Week 79: From Chaos to Order

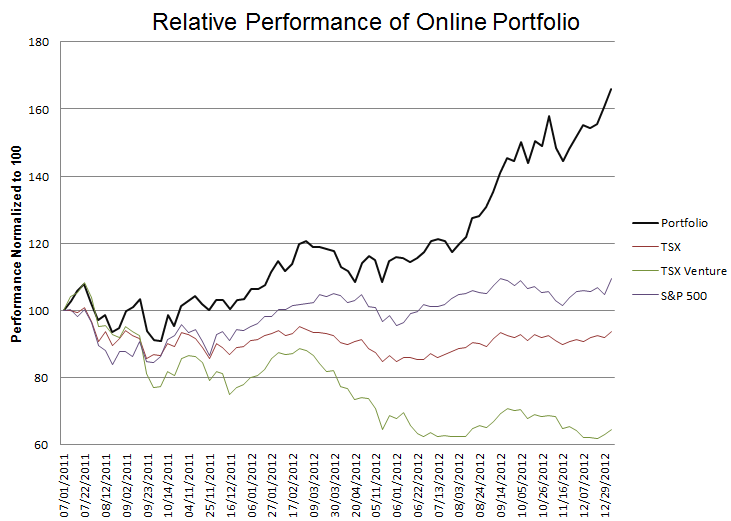

Portfolio Performance

Summary

I am going to try to keep to a shorter update but given my track record with brevity we will see how that pans out. The reason I want to keep it brief is that I am attempting to write a Visual Basic program this weekend that will allow me to paste my transactions into an excel spreadsheet and automatically spit out a list of the closed positions, the open positions, and the relevant transaction parameters. I want a better solution than a snapshot of the RBC Practice Account portfolio holdings page; I have no ability to come up with graphs and charts of performance with my current snipit method, the practice account summary has a bug that screws up the book value and gain/loss numbers every time you make a partial sale of a position, which is a real pain, and I want to be able to post a consolidated list of all my closed positions along with their gain and loss, something that is not possible from the practice account (my current method, which has been to post every one of my updates on my portfolio page, is getting to be a little too long).

On the Cliff

The market was a real yo-yo over the last couple weeks but I didn’t really panic much. I have been known to do violent purges in the midst of chaos, but not this time. I was pretty confident that something would get done, either at the deadline or as a result of the steep fall that would occur after it was passed. As it was, things turned out just about in-line with my expectations.

The one “cliff-trade” that I did make was selling out of MBIA for a couple days. My thinking, which admittedly was too cute by half, was that MBIA was not a company that would benefit much from the cliff resolution and that I would free up cash ahead of the event to put towards other stocks that came on sale. A few days later it became clear that a cliff deal was going to happen sooner rather than later and so I bought the shares back. It was a foray that amounted to a twenty cent loss and commissions.

Too Many Stocks?

I’m probably getting too many stocks in my portfolio. I’d like to have less than 15 and right now its well above that. I’m going to chalk this up to my process and this being a bit of a transition time. I have a number of mortgage related positions that are probably in their later stages of playing out (NCT, MTG, RDN, IMH) but aren’t quite to the levels where I am ready to let them go. So I’ve been actively looking for the next big thing, which is a process that inevitably leads to some chaos.

Its kind of an interesting process really and it repeats itself with consistency. As one big idea matures I go out on the lookout for another. This leads me down all sorts of avenues, and my method is that I never really know what I think about an idea until I’ve bought the stock and held it for a time. Somehow this crystallizes just how much I like it. So for a time I end up with a disparate assortment of stocks from all over the spectrum (which is what you see in my portfolio right now). As things get on it becomes clear that some of these ideas aren’t going to work and they fall by the wayside, while others do begin to work and, if I like what I see, those positions become bigger. This leads to consolidation and order, until that cycle matures and we start over again. Its just my little part in the neverending battle against entropy.

Avenex Debacle and Parkland Fuel

A friend of mine asked me to look at Avenex back in September. I didn’t know too much about the company other than that it had a really high yield and when I had looked at their oil and gas properties in the past they seemed to be one of those dart-board spatterings of low-working-interest wells in flavour of the month fields of the Western Canadian Basin. I took a closer look at the time and wrote back the following:

I think that the Elbow River business segment looks interesting. Gross Margin and cash flow are growing every quarter, and they could probably pay a lot of the current dividend from Elbow River alone right now. The AIF and one of the MD&A’s made mention that they expect to grow the oil transportation side of the business. I know from having listened to a couple of presentations from Phillips 66 that they feel that oil transportation by rail car is a growth area and they want to be expand there as well. So there is an opportunity for Avenex to grow here, and it sounds like they can do so without having to tie up too much capital. I’m not sure if I can believe the number but according to beatingthindex.com they can get their capital expenditures back in 6 months which would be quite something if true.

My concern is on the oil and gas production side. Avenex remains exposed to natural gas, its about 50% of their production, and their natural gas production is in the Western Canadian Sedimentary basin where natural gas prices remain even more depressed than Henry Hub. AECO is still barely above $2/mcf even now. I don’t see a lot of upside from the oil and gas side until gas prices improve.

I’m not sure they can maintain current production levels (~4,000boe/d) with the amount of CAPEX they plan on spending. They said in one of the reports I read that they were going to limit oil and gas spending to be within the cash flow limits from that segment less dividend requirements. Cash flow from the segment was a little over $8 million in the second quarter before accounting for the contribution of G&A and interest payments, and the contribution to the dividend of the segment is probably around $2 million range. That doesn’t leave much for CAPEX. Spending $4 million or so a quarter on new wells is not a lot. A single horizontal multi-frac well is going to cost that much. I really doubt they can maintain 4,000 boe/d with that kind of spending. I also suspect that their mature, more stable production base is the gas production. I bet if they don’t spend money the oil side is going to see a hit as those new Cardium and Slave Point wells decline.

So I was less than enthused at the time, but a month later I had come around as I really saw potential from the oil-on-rails story. I imagined a Pason/Open Range sort of story (the upside part of it that is), where Avenex spins off Elbow River and the business gets revalued based on its growth potential.

Well that bubble was burst on December 20th when Avenex announced that they were selling Elbow River and merging with two other oil and gas companies.

I haven’t really looked that closely at the combined entity. I sold Avenex the morning of, almost immediately after I read the news. My thinking, as I summed up to that same friend: “Once the play is over I have found its best to get out. Otherwise I end up spending emotional capital waiting and worrying about a better price. Its over, I lose, move on.”

I did, however, also buy Parkland Fuel. There wasn’t a lot of deep analysis to that purchase, simply the logical thought that if this company was worth $18.50 before it purchased Elbow River for what I deemed to be a fire sale price, then it was probably worth somewhat more with Elbow River in the mix. I have since done quite a bit of work on the name, and I still like it. I don’t love it, but I like it. What I don’t love about it is that Elbow River is not as big of a part of the company as it was with Avenex. EBITDA was $60 million last quarter and they should be able to add another $7-$8 million from Elbow. The rest of the business revolves around retail and commercial fuel distribution which is pretty low margin, but appears to be unconsolidated here in Canada. So there is a chance that the company can be the consolidator, the Elbow River transaction suggests they are astute enough to take advantage of opportunities. I talked with IR and they are going to let Elbow River operate on their own, but will be available to provide capital to the business for growth. We’ll have to see how it turns out

Another spec play: Niko Resources

I often have to brush off the feeling that a stock is a spec situation and could go either way because the truth is I pretty much invest in nothing but companies that fit this profile. To turn the coin around, if the outcome was more certain, there probably wouldn’t be much of an opportunity. Niko is a spec play, actually brought up to me by the same fellow that brought up Avenex. It used to be a $100 stock. The company has a 10% working interest in a block of natural gas production in India. It has been a real disappointment, reserves were cut more than in half last year as the production failed to live up to the initial geological interpretation and production is falling. The stock has fallen too: this was a $100 stock two years ago.

There are two plays on this one. First, the consortium has a signed contract to sell gas in India at a little over $4/mcf. That contract expires in March 2014. Right now LNG imports into India are in the double digits, whereas at the time the original contract was signed (2007) they were floating around the $4 mark. I ran the numbers on an $8-$12/mcf contract price and there is a lot of cash flow to be had, even with the declining production. I think its also likely that the group, which owns an extremely large block of land compared to what has currently been explored, steps up exploration once the contract is signed. There was an interesting article in the Hindu Times that reported that a government appointed Advisory Council made recommendations that would lead to a much higher contract price going forward.

Second, the company is expected to drill a number of exploration wells in the coming months. If one of them hits…. of course that is the commonly phrased if, if, if that one hears in these international exploration companies. I’ve been down that road before, most recently with Pan Orient and their continuing adventures in Indonesia, and its painful to watch the cash burn on failed exploration. Nevertheless, as I wait for positive news to be released on the contract, I will keep my fingers crossed that something good happens.

Niko really deserves a full post to explain the idea well, and fortunately I don’t have to write one. There was an absolutely excellent post, followed by an equally excellent discussion, about Niko on the UK Motley Fool board. It gives a very balanced appraisal of the company, including all the negatives. On the same board there is another comment on the gas contract negotiation that is well worth reading.

Other stocks I’m looking at

I also bought a small position in Comverse Inc(CNSI) off of a twitter write-up that was done by @mojoris1977 but until I get the time to understand the company better I will leave the position small and my comments to this. I bought a small position in Atlantic Coast Financial, which is a tiny ($5 million market cap) bank in Jacksonville Florida that I am sure I will get emails telling me how crazy I am to buy, but which trades at about 15% of its tangible book and peaked my interest again after another bank in Jacksonville (Jacksonville Bancorp (JAXB)) that appears to me to be in worse straits than Atlantic Coast, announced that they were able to find financing that will put some much needed capital into the company. yeah, I know, spec play. And of course I now own Arkansas Best and YRC Worldwide, which I have already written about extensively and of which there is not much more to say.

I’ve been using twitter to communicate some of the interesting ideas I read about and some of the stocks I’m looking at, and while I’m not going to start posting a play-by play of my trades on there I do guarantee that you will read about the ideas more quickly if you follow me there rather than here. I’m @LSigurd. As I’ve mentioned there, I’ve been looking at a couple of asset managers that are buying single family homes in the US for rental purposes; Tricon capital (TCN.to), Silver Bay Realty (SBY) and Altisource Residential (RESI). I’ve started to look at Pan Orient (POE.v) again, though it kind of got away from me in the last couple days and I am reluctant to chase it. And on another twitter recommendation I am looking at API Technologies (ATNY). I also have a number of gold stocks on my radar; I took a small position in Brigus Gold (BRD) and briefly had one in Mirasol Resources (MRZ.v). I’d really like to get back into the gold sector at some point, but picking a bottom is tough.

Portfolio Composition

Click here for the past three weeks of trades.

{kind=link}

The Altisource spins offs are very complicated. I hope you also analyse RESI’s service provider AAMC to see if maybe that would be the better value. It seems to me like AAMC will be paid very handsomely if RESI is successful (however, already up ~50% since IPO). Or maybe the old ASPS is the best value right now. Great Blog

Thanks for that. I haven’t really done enough work to comment yet but I’ll keep the relationship in mind as I look at it.

Lane – you and I have talked RESI/AAMC before. My thoughts are that AAMC is nicely levered to any growth in RESI AUM. It’s pricy now based on RESI putting just $80m to work (assuming some leverage too), but if they raise more capital or AAMC can provide their services to other capital pools, it could work out very well.

Thanks for the comment – yeah I need to take a look at these companies. i haven’t gotten back to you because I haven’t had enough time to comment intelligently.

AAMC is also going to manage NewSource for management fees. Not much info on NewSource however. Erbey has created a very complex structure of companies. So either he’s very methodical about efficiently allocating capital like Malone at Liberty, or it’s complicated so that money can be siphoned off from shareholders. I haven’t been able to come to a conclusion as of yet. Still looking at it though.

NewSource being the title insurance JV that will be capitalized to the tune of $20m – $18m in non-voting interest coming from RESI, $2m and voting control coming from AAMC. I haven’t completely figured out how NewSource plays into the situation, but it looks like another fee generator for AAMC.

Looks like NewSource will pay 840k in fees to AAMC at the start. As it’s a fixed amount this will be very substantial while RESI is still growing. Although as you stated, most of the NewSource capital is coming from RESI so we have to be careful not the double count the fees.