Arkansas Best: The Upside of Union Negotiations

Arkansas Best is my second foray into the trucking world. Its discovery I owe to @Largcaptrader1 on twitter, who pointed out to me that the company may be a better way to play the industry than YRC Worldwide.

This is a much simpler investment idea than YRC Worldwide. While it took me weeks to wrap my head around all of the debt, liabilities and history of YRC Worldwide, it took me a couple days to get to the core of Arkansas Best.

But that isn’t to say that this is an easy win. The issue with Arkansas Best is singular, but it’s outcome is not easily determined. Just how well the investment plays out depends almost entirely on the outcome of negotiations with the Teamster union for the soon to be expired workers contract.

A bit of Background

Arkansas Best is a less-than-load trucker, very much a competitor of YRC Worldwide (which I wrote about the other day). Like YRC Worldwide, Arkansas Best is burdened by high costs relative to their competitors due to the high level of union employees. However unlike YRC Worldwide, Arkansas Best has been able to get by and be very marginally profitable without modifications to their employee contracts. They have an efficient operation that is mostly cash positive of an operating basis and that appears to be close to cash neutral after considering CAPEX requirements. They have far less debt than YRC Worldwide ($195 million versus 1.4 billion) and the company trades at a discount to book value ($11.55).

Union Contract History

The investment thesis here revolves around the negotiations with the Teamster union that covers about 75% of the employees of the company, including almost all of their drivers. The existing agreement that Arkansas Best has with the union is the National Master Freight Agreement, which was negotiated back in 2008 and encompassed a number of less-than-load national carriers including YRC Worldwide. It expires in March of 2013.

The existing agreement has not been without its drama. Beginning in 2008, YRC Worldwide began to experience some serious financial trouble, and it quickly became clear that they would not be able to comply with the agreement and still stay solvent. Between 2008 and November 2010, the union and YRC Worldwide made 3 separate amendments in an attempt to keep the company afloat.

The amendments were not insignificant, at one point going so far as to allow YRC Worldwide to take a one and a half year holiday from any contributions to the multi-employer pension plan. The last amendment, completed at the end of 2010, included the following: “resuming pension contributions on June 1, 2011 at a 25 percent contribution rate; revised union work rules, comprised of reduced vacation time, a flexible work week, and four-hour work classification. The deal was expected to save the company $350 million annually over its duration.

Arkansas Best tried to get its members to agree to the same conditions as YRC Worldwide but they voted it down. I was pointed to a really interesting website (again a hat tip to @largecaptrader1) where members posted their thoughts on the deal. One interesting point that can be made about the comments is that the union members seem to be more upset with their own negotiating team than with the company itself.

In addition, at one point during the YRC Worldwide negotiations the union tried to get Arkansas Best to buy YRC Worldwide, dangling the incentive of a more lenient workers contract as a carrot. Arkansas Best smartly refused to agree to this.

After the final amendment in November 2010, Arkansas Best tried to sue both YRCW Worldwide and the Teamster union for breach of the original Master Freight Agreement. That suit has been rejected a couple of times now, so I don’t know if it still has legs left.

As far as the negotiations of the new contract, this time around Arkansas Best is abandoning the Master Freight Agreement and going it alone. So far the union and the company have made opening offers, and as you might expect, they are quite far apart. The union offer is “asking ABF for $1-per hour wage increases and additional contributions to their pension, health and benefit package.”

Arkansas Best replied publicly just before Christmas. They pointed out that:

…our pension costs have escalated 40% since the 2008 NMFA was signed and are now 14 times that of non-union competitors, and two to three times higher than all other LTL carriers with Teamster contracts.

To which the union replied with this rebuttal.

I’m not going to read too much into this back and forth. Its early on in negotiations and it seems pretty standard to establish a position at the boundary and work your way in. I do think its interesting that the union admitted that “the company needs some relief”.

Relief is primarily needed from pension costs, which, as Arkansas Best noted above, are two to three times higher than other union LTL carriers. One reason that pension costs are so much higher is because the only other large remaining union LTL carrier, YRC Worldwide, has already negotiated a 25% contribution rate through to March 2015. Taking a look back at the YRC Worldwide amendment, the cost to fully pay pension contributions would have been about $360 million a year, versus the $90 million that they are now paying now. Can you imagine the losses if they were paying the same pension contribution as Arkansas Best is? They would be done.

As somewhat of an aside, the absurdity of the existing multi-employer pension structure (a topic I tackled in my post about YRC Worldwide) is highlighted by the fact that Arkansas Best pays over 50% of the pension costs to employees that have never worked a day for the company.

At the end of 2014 the legislation that governs the multi-employer pensions is coming up for renewal, so there may also be some relief when new legislation is put in place. It appears that there is a wide agreement that the current structure is not sustainable and that putting the remaining contributors into bankruptcy is not going to improve things. A number of companies are switching over to a “hybrid” pension model which limits their exposure to covering employees other than their own. I think that there is a good chance we see some pretty significant changes to the way the multi-employer pension plans are treated, and perhaps the start of this process will occur with the current negotiations.

You can see just how out of whack the pay structure is at Arkansas Best when compared to other companies. I have created a simple table of the Salaries, Wages and Benefits on a per employee basis for a number of players in the industry.

Its really quite a testament to the efficiency of the company (which the union employees should be rightly recognized for) that they can compete at all given the comparative cost structures. While I have no doubt that having a stable, experienced workforce provides benefit to the company, the difference in cost between Arkansas Best and its competitors is just too large.

What’s the angle?

I do not have any intimate knowledge about the union negotiations and whether Arkansas Best will be able to deliver a better deal. I do, however, have some comments, which are admittedly conjectures and should be considered on their own merits only.

A. The union has already capitulated on a deal to Arkansas Best’s primary union competitor (YRC Worldwide), making significant concessions, in particular on the pension front

B. Back in 2010 the union negotiators agreed with Arkansas Best to a deal that was similar to YRC Worldwide, but the members balked on it.

C. Arkansas Best should be able to achieve significant reductions simply by making changes to its multi-employer pension contributions so that they are more closely in-line with YRC Worldwide.

D. I believe that in the negotiations the multi-employer pension plans are represented separately than the union at the table because they represent different workers. Given the massive reductions that these plans accepted with YRC Worldwide, and the previous agreement that almost went through between the union and Arkansas Best, I have to wonder whether they have a weaker hand at the table?

Logic suggests to me that Arkansas Best should have the upper hand to at least get a marginally better deal than they have. But I have to admit I can’t say this with a lot of confidence, negotiations, in my experience, are like politics, difficult to predict and surprising at the most inopportune times. And a long strike could be pretty devastating to the company.

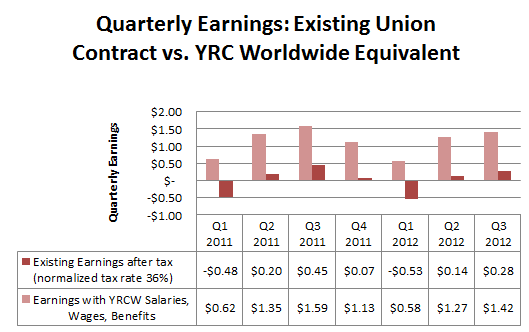

What I do know is that if Arkansas Best could get an agreement that even came close to the one YRC Worldwide has, the stock would be significantly higher than it is now. At its current price, Arkansas Best is pricing in a new contract that perpetuates the status quo, meaning little if any profitability and probably a collapse at the onset of the next recession. But if the contract were only a little bit more favorable… below is a chart that compares Arkansas Best historical earnings against what those earnings would have been if the company had salaries, wages and benefit costs that were the same as YRC Worldwide.

Note that I have normalized both the nominal and YRC Worldwide cost base earnings to a tax rate of 36%, so the numbers won’t match the reported numbers from Arkansas Best.

Honestly, I was kind of lukewarm on this whole Arkansas Best idea until I ran the numbers in the chart above. Like I said I don’t really have any particular insights about the negotiations, and the company is clearly struggling with the existing costs, and so I was about to pass but then about a week ago I sat down and made a little spreadsheet that plugged in YRC Worldwide costs per employee into the Arkansas Best income statement. I was blown away by the results.

If you give Arkansas Best the cost structure of YRC Worldwide, the stock is worth $40 easily. Now I don’t really think they are going to get that cost structure, but given the price of the stock right now (below its tangible book of $11.55 per share), it seems like a reasonable bet that they will get something better than they have right now.

Much like YRC Worldwide, this is a buy, wait and watch story. I have bought a position in the stock, actually a somewhat larger one than I have in YRC Worldwide, but still not a large enough one to do real damage if something goes wrong (ie. a strike). The size relative to YRC Worldwide reflects my confidence in the efficiency of the company to do as well as they have with the inherent constraints. Now I’m going to wait and watch the news coming out of both sides. Depending on the eventual agreement I will either be adding further or doing the cut and run. The upside here of a positive outcome is enough to justify being in the game.

I take it there bonds are privately held? I can’t find any bond data on FINRA for ABFS. I really need to know their credit rating, covenants, and bond yields to make a decision. Do you know thier yields, credit ratings and maturities? Can you please share that if you know please?

As far as I know they don’t have any bonds? Which bonds are you referring to? If they do I don’t have a good source for that data so I probably wouldn’t be much help. I tried to look into YRC Worldwide notes and my brokerages couldn’t get me them.

The only debt, I believe, was a term loan issued for the purchase of Panther. Details on the loan are on the 8-k:

http://biz.yahoo.com/e/120619/abfs8-k.html

I assume that’s why there is no information on FINRA site since it’s a term loan as opposed to a bond offering?

I’m just looking at your salary comparison now. it says in their 2011 annual report “As of December 2011, approximately 75% of ABF’s employees are covered under a five-year collective bargaining agreement with the IBT that expires on March 31, 2013.” and abfs has a total of 10800 employees, so the unionized employees number should be 8100 instead of the 10000 you have now. not sure how you would find the appropriate unionized salary number without looking in to it further, although that may be why you were using the numbers you did.

Looking at your salary comparisons now. not sure how you got the 10000 employees number, i find in the 2011 annual 10800 employees, of which 75% are under the current agreement, making 8100 total. not sure how you’d find the unionized portion of total salaries but just wanted to point that out.

If you look at page 6 of the 10-K the number of employees for ABF, which is the freight division was 10,000. That is where I got that number, and I used that number because I was trying to remove, where possible, the non-freight business. If you look at my expense item its also just for the freight division. It wasn’t easy to get that number – you have to multiply revenues for freight by the 61.3% expense they say salaries etc are