Is the Gain on Sale Boom over?

Earlier this week my portfolio was rolling along nicely, having closed at an all-time high on Wednesday night with me looking forward to further gains ahead.

And then Flagstar reported their fourth quarter results.

I don’t own Flagstar. I don’t even follow Flagstar. They are a Michigan based bank that has had some problems in their past and, most importantly for this discussion, run a reasonably large sized mortgage operation. In the fourth quarter Flagstar reported a big decline in their gain on sale margin, from 244 basis points to 153, and the Street took it to mean that the mortgage origination boom was over. In addition to the carnage of Flagstar (down about $2.50 to $15.57 on Thursday), PHH Corp, Impact Mortgage and Nationstar all took it on the chin.

But while the headline decline was steep, there is more to the story. During the conference call Flagstar provided some clarity. The following exchange between Matthew Kerin, the president of the Mortgage banking division, and Paul Miller of FBR is instructive (via SeekingAlpha).

…there is a lot of confusion out there, and I think it’s driving the stock price today on your gain on sale margins. Now, I think the confusion, it doesn’t necessarily lie under 153, but it’s really going back to the gain on sale margins of last quarter, what exactly drove that 244 to be so high, and can you add some color to that. And then also can you add any color on what you are seeing right now, is there interest rate locks up today, it seems like December was abnormally spike down?

Michael J. Tierney

I mean look, if I went back on it, as we all know the industry benefited in the second and third quarter as mortgage yields had a pretty steady decline on a 100 basis points or so, and we all had the opportunity to enjoy higher margins, and then pretty strong volumes. In the fourth quarter obviously yields increase in a roughly 18-20 bps and that did have some impact on our overall margin.

Some of the factors that impacted the fourth quarter, I think you saw, our lot of volume was down, and that was consciously done as we look at where originations and kind of focusing on where our production was coming from and some tweaking or just some pause, if you will to assess and confirm and validate to our board and others, where our business and the type of business we are doing.

There are a number of other things that impacted the margins and December in particular we had the December Fannie GP increase, it took effect and that had a tempering influence on some of the wider margins that has been available for our said GP increase. Part of our origination, development activities, we had benefited from some previous high balanced full transactions, that had some spread widening impact in the mid November at the loans and the yields, and impacted our execution in that space in December.

Overall December was a little bit of reduced supply of premium coupon spec tools and that impacted some of our ability to make volatility, get higher pay ups and yields, let’s say flattened out. We also had a loan different mix in our production volume, as you know the FHA introduced their insurance premium increase, and that just closed out of the market, and we’re a big FHA player, so they were just a number of things that impacted that overall execution premium that we are contributing as well as our own kind of predetermined pooling activities based on the originations that we were developing.

I do want to reiterate that our based production margin as we remained steady, and pretty strong over the course of time…

Miller went on to do his best to get clarification on the point that base margins are only down marginally.

Paul J. Miller – FBR Capital Markets

But this base margin right? Getting to the core of the profitability, so this base margin remains relative constant over the last couple of quarters?

Michael J. Tierney

Yeah, I mean it was down modestly in December obviously as a result of deals moving, but no it’s been very consistent. We were above 145 for the year, I guess and probably slightly higher than that for the fourth quarter, and slightly higher than that for the third quarter.

Paul J. Miller – FBR Capital Markets

And what about today, like in the first couple of weeks of 2013, is that base margin holding in there pretty solidly.

Michael J. Tierney

Let me say this without making any forward-looking comments, I think that we’ve been consistently pretty good indicated where the market is, and I would suggest that that’s still true.

Paul J. Miller – FBR Capital Markets

So, you are looking at, if you’re pulling up Bloomberg, and you’re seeing a primary secondary markets spread, that’s relatively flat down slightly that’s a good indication of what’s going on with your base margin.

Michael J. Tierney

I would say we are pretty consistent with what you could look, what’s going out on the industry and the markets specifically.

I thought the conversation clearly described an origination market that is pretty strong, and while margins have softened some from the third quarter, which was one of the strongest ever, they are still well above historic levels and remain highly profitable.

I found similar comments a few days ago on the Sun Trust conference call (again via SeekingAlpha).

Our mortgage production income remains strong overall, with production volume again around the $8 billion mark this quarter, split roughly 75:25 between refinance and purchase. However, we did experience some decline in margins from their unsustainably high third quarter levels. This was not surprising, as well as we saw some usual fourth quarter seasonality decline in loan applications.

I mean, we really reached some rarified air on gain on sale margin in the [third] quarter. It was down probably about 15% or so [in Q4]. Will we see continued gain on sale margin to be under a little bit of pressure… If I look at the first 2 weeks or 2.5 weeks of the year, things are looking pretty good. I mean, our add volume really sort of jumped back up pretty significantly in January. It fell off a lot in the last 2 weeks of the year, which I think has a seasonal impact, but jumped back pretty significantly. So certainly, for this — what I can see in the short term, I’m still pretty optimistic about our other opportunities in mortgage.

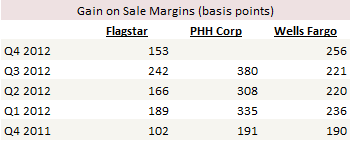

I did a bit of work to compare the gain on sale margin at Flagstar to some of the other originators out there that make the data available. Here is gain on sale from Flagstar, PHH Corp, and Well Fargo.

Flagstar had nearly a 50% jump on gain on sale from Q2 to Q3, while the improvement registered by Wells Fargo and PHH were of a much lower magnitude. One might think that the question the Street should have been asking was: “How did Flagstar’s gain on sale get so high in Q3?”

When I weigh all the evidence I am drawn to the conclusion that the Flagstar-shows-mortgage-origination-boom-is-over selloff is mostly fear induced. It doesn’t seem to me like volumes or margins have deteriorated much.

When will the Strength in Margins End?

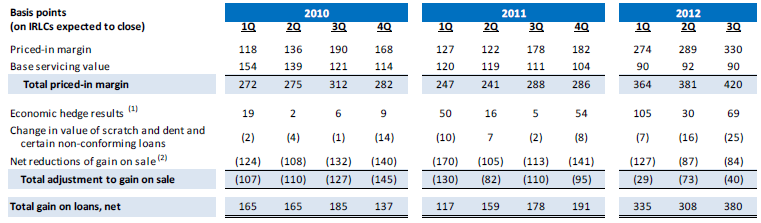

Nevertheless, it does raise the question of how much longer these margins can last? Taking a look at PHH Corp gain on sale margin going back the last couple of years shows just how high they have been:

Pipeline Press, a daily mortgage business update put out by Rich Chapman, often includes update of companies expanding, and he has been having an update almost every day about some mortgage op. that is growing and looking to hire. The competition is rising.

Another negative piece of scuttlebutt that I recently heard came from an episode of Lykken on Lending, where it was suggested (I can’t remember by whom) that the time to get approval from Fannie Mae to be a certified lender has fallen considerably.

A last consideration is that the US economy is improving. With that improvement will eventually come a rise in interest rates, and with the rise in interest rates will come a drop in refinancings. The refinancing boom may last another quarter or another year, but eventually it will end.

Of course the strengthening US economy means more demand for housing, and it is clear that the purchase market is strengthening. I also remain of the mind that margins going forward will remain above historic levels, as they will reflect the uncertainty of regulation and liability, and the costs associated with compliance.

What I’m doing with Impac and PHH

The picture I’m trying to paint here is intentionally ambiguous. It simply isn’t clear how long margins will remain at these levels, and just where they will settle when the refinancing boom settles back to more normal levels.

The bottom-line for me is what it all means for the stocks I own. The two stocks that are most directly effected by the outcome are Impac Mortgage and PHH Corp.

I’ve give it a lot of thought to my positions in both companies, and I am reluctant to make any moves in my position in Impac Mortgage before I see how the company’s fourth quarter played out.

The thing is, the management team at Impac pulled off what was pretty much a miracle when they managed to survive through the crash of 2008. They got into title insurance and built that business up, then got into residential originations and built that business up. They have said they plan to get into Commercial originations this year and so let’s see what they can do with that. Impac is growing, and the market likes growth. They are such a tiny company when compared to the origination market that there is certainly room for them to grow further. I think there is a niche for publicly traded mortgage origination companies (considering all the previously existing one’s have gone belly-up) and I think Impac could help fill that niche.

I did, however, decide to reduce my position in PHH.

I still think the company is still cheap but I am willing to concede that the market could easily send the stock back down into the teens if gain on sale margins do start to fall. More generally, with the stock here in the 20’s PHH has become more of a event driven opportunity, but one where the potential events (ie. a spinoff or a change in direction to a growth orientation) are of an indeterminable horizon. I decided to take off about one-third of my position in the company, which makes it an average sized position as opposed to an outsized position. Like Nationstar, its been a very good run in PHH since my original purchases in the $12 range, and I am always of the mind that when I am uncertain, it is better to be so from a distance than with too much on the line.

There has been a huge move in the IMH preferreds (IMPHO & IMPHP) on huge volume over the last 3 trading days. What do you make of this? Do you suspect a settlement is coming?