2012 Recap

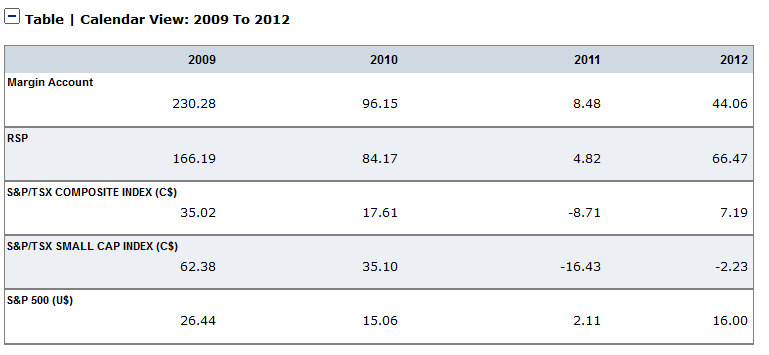

Below are the results for 2012 from my actual portfolios. My bank does a good job of providing performance analysis; its improved to the point that I may start to track my actual portfolio directly rather than through a practice account. The results available from the service go back to 2009.

In 2012 I managed to outperform the S&P and the TSX and I’m pretty happy with that. I’ve commented before on my time constraints. I work a day job so my time to analyze investments is mostly limited to a few early morning hours, an hour at lunch and sometimes (when I’m not too tired) an hour before bed. While my hope is that this will eventually change, right now time limits me from investigating every possibility and often causes me to get to ideas much later than I would otherwise.

In order to maximize efficiency I try to come up with a few big ideas that I can leverage a number of investments from. Last year those ideas were:

- Mortgage Servicing Rights

- Mortgage insurers

- Small community banks

- Gold stocks that have gotten ridiculously cheap

The first three ideas worked out very well. As for gold stocks, I had some success (OceanaGold, Atna Resources, and Esperenza Resources) but I also spent a disproportionate amount of time and energy on the sector. Picking gold stocks is a tough gig.

Next up is performance on a quarterly basis.

I have proven myself to be much more able to outperform when the market as a whole was doing well. It reminds me of when I looked at the past performance of the magic formula investing strategy, the strategy proposed by Joel Greenblatt (which has a similar kind of under-the-radar value approach to what I try to accomplish). It has a similar distribution.

I think that the reason for the under-performance in bad times is that under-the-radar stocks don’t typically have strong institutional support and so they tend to perform poorly when the market gets fearful and retail investors flee. This is even though the businesses themselves may be better suited to a downturn than most.

The other aspect is that I have a hard time figuring out macro. Its much easier for me to understand a business than a country. My only strategy for handling macro uncertainty that has worked has been to admit my ignorance and get small. This can be tough because you end up getting rid of perfectly good positions for no company specific reason. And you lose out – to give an example, the profits I lost on Coastal Energy in 2011 because I couldn’t bring myself to put together a large position in the uncertain macro environment. Had it not been for the problems in Europe and my worry that everything was about to implode, Coastal at $5 or $6 would have been a 15% position easily. As it was it never got to 5%.

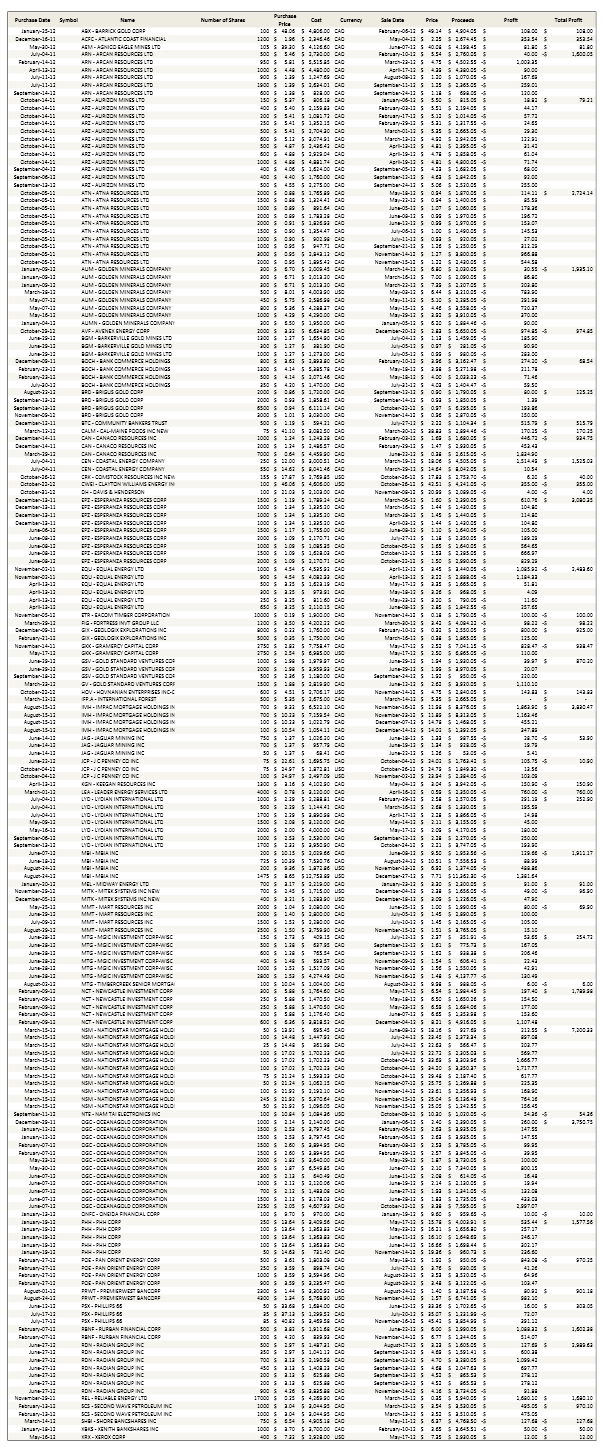

Finally, here are the closed positions in 2012 (from the practice portfolio). I put this together from the little visual basic program I wrote that takes raw transactions and converts them to open and close positions – I’m quite happy I was able to build this in the last week. I’ve sorted these by company because I think it is interesting to note which companies I did well with and which I did not. Of course some of the companies, like Impac Mortgage and MGIC, have a lot of unbooked profits in the remaining open positions, so you can’t just take the closed book as a summation of the year. Still, it is interesting to reflect on.

One thing that surprised me when I looked at this list was just how well I did on my gold stocks. OceanaGold, Esperenza Resources, Atna Resources, Geologix, Gold Standard Ventures, all of these names had significant gains. I think that one trick with gold stocks is to get out as soon as the story appears to not be playing out the way you expect. I avoided significant losses in Canaco, Jaguar Mining, Aurizon Mining and even of all companies Barrick by cutting my losses before they got out of hand.

Also, Equal Energy and Golden Minerals have been recurring disasters. There are some stocks that appear enticing but that you just can’t seem to win on. These two qualify and I think my best course of action in the future will be to stay away entirely.

The last observation that I will make is how many losing trades I had this year. Even though it was a profitable year, my win/loss ratio was pretty close to 1:1. And I don’t think this is a bad thing. It exemplifies an important part of my strategy and one that is one of the hardest things to do. Cut my losses. When a stock goes south I don’t want to be held by the feeling that I have to hold it until I am proven right, even though the impulsion to do so is inevitable. Better to be a Buddhist; practice non-attachment and walk away when things are not going well. That has been the most important thought for me to hold in years past and I expect it will be so again in the year ahead.

Great Job! Outperforming The Herd Fund “Titans”!!

What are you looking at in 2013? Any dividend stocks?

The two areas I’ve been looking at are trucking and autos, in particular parts manufacturers (had a friend rec AXL which I think looks pretty interesting). I also think that 2013 could be good for the insurers (RDN and MTG)

Your blog and twitter account has become one I follow regularly. Thanks for the great ideas.

Woah, huge drop in IMH today! Wonder what that is about…

The theme that has been going around is that the refi boom is about to end and volumes will of course suffer. I think it will be interesting to see what volumes settle at with Impac. Are they are refi flash in the pan or have they taken market share away from smaller brokers that have left industry in the last few years and from larger banks getting out of correspondent. I’m still of the mind they are creating a franchise here and you are seeing expansion to the east in job postings and recent VP appointments.

Full disclosure: as I tweeted last week I took off about 25% of my position once we passed into new year. Nothing to do with the company, my position was simply too large for my liking because of gains and I had been waiting until new year to sell to avoid taxes for a year.

I read your mortage servicing rights analysis “Pounding the table on Mortage Servicing Rights” several times before I decided that it was rock solid research. I am a real estate property investor on the side, with a day job, just as you are. I then read everything on Newcastle’s website for investors before I went all in on NCT. I also considered the synergy generated as part of the Fortress Investment Group, which is focused on unlocking shareholder value and have been rewarded beyond my expectations. I am up 50%, and continue to hold the stock because of the upcoming split into two corporations, and the continuing strong management of both entities.

That’s great! Yeah, NCT has been a big winner for me, more than a double now. I have no plans to sell any until they complete the spin-off.