MGIC: Is Something out of Whack?

MGIC has really taken it on the chin over the last couple of days. While I can’t speak to the cause of the move down on Thursday, the fall on Friday, which was followed by further pressure in after hours trading, was precipitated by a note from Macquarie analyst jasper Burch.

Burch called MGIC’s valuation “out of whack”, cited earnings and book value pressure, and suggested that there was “an outside chance” that the regulators might “pull the plug”.

I found the comments surprising.

First, I don’t think his regulator comment is consistent with MGIC’s disclosure (from the SeekingAlpha transcript).

We regularly provide updates to both the GSEs and the OCI of our expectations regarding our capital position and as a result this quarter’s results including the risk to capital ratio are not a surprise to them. The GSEs and the OCI understand that our forecast calls for the risk to capital ratio of Magic to continue to rise for some time to come. The exact timing of when it will begin to decline is subject to among other things, the level of new notices and cures, the amount of new insurance written to Magic and the outcome of dispute resolutions.

I can’t imagine a regulator telling MGIC to close up shop at this point. For the regulator to come in and say: “you know we realize that you’ve settled your issues with Freddie, we can see that your cure ratio approached 100% in the 3 toughest months of the year, we know that house prices are recovering and that you guys are writing some of the safest and most profitable business ever, but we’re sorry, you guys are done.”

I find it very hard to believe that would happen.

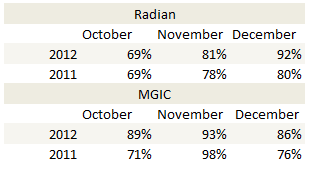

MGIC struggled with cure rates over the summer months but they have been putting up some very strong numbers since October. Below are the cure ratios (which is the ratio of new delinquencies to cured existing delinquencies) for October, November and December, compared against the same data in 2011 and compared against Radian. The December quarter excludes 941 delinquencies that “cured” because they reached their aggregate loss limit.

Regarding comments about the risk to capital ratio, I think there is a real misconception here on how the regulators are looking at the mortgage insurers. On the third quarter conference call MGIC went to lengths to describe that it was not risk to capital that the regulator was looking at and that it was claims paying resources that mattered. MGIC admitted that risk to cap would keep going up for another 2 years but that claims paying resources were going to remain well above $1 billion even under stressed scenario.

So while risk to capital will continue to rise for some period of time, I want to emphasize the fact that we believe there is no liquidity issue at the insurance operations, and we have paid over $10.5 billion in claims since 2007.

…We have a significant level of excess claims paying ability at MGIC. That is, the sources of plain paying resources, namely cash and investments plus future premiums from the existing and in-force portfolio comfortably exceed the level of expected claim payments even with reasonably adverse outcomes and various legal contingencies. Furthermore we believe that we have sufficient claim paying resources to meet all obligations to policy holders, even under a stress-loss scenario.

In my post Does Radian Guaranty have a Liquidity Problem I ran through an analysis of Radian Guaranty’s claim paying resources and concluded that as long as Radian keeps writing new business they will have more than sufficient capital to stay above their minimum requirements, and that is even if the Radian Assurance cash remains mostly unavailable. A friend of mine took my work and ran through the same analysis with MGIC. The result showed clearly that MGIC had more than enough claims paying resources to make it under even reasonbly stressed scenarios that were more taxing than the way the housing market is currently playing out (for example one key assumption was year over year delinquency declines of 15% for the next 3 years, whereas the third and fourth quarter delinquency declines were over 20%)

Now this is purely my opinion, and I’m not directing this at anyone in particular so much as to the general perspective of the industry, but I think the focus on risk-to-capital is because its a single number metric, and doesn’t require the rather complex assumptions that are needed to actually run out the business over a number of years and look at the cash coming in and going out. Fortunately the regulators seem to be aware that risk to capital is not, in and of itself, the all-telling metric of the mortgage insurance business, as both MGIC and Radian have explained that their regulators make decisions by forecasting out the book of business under different scenarios.

And what seems to never be considered is that its in the regulators best interests to keep MGIC writing new business. The best way to insure that MGIC has the cash to pay out claims on their legacy book of business is to have them write new business. Limiting new business accomplishes nothing.

At the end of the third quarter my concern was that MGIC’s cure rate was stubbornly low. That changed over the last 3 months and things are looking much more favorable now. If the cure rate can stay at these levels on a seasonally adjusted basis we are looking at much better cash flow metrics at the subsidiary level. If delinquencies continue to decline at 20% and there is no further revaluation of reserves to the existing book, earnings may turn positive quite soon.

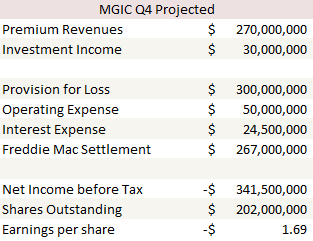

The one thing I do agree with Macquarie on is that Q4 EPS is going to be ugly. That is mostly due to the Freddie Mac settlement. Below is my own estimate, which quite by chance matched exactly what Macquarie is looking for.

Nevertheless, the market is forward looking. So while there is no question that the fourth quarter is going to have a big loss because of Freddie Mac, I think that the market is going to look past that, particularly if the delinquency numbers for January are as good as the past 3 months. Reducing the company to under-perform just at the time that they are turning the corner to better results made very little sense to me. I will continue to hold my shares.

I’m having a hard time finding a definitive earnings release date for 4th quarter results. Nasdaq says Jan 28th, others Jan 31st and yet others Jan 24th.. Called investor relations yesterday but no call back..

I don’t know when they plan to release earnings but I’d be surprised if its before the second week in February. I mean if I was the company I would certainly want to time earnings with the release of January operating stats. A positive January (which I’m really hopeful will be the case) could overshadow the hit to book and earnings from the Freddie settlement.

Good point on the timing… But holding off the extra two weeks could really bring some grinding losses to the stock value. Hopefully…

How did january’s look in your opinion?

I thought they were fine. Didn’t blow me away but were fine. Radian jan numbers sounded very good. Said on CC that cure ratio was 109% in January.

A total noob question here. It looks like it is inevitable that MGIC hit’s negative book before earnings turn around. Is it reasonable to assume that they will be allowed to continue to write insurance with no book value?

Yeah so that is related to what I was trying to explain in the post. The regulators aren’t going to look at book value when they are evaluating the company. They are going to look at whether the cash and investment resources, and the premiums coming in from existing and new insurance, are going to be enough to cover the claims under stressed scenarios. The model I describe in the post, and the one that I posted for Radian, goes through that analysis and it shows that MGIC has more than enough capital to cover claims even under stressed scenarios.

January’s numbers were posted on friday.

Progressively better every month… Delinquencies still evaporating, new business written was almost double a year ago’s number and cures solid. Thursday morning we get earnings which will show the settlement so to me any hit the stock takes for that charge would be a chance to add to position.

January 2013

Primary New Insurance Written ($Billions)

$2.2

Beginning Primary Delinquent Inventory (# of loans)

139,845

Plus: New Notices

11,098

Less: Cures (1)

9,627

Less: Paids (including those charged to a deductible or captive)

3,248

Less: Rescissions and Denials (2)

221

Ending Primary Delinquent Inventory (# of loans)

137,847