding liability, which is basically the anticipated deficit between the plans assets and liabilities, was $438 million as of year end 2011.

The company is funding this liability by making cash payments each year that exceed the nominal payments that would otherwise be required. This excess cash payment is determined by law and is a function of the expected returns and anticipated plan deficit going forward. In 2012 the company made cash payments of about $70 million. Below are the expected cash payments for 2013 and beyond.

The actual cash contribution can jump around quite a bit depending on the assumptions used and the actual returns accrued to the pension. At the beginning of 2011 the expected contributions from 2014 through to 2016 were over $100 million per year.

Worth noting is that the cash payments differ from the expensed payment that goes through the income statement (where it is expensed as an item within the Salaries, Wages and Employee Benefits). The expensed amount passed through on the income statement is around $30 million per year. Cash payments are higher to make up the deficiency in the fund and will continue as long as the plan has an unfunded liability.

If you think the single employer pension plan is ugly, the multi-employer plan is worse. In the 10-K the company makes the following statement about the state of the multi-employer pension plans that they participate in.

We believe that based on information obtained from public filings and from plan administrators and trustees, our portion of the contingent liability in the case of a full withdrawal or termination from all of the multi-employer pension plans would be an estimated $9 billion on a pre-tax basis. Our applicable subsidiaries have no current intention of taking any action that would subject us to payment of material withdrawal obligations.

When a number like $9 billion is thrown out there, it is worth examining.

In 2009 YRC Worldwide was on the verge of bankruptcy and there was no way they were going to be able to meet their multi-employer pension contribution requirements. They were able to strike a deal with the Teamster union that gave them a payment holiday on the plan. This lasted from the third quarter of 2009 to May 2011. Subsequent to that, YRC Worldwide has been contributing to the multi-employer pension plan on a reduced basis of 25% of what its contribution would typically be. The contract that is in place runs until 2015, so for the foreseeable future the company will continue at the reduced rate. The contributions the company is currently making to the multi-employer pension also are part of the Salaries, Wages and Employee Benefits on the income statement, and are roughly the numbers below:

Now onto that truly frightening figure of what it would cost to get out of the multi-employer pension plan: $9 billion dollars. It is worth putting this number into context. Based on the research I have done, the reason that the cost of exit is so high is because of the rather insane structure of the multi-employer pension plan. The way it works is that as employers run into financial difficulty and can’t pay their pension dues, their obligation falls on others to make up the difference. This is probably the quintessential example of a house of cards. As companies fall by the way side, the burden grows for the remaining participants, making it more likely that they too will not be able to fulfill their obligation. In my opinion, something has to give. It is in nobody’s best interest, not the workers, not the union and certainly not the companies involved, to continue burdening them with other people’s debt. But I admit that I do not know how this plays out and it could get pretty ugly going from A to B.

While the play out of these long-term issues could be rough, in the short term I am more focused on the fact that the pension costs are known and quantifiable over the next two years, and that the company is approaching profitability at an operational level with that expense. The existing agreement that YRC Worldwide has with its unions is good until 2015. And the single employer plan stands to benefit from any pick-up in the US economy. With respect to the longer term issue of how the multi-employer plan plays out, I have little more to add, expect to say that well before that time my thesis is going to have played itself out one way or the other. I hope to be long out of the stock before this problem has to be resolved.

Looking Past all That

There is an obvious question here: Why am I investing in a company with this many problems?

I am always on the look-out for opportunities that will result in out-sized returns. And while I can find a lot of solid companies with strong balance sheets that have good prospects, usually the market already knows about these companies, and the return potential is measured in low double digits at best. In order to find companies that have multi-bagger potential, you have to go into some pretty ugly scenarios, accept them for what they are, and figure out if there is a chance that they can dig themselves out of the hole they are in. Witness my investments in MGIC and Radian, or even Impac Mortgage, earlier this year as recent evidence of this.

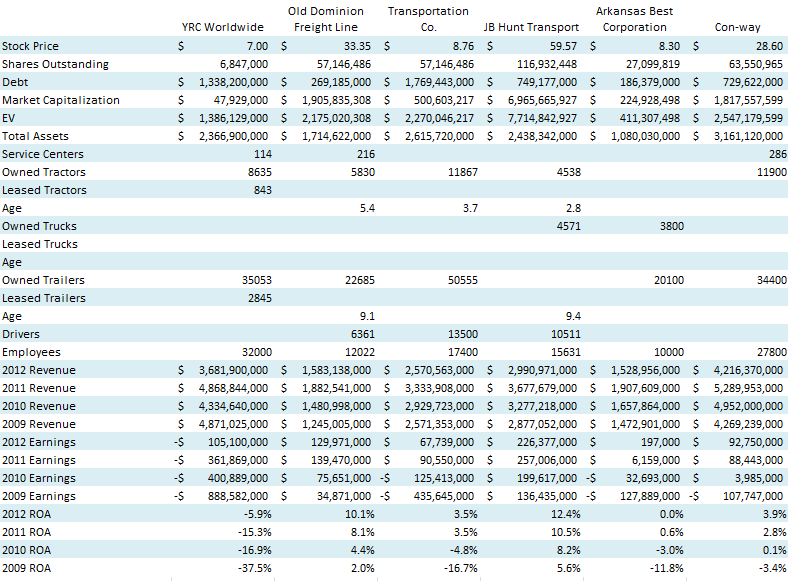

The table below compares YRC Worldwide to a number of its competitors in the less-than-load and general freight trucking business (Note that I put this table together a few weeks ago so the stock prices are a bit dated, but its the relative magnitude of valuation that is important here and they have not changed much).

Two key points are illustrated by this table:

- The equity at YRC Worldwide is a tiny fraction of its debt

- If YRC Worldwide were to reach a comparable valuation with its competitors, the equity would be worth multiples of what it is today

(A third point that might be made, but which I will explore in another post, is that Arkansas Best also looks like it also holds promise)

YRC Worldwide has a little less than 7 million shares outstanding right now. The lowest conversion price of any of the convertible debt is $14, so it can be ignored for the time being (if I got $14 out of the stock it would be time to re-evaluate). As far as earnings go, a 10 basis point move in the operating ratio of the company as a whole creates about $4.5 million in income. That is $0.64 per share. It doesn’t take much of a change in the operating results to create big swings in earnings.

And while big swings in earnings have been almost exclusively to the downside over the past 4 years, there are signs that the ship might be turning. The last few quarters have been marginally profitable.

Consider the following:

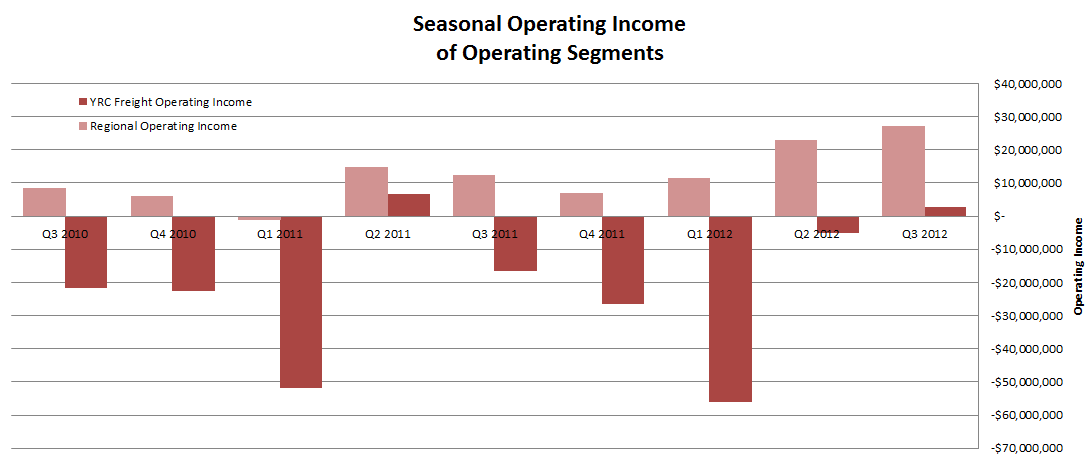

- The third quarter was the first quarter in over 5 years where both YRC Freight and the Regionals both put together an operating profit. The Regionals had income of $27 million while YRC Freight had income of $2.8 million

- The Regional segment is outperforming its competitors. The operating ratio is a metric commonly used to compare the efficiency of trucking companies. The operating ratio is quite simply the direct expenses divided by the revenues. In the third quarter the regional segment put up an operating ratio of 92.5%. This was the second best ratio of any publically traded regional provider, including non-union competitors.

In my opinion the problem has been less that of a company that has a lot of debt, and more that the assets that back the debt are not generating a return. While YRC Worldwide has a significant amount of on-balance sheet debt, it’s really not that far out of line with other companies of similar size when measured by revenue and could quickly become in-line if the company can show some top-line growth.

Listening to the last couple company conference calls and reading prior reports paints a picture of a company that took on unprofitable business, made poor investments, let their operating efficiency and customer service slide, and did all of this at a time where the US economy hardly grew. It was a little over a year ago that a new management team was put in place to try to turn around the company.

Year over year results of both YRC Freight and the regional carriers have shown consistent improvement. Below is the quarterly operating income of both segments.

What is made clear by breaking out the regional and national segments is that the stage of turnaround of the two segments is quite different. The turnaround of the regional carriers is already well underway. The businesses are profitable and in the third quarter the regional carriers performance was the second best of any regional less-than-load trucker, including their non-union competition.

The national business, YRC Freight, has a lot more work to do. Up until this year the national business was in disarray. Before the introduction of the current management team, YRC Freight did not even have a dedicated management team of its own. It was being run at arms length by the holding company. Morale was poor and efficiencies were non-existent. But that appears to be in the early stages of turning itself around. When you look at the operating income of the Freight segment you can discern that some improvement has begun to take place in the last year, but that there is still a long ways to go.

The bet here is that the improvement at YRC Freight continues. There is no question that in the aggregate, as measured by the operating statistics, the company has improved its performance since the restructuring in 2011. If this can continue, and really that is what this is a bet on, then the debt may not be as unmanageable as it seems to be now.

A closer look at the debt

Because the debt is such a big part of the story, I think its worthwhile to review it in detail. Below is the total on-balance sheet debt of the company.

Next I want to point out some of the key features of each of the debt instruments.

Term Loan

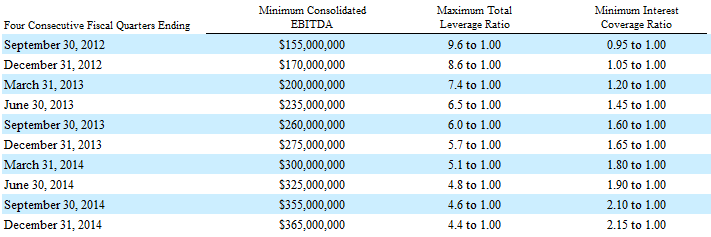

The principle amount of the term loan was a little less than $300 million at the end of the third quarter. It is due March 15, 2015. There are a number of covenants associated with the term loan that would have been a problem already if they had not been amended. The amended covenants are shown in the table below:

The company is in compliance with all of these covenants as of the third quarter. The EBITDA covenant has been the most difficult to maintain, but they were about $50 million above the covenant amount in Q3.

Asset Backed Facilities

The asset backed facilities are pretty straightforward. The following 5 points, taken from the 2011 10-K, summarize the facilities:

- Size: Our ABL facility provides for a $225.0 million ABL last-out term loan facility (the “Term B facility”) and a $175.0 million ABL first-out term loan facility (the “Term A facility”).

- Term: The ABL facility terminates on September 30, 2014

- Collateral: The ABL facility is secured by a perfected first priority security interest in and lien (subject to permitted liens) upon all accounts receivable (and the related rights) of the ABL Borrower

- Covenants: The ABL facility contains certain affirmative and negative covenants and “Termination Events,” including, without limitation, specified minimum consolidated adjusted EBITDA, unrestricted cash and capital expenditure trigger events (that are consistent with the credit agreement), and certain provisions regarding borrowing base reporting and delivery of financial statements.

Series A Notes

The Series A Notes mature on March 31, 2015. They pay interest at 10% per year.

As of year end 2011, there was $146.3 million in principal Series A Notes outstanding after considering “payment in kind”. What payment in kind means is that instead of YRC Worldwide making cash interest payments, they pay interest by issuing further principle. This conserves cash. The company “paid in kind” about $22 million of interest from the Series A and B notes in Q3.

There are convents on the Series A but these apply to limitations on what can be done with the assets that back the notes, and not operating conditions on the company.

The Series A Notes are convertible into shares of our common stock at the conversion price per share of approximately $34.02. If all the notes are converted it will result in abut 6 million shares.

Series B Notes

The Series B Notes are similar to the Series A. They bear interest at 10% per year and mature on March 31, 2015. Interest is paid in kind. And they are convertible to shares. There is $6.3 million in principle outstanding. The Series B is convertible at $18.54 and if the full amount was converted it would create 7.7 million shares.

6% Notes

There are $69.4 million in principal outstanding of 6% convertible senior notes. The 6% notes are due February 2014. Even though the notes are convertible, the convertible price is so high that they effectively are not.

Lease Arrangements

In 2009 YRC Worldwide sold assets to pay back debt and then entered into agreements to lease back those assets. Below are the relevant facts about the agreement.

- During 2011, 2010 and 2009, we received $9.0 million, $45.0 million and $315.5 million, respectively, in net cash proceeds from lease financing transactions with various parties

- The underlying transactions included providing title of certain real estate assets to the issuer in exchange for agreed upon proceeds

- We are required to make monthly lease payments, which are recorded as principal and interest payments under these arrangements, generally over a term of ten years, with effective interest rates ranging from 10% to 18.2%.

The debt runway

Probably the most important point about the debt is that nothing significant comes due until March 2015. Between now and that time the only debt maturity is in February 2014, and that is for $69.4 million. The company has a run way. If operating performance can continue to improve over the next year, an in particular if the turnaround at YRC Freight can take hold, refinancing the $69 million shouldn’t be a problem. If that continues through 2014, we should be looking at a significantly different company by the time the debt matures.

I know it’s a lot of if’s. As I wrote in my post a few weeks ago, I would not characterize myself as “confident” that the company will turn itself around. I think its possible, that there are reasons to believe that it will happen. But if it happens, the reward is going to be huge. I think its reasonable to expect that if the YRC Worldwide became profitable the stock is a double or a triple from $7, where I purchased it.

Putting on a Valuation

While I’ve thrown out a lot of numbers, both with respect to debt and earnings, I’m really reluctant to go a step further and forecast what earnings could be or what the stock price might be worth as earnings improve.

The value of the equity is a call option on the success of the turnaround. If you look at the competition you can get a sense of what the value might be, and it is clear we are talking multiples here. All hinging in if, and to what degree, management is successful.

Whether they are successful depends on a lot variables. The strength of the US economy. The motivation of the workforce. The success of the initiatives to improve efficiency. The drive of the sales staff. A lot has to come together.

So its a watch and see story. I have my position. I will sit on it and see how the next quarter goes. It could be a tough one. Hurricane Sandy is going to have an impact. Additionally, the quarter is typically seasonally weak. But less than the absolute performance I will be focused on how things are doing relative to the previous year, particularly at YRC Freight. Management comments on the state of the business will be equally important. If the turnaround is in tact, I will hold and maye even add, while if not, then I’m out. We’ll see how this pans out.

Lane:

An excellent writeup as usual.

i almost passed this one by, as the trucking industry is so difficult, and is plagued by low returns.

What I find so compelling is the sales leverage behind these shares. The company is trading for .01 Price/sales ratio. Each share has over $600 of revenue behind it.

If, in a couple of years, if YRCW can simply keep 1% of revenue, they will make over $6/share!

I was looking at some other financial metrics…

One concern I have is that the depreciation of their fleet has to be made up at some point. The tractors & trailers will definitely wear out and have to be replaced. What happens when all the depreciation has gone to pay debt and nothing is left to replace the capital stock?

The book value is also at -$56? The company would have to earn $56 before the stock has a zero book value?

Definitely long odds, but this is definitely an interesting speculation. I don’t think it will work out well, but if it does, you are right, you will make MULTIPLES on your investment.

I’ll keep an eye on it.

Looks like you understood my position. I’m not suggesting YRCW is a sure thing, or a great company waiting to be recognized or anything like that. I’m just saying that if it does work out the reward is ridiculous because of the leverage.

The other point that gets forgotten with stocks is that really, we don’t need it to work out so much as we need the appearance that it is working out for a time. YRCW does not have to turn itself around permanently to make money on the idea. I don’t want to be too focused on whether YRCW is a viable entity 5 or 10 years from now. I think its easy to get caught up treating a stock like you are actually buying the business. But you aren’t – you can sell tomorrow if its not panning out. So I’m more interested in if YRCW can be in a better position 6 or 9 months from now than they are in today. I think that is quite possible. And if they are in a better position the impact on the stock price could be substantial because of the leverage.

Keep an eye on ABFS. That is likely a better trucking company to own.

YRCW has no shot to come out of this with the stock surging. I’ve looked at them in the past, but the issue is their trucks are old and outdated. They are fuel inefficient and don’t have the money to invest in their business. They are falling further behind the rest of the industry and you can see that as their revenues continue to drop as competitors steal share.

I put together a position in ABFS as well, and its a bigger one than YRC Worldwide. No question is in a better position right now. I’m not so sure that YRCW has no shot, we’ll have to wait and see if you are right.

Lane:

I think you’ve got a good strategy here. Get in quick, get out quick. They don’t have to actually earn a lot of money, just show YOY improvement.

I’m not very good at trading, I”m going to work on improving that in the new year.

Have a happy, healthy & prosperous new year!

Hi, the stock price had surged to $28-30. And I am fairly new at this, would you tell me what I should do? Some people said it is worth a lot more.

I can’t tell you what to do but I can tell you what I have done. I sold about 1/3 of my position yesterday at around $31. Just so you know, I try to post my buys and sells on twitter because the forum there allows for quick updates more readily than the blog format. @LSigurd

So you might be right, but the path from $30 to say $100+ is not as clear to me as the one from $6 to $30 was. The move so far was a simple thesis: the company is not going to go bankrupt. The move from $30 to $100+ is going to depend on just how much earnings they can generate, how the next round of union negotiations is settled, how much market share they can take back from competitors, you can go on with a littany of questions that need answers in order to value the business… and most of these questions are harder for me to answer. Perhaps the hardest question to answer is what earnings eventually look like once the turnaround is complete. And at this price level, determining whether the company has earnings power of $4, $5, or $6 per share begins to matter, and I have always found it difficult to predict earnings at inflections.

So those are my thoughts. I sold some stock yesterday on the BB&T upgrade. I’ll probably sell more as the week goes on. It’s a lot like MGIC earlier this year, once the bankruptcy question was answered and the stock made its pop the questions that needed to be answered were with respect to profitability and the long-term business plan which for me are tougher questions, so I took down my MGIC exposure to a more suitable level given my uncertainty with the answers. I expect the same sort of pattern here.

I am very impressed with the precision of your analysis, and only using fundamental data.

Based on this I dare to ask …. 6 months later, you see this stock??

I think that can reach up to $ 300 in the 2nd or 3rd Q, but would appreciate your opinion.

Gabriel

Excellent analysis.

Regarding your below statement:

“The debt runway

Probably the most important point about the debt is that nothing significant comes due until March 2015. Between now and that time the only debt maturity is in February 2014, and that is for $69.4 million”

The company do have ABL terminate on sep, 30 2014. The ABL is also significant portion of company’s debt.

It’s interesting to see how they restructure 2014 debts?