Never Afraid to Change My Mind and Change Again (MGIC)

Over the last couple of weeks I have been reading “Ideas have Consequences” by Richard Weaver, a somewhat well known and from what I understand quite well respected philosopher of conservative thought. The book, in which Weaver critiques the ills of our age and conveys the forgotten values of conservatism that have led to them, was written in 1948, and thus in retrospect it can be seen to have been quite prescient, having anticipated the spirit, if not an eerie amount of the details, that have come to characterize our culture. I would recommend it to any one interested in the subject of how we (as a society) have come to do as we do.

What I wanted to touch on here was a particular passage that I found striking, and also quite right.

In addition, the disappearance of the heroic ideal is always accompanied by the growth of commercialism. There is a cause-and-effect relation here, for the man of commerce is by the nature of things a relativist; his mind is constantly on the fluctuating values of the market place, and there is no surer way for him to fail than to dogmatize and moralize about things.

While Weaver’s intention is a broad sweep of our cultural landscape, I want to focus, perhaps somewhat ironically, on the narrower topic of how right he is when it comes to matters of investment.

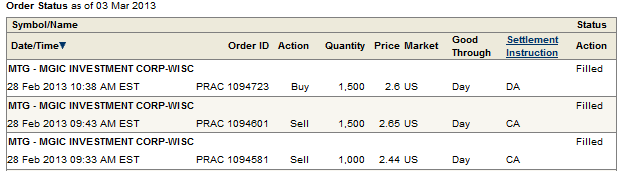

On Thursday morning MGIC released their fourth quarter results. I wrote last week that I had expected poor results in the fourth quarter, but even with that expectation the actual results were worse than I expected. The company lost abut $100 million more due to a reserve they took on Countrywide loans. The risk to capital ratio at the holding company rose to 47.8:1 and to 44.7:1 at the MGIC insurance sub.

While I have explained the limitations of risk to capital on a number of occasions even I was a bit taken aback by how high it had gotten and began to question whether the regulator may balk at this level. More importantly I was worried about how the market, which has put a lot of emphasis on risk to capital for the MI industry, might take the news.

And so it was that even though I had expressed a great deal of conviction about MGIC over the past few weeks, I sold some shares at the open.

I actually had every intention of selling the position down further if the stock continued to decline, but I wanted to wait until I listened to the conference call first. While the results had made me doubt whether I was right, I was not yet convinced.

On the conference call two comments caused me to swing my opinion back in favor of MGIC. First, the company said that they had the Wisconsin regulator on-board and highlighted that the regulator was looking specifically at claims paying resources, including future premiums that will be received, when doing their assessment. This confirmed my expectation.

Second, and probably more importantly, the company suggested that capital was available to be raised during the following exchange (from SeekingAlpha).

Craig William Perry – Sabretooth Capital Management, LLC: “…And if you’re talking about external capital, what would that look like? And please keep us in mind at Panning when you think about external capital.”

Michael Lauer: …and so, as Curt pointed out, the good news is that there’s a significant amount of capital interested in our industry. We’ve got new competitors coming in. They’ve attracted capital. We had the offering this week that was well-received. And we know that, just by talking to institutions in the last couple of months, there’s a lot of interest in our industry. So that all bodes well and we’ll look at all those alternatives.

As soon as I heard that the capital markets were knocking at their door, I figured that the game had changed (As I tweeted at the time). I bought back much of the stock I sold and changed my sentiment from negative to positive as quickly as I had done the opposite a few hours before.

My intent here (apart from conveying my thoughts on MGIC) is to illustrate a larger premise: just how quickly I have trained myself to disregard prior convictions and head in a new direction.

Now some might say that this is just recognizing ones own fallibility or just being flexible. If you wanted to frame it as a more spiritual extension (which admittedly may be a bit of a stretch) you might say it is an application of non-attachment.

These are all very positive spins. A more negative one, more aligned with Weaver’s thesis, is that I have taught myself to accept nothing on principle, believe nothing with certainty and let the most immediate evidence guide my decision.

While these are necessary skills and helpful aids to maneuver the market, I am not sure that they are the best skills for our culture to cultivate. And while I know that investing is a small part of most of our lives, I think that the argument could be made that it and similar decisions constitute a much larger part of that to which we consciously apply a set of principles and structure. It therefore holds that if that structure is mostly (for lack of a better word) relativism, well, I think it may pervade deeper than you think. And I’m not sure that’s for the best.

The point of Weaver’s book, if I may attempt a blunt summary of this complicated work, is to argue that in doing away with tradition, hierarchy, and a definite truth, we have left ourselves rather naked to harsh realities that we were never intended to contemplate. His argument is that it is not healthy, for the culture or for the individual, to reside where there is no truth to hang one’s hat.

Yet that is where we live as investors. No definitive truth, no certainty, only probability and event driven decision. This post is intended to address a small symptom of what is maybe the larger disease. In the short run, my pragmatism resulted in a great deal of success with MGIC this week. In the long run I wonder what it costs.

Good post! I sold out of MTG too early. I think the conference call spooked me. What I found lacking from the conference call was a strategy to regain lost market shares. I ended up switching to RDN and GNW. Originally, my bias was that RDN was overvalued and MTG was under valued. But in the end, because RDN is currently the market leader in NIW, fast forward a few years, it will have the least % exposure to pre-08 loans. From this perspective, the reason that I found MTG undervalued (its large LLR) became its drawback. I rather own the new market share leader with the least amount of risk from legacy loans.