An Appreciation of Comverse

One of my new sources of ideas and opinions has been twitter. I’ve found a bunch of people on there who provide insights and from whom I have been able to learn and garner new investment ideas. While twitter has its drawbacks (for one it is difficult to hold a long conversation) it’s a great place full of investors, traders and fund managers that I would otherwise not have access to.

One fellow who I follow goes by the moniker @mojoris1977 and the name Jim Morrison. He has had a number of successful recommendations, but I hadn’t followed him into any of them until around the middle of December when he recommended a company called Comverse Inc. Shortly after the recommendation I bought a small position after just a little background diligence, but since then I have looked a more closely at the company and turned my position into a more significant one.

Having gotten the idea from someone who has proven to be quite astute, I approached my research from a somewhat different angle than I usually do. Rather than coming at it from the is-this-company-worth-looking-at-any-further angle I came at it from what’s-the-story-I’m-missing angle.

The Story

It wasn’t obvious at first glance. You take a look at the Comverse balance sheet and you see negative book value. You take a look at the income statement and you see barely break-even earnings. You take a look at the history and you see a prior accounting scandal related to the back dating of stock options and pre-spin-off financials that are mixed together with the holding company’s majority ownership in Verint. Add to that a somewhat hard to understand business, and an equally hard to understand (CEO (because of his French accent) and you have a whole bunch of reasons to stop looking.

But if you do look a bit closer, the story becomes more clear. The negative book is mostly because of a deferred revenue liability and not because of debt (of which the company has none). The company has significant cash on the balance sheet. They had $233 million of cash at the end of October and on the conference call in mid-December said they expected that they would end the year with $280 million of cash, another $25 million in escrow and $11 million tax refund that are both expected in the first half of 2013. That works out to a little over $14 per share.

The less than stellar income statement is partly the work of restructuring charges associated with the severing of ties with the parent but mostly the result of out-sized SG&A which appears to be mostly related to the previous holding company structure.

On the Q3 conference call management said that one of their primary objectives over the coming months is a rationalization of SG&A. Their original target had been to achieve cost savings of $35 million to $40 million, but upon closer investigation they felt they could even exceed that amount.

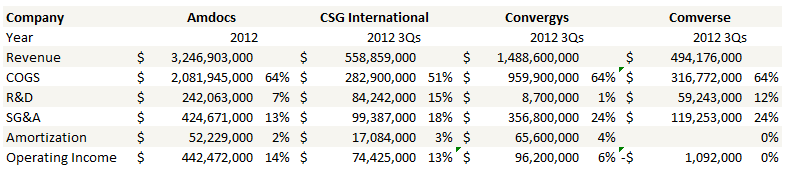

To help put that goal into perspective,the company has about 22 million shares outstanding, so they are suggesting that they can improve their operating margin by nearly $2 per share simply through SG&A improvements.

I took a look at some of their competitors. Below is Comverse and three other companies in the space. A $40 million reduction would put Comverse right between Amdocs and CSG on a percentage of revenue basis.

On the second quarter conference call for the parent Comverse Technology (CTI), I interpreted CTI management to have said that the Comverse Inc. sub incurred about $30 million related to the holding company structure. Now the way it was said was not perfectly clear, so I might be wrong, but if I understood the comment correctly a big part of the cost reduction should be achievable by simply eliminating the holding company related costs.

The Business – BSS

In addition the company is expecting improvement in its business segments. Each of the businesses revolve around products provided to communications service providers (CSPs).

First, Comverse provides business support systems (BSS). This is really a catch-all term to describe the business of managing customers billing. In its simplest form Comverse handles the basic billing mechanics, and they have a couple legacy post-paid and prepaid products for handling that. What’s happened over the last few years though, is that with the complexity of offerings and packages available, the role of billing has grown to be more of a customer management business. Comverse’s new product offering, which is called Comverse ONE, provides functionality for managing and analyzing customer usage, matching product offerings to customers based on usage and identifying new package alternatives that would more effectively capture revenue.

In the 10-K the company describes the value proposition of Comverse ONE as follows:

The Comverse ONE Billing and Active Customer Management solution provides comprehensive BSS functionality, including real-time rating, charging, promotions and session control for both prepaid and postpaid subscribers, mediation and content partner settlements, roaming support, sales force automation, campaign management, case and interaction management, customer self-service and order management, and converged billing for hybrid prepaid/postpaid wireless and triple play/quad play (wireless/wireline telephone/Internet/TV) services.

Real-time rating, charging and account re-charging capabilities are particularly valuable to service providers, to reduce revenue loss by ensuring that prepaid subscribers do not exceed their account balances and postpaid subscribers do not exceed credit limits, and to promote continuous revenue generation by providing user-friendly tools for end user balance awareness and account replenishment. These and other end user self-service features give subscribers greater control over their accounts, services and applications, increase service provider revenue and end user satisfaction, and reduce the costs associated with network operator-assisted service.

It sounds like the Comverse ONE product is top of the line for this next generation BSS. Comverse was named by Gartner as one of the premium providers of services in a report release last summer. Last February Frost and Sullivan, another business research firm, awarded Comverse for their “forward looking strategy” of providing a more complete billing solution.

As a whole the BSS business is expected to grow at a 3-5% rate over the long-term, which isn’t terribly exciting. But if you separate the traditional BSS business, which is the simple post-paid and pre-paid products, and the new integrated product offering that Comverse has, you get a different picture. The company said on various calls that the next generation offerings are expected to grow “much faster” and at “many times” that of the traditional business. Comverse currently has ~110 customers on the old generation pre-paid/post-paid products and 30 signed up for the new Comverse One, so there is plenty of room for upgrade.

On a purely qualitative note, the BSS space and the Comverse ONE product offering make a lot of sense to me. Providing CSP’s with the functionality to create payment streams based on usage and to provide a service centered around compiling and analyzing user data to help with those decisions is a good approach to tackling the competitive pressures from non-CSP service providers. I like the outlook here.

VAS

The second business Comverse operates provides CSP’s products such as voice messaging, text messaging and, more recently, third-party interfacing platforms (middleware). They bundle these offerings into a segment called “Value Added Services” or VAS. Comverse is a industry leader in VAS, particularly on the voice side, and have recently been recognized as the number one firm in the business by Frost and Sullivan:

Ronald Gruia, principal analyst for Frost & Sullivan’s ICT Practice, said it is a significant achievement in a crowded field that is in constant flux. “Comverse is further distinguished as the only company to place in the top two in all three VAS segments: voice, text and multimedia messaging. In contrast, no other company was able to accomplish a top-two ranking in more than a single segment,” he said.

While VAS is a solid gross margin business, I am less enthused about its prospects than I am of BSS. Comverse already has a large market share, and the sector is facing some headwinds.

The VAS business is in direct competition with what is called over-the-top (OTT) content providers. OTT content is delivered by a party outside of the service provider. The Economist had a good article summarizing the competition here, and describes OTT as follows:

OTT services can take many forms, but voice and message apps have been the operators’ biggest headache. Rather than pay for an SMS message or a phone call, people may use Skype (bought by Microsoft last year), WhatsApp (brainchild of two alumni of Yahoo!), Rebtel (a Swedish start-up), Viber, Voxer or some other upstart to send messages and videos or make VOIP calls for nothing. They may still incur data charges but with Wi-Fi access may avoid even those. Ovum, a consultancy, has estimated that OTT messaging cost operators $13.9 billion, or 9% of message revenue, last year.

The article pointed to the decline in voice and text messaging, and I thought this graph of annual revenue growth for CSP’s from text messaging that they provided was worth considering:

I found some other good articles on the struggles of CSP’s with OTT here, here, and here.

On the bright side (for Comverse), the rise of OTT is exactly the reason that CSP’s need a BSS solution like Comverse ONE; so they can track and bill users for their bandwidth even if the application resides outside of the CSP’s grasp. So there is a built-in hedge. And the argument could be made in return that when it comes right down to it, the CSP’s own the gateway and so they hold trump.

While so far this year margins in VAS have been up slightly up from last year (which is probably attributable to the company’s strategy to go after high margin business), revenue is down for a second year (also attributable to the strategy), albeit at a decreasing rate when compared to the prior years decline. VAS revenue declined 23% from 2010 to 2011 compared to being down only a small amount this year. So it may be that the worst of the VAS declines are behind Comverse, but its equally possible that the company will continue to see headwinds as the struggle between VAS and OTT plays out. I suspect that this uncertainty is why, when you listen to the last couple of conference calls with new management, they are noticeably more vague about the growth expectations of VAS than they are of BSS. In the CTI 10-K risks factors the following risk was cited:

Currently, we are unable to predict whether increases in BSS revenue, if any, will exceed or fully offset declines in VAS revenue. If BSS revenue does not increase, or if increases in BSS revenue do not exceed or fully offset declines in VAS revenue, Comverse’s revenue, profitability and cash flows would likely be materially adversely affected.

Comverse has a fairly new product (VAS 3.0 which was released last year) that is focused on higher margin content like video messaging and IP communications and providing the “middleware” for cloud based services. It could drive the top line at least somewhat bit higher. The company also says there is some opportunity to improve margins in the business as they move to more cloud based offerings. I’m not sure how much more fat there is to be trimmed since the segment already went through a pretty significant restructuring in 2011.

Managed Services

The third and smaller segment that the company operates is providing service and maintenance to their own product lines (so to BSS and VAS). They see a growth opportunity here. Right now this segment is about $15 million in revenue per year, but they think they have the opportunity to grow it to $120 million over the next 3 years. The managed services business has a lower gross margin than BSS or VAS (about 30%) but higher operating margins (about 20%). If they can accomplish their goal you are looking at another $20 million of operating income.

What it means to Earnings

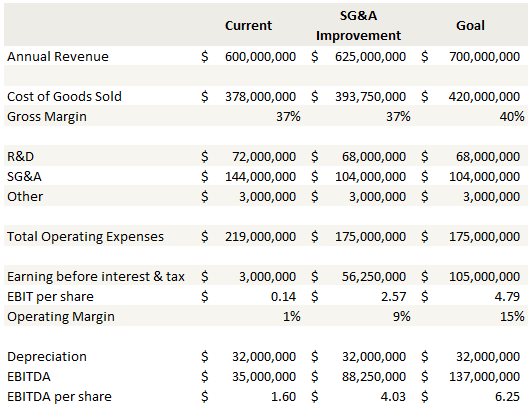

If the company can achieve the SG&A reduction, improve their revenue run rate and increase the operating margin into the mid-teens (which is basically the plan), we are probably looking at EBIT close to $5 and EBITDA well over $6.

Below I have roughed out the current run rate and two scenarios. The first scenario assumes no improvement in bookings, no improvement in gross margins and only a small improvement from Managed Services; all the bottomline benefit comes from a reduction of SG&A and a slight reduction in R&D. The third scenario is the “goal”; SG&A and R&D efficiencies are joined by an improvement in gross margins and growth in revenues which, at $100 million,implies either no growth to BSS and VAS or only partial success of the goal to grow maintenance revenues from $20 million to $120 million.

(Note that in the current case I am ignoring deferred revenues and have scaled all expenses as a percentage of revenue, which I believe should discount the impact of the deferred revenue to both the top and bottom line).

The company retains an net operating loss carryforward of the parent which amounts to a rather staggering $659 million at the Federal level and an unstated but presumably smaller amount at the state level. The company suggested that tax rates in most of its operating area will be limited to the level of the withholding tax, which is in the 10-15% range. Its difficult to say what the overall tax rate is going to be, but given a nominal tax rate of around 40% offset by some areas where the tax rate is only 10-15% it shouldn’t be too high. Maybe in the neighbourhood of 20-25% overall as a rough guess?

In addition, maintenance capital expenditures are relatively low, based on management estimates on one of the calls they are probably around the $15 million range annually, so a large portion of EBITDA translates into free cash flow.

If the company struggles with these initiatives, there is always the option of selling out. While part of the parent, CTI put the BSS and VAS businesses on the block in 2011 and received interest from Amdocs and Oracle. That could be the fall-back plan this time around.

The bottom line is that if management can accomplish its cost reductions, resize the staff and equipment to the business, show stabilization of revenues from VAS and a bit of growth from BSS in the latter half of the year, the shares should trade higher, perhaps to $50, and higher if they can improve on gross margins and show sustained top line growth. All of this is going to play out in the next number of quarters, the SG&A rationalization is supposed to be complete in 18 months, so we shouldn’t have to wait too long for some results. If it doesn’t pan out, if either the cost reductions don’t come through or if more significant deterioration occurs in the VAS business, the stock trades back down into the mid-20’s, but with the cash margin its hard to see it going much lower than that. Weighing those pro’s and cons it seems to make for a solid risk/reward even at current levels (~$30).

Check out p.88 of the recent Q. Says they have a pretty sizeable NOL with CTI. I think greater than Mkt cap and total EV. Is that how you read it? Think this is where the RMT issues comes into play…

Yeah I have to admit I don’t understand how the RMT plays into it and what the limitations on use of NOLs end up being but the company did say on the Q3 call that taxes would be lower in the operating regions where they had the NOL so they are going to get a benefit. They said they will quantify that benefit when they give 2013 guidance on at fiscal year end.

views on spinoff?

Is this back on your radar now that it is in the mid 20’s and Becker Drapkin has a board seat and is a large buyer at these prices?

It was before Q1 was released but I stepped thru Q4 results and listened to the Q4 call and it was just so dismal it was impossible for me to get excited about it. I didn’t listen and spend any time on Q1 yet. Is there any improvement?

Becker Drapkin got my attention. Their average return on the last 11 13d’s with a board seat is 114%. (Barron’s march 22). Drapkin just bought 2m more in stock. I was reading your posts and VIC write up to get up to speed on co. Just above 52-wk low. Still have to listen to the most recent cc to get a feel for which direction cost savings & revs are headed. Also want to see if they’ve done anything with $30m buyback authorization.

I think the recent pop was bc of Drapkin buying at the lows. I’m doing more work this weekend.

I was reading on your blog posts and the VIC writeup first to get up to speed then Cc’s tomorrow. Did some poking around on Drapkin Becker and the last 11 13d’s with a board seat yielded average return in 114%. (Barron’s march 22). That’s what really hit my attention plus know you and mojo had been sniffing around. Drapkin just bought another 2.3m near the lows. Probably caused the pop

this comment got caught in the spam. Just caught in now.