Could my Next Big Play be Leveraged Companies? (Y, NXST, HOV)

Early last year I warmed up to the idea that housing was in the early stages of recovery and this single idea generated a number of successful investments for me (NCT, NSM, IMH, MTG, RDN, HOV…). With many of these housing investments having now played out I have been trying to think of what big idea might drive my strategy in the next 9-12 months.

What occurred to me rather suddenly this week was that perhaps I had already figured that out, had even been acting on the idea, though I had not articulated it consciously.

Companies with excessive leverage have been shunned for the past 5 years. Many have lagged as questions about their ability to continue as a going-concern have superseded any potential out-performance to the upside if things take off.

I think that this might be the year that changes.

Much like my idea with housing last year, this is an idea, a theory, and by no means something that I am convinced will happen. Its something that makes sense to me and could be quite profitable if it plays out the way I imagine it. Much like housing last year, it feels a bit scary.

Nevertheless, I have waded in with purchases of stocks like YRC Worldwide, Arkansas Best, Nexstar, Yellow Pages, and Axle Manufacturing (which I unfortunately subsequently sold), all of whom would be considered quite levered on most scales. I am actively looking for others.

The reason it makes sense is that we have entered the rather unique situation where either the US economy is going to start to improve (which some of the latest economic numbers suggest might be happening) or the Federal Reserve (along with just about every other Central Bank on the planet) is going to continue to print money and keep interest rates absurdly low. In the former scenario business could finally begin to improve enough to support the level of debt on the balance sheet (or at least give the perception that this is the case for a time) and in the latter investors will continue to look for places to put all of this money sloshing around, a situation that I have found to be beneficial of speculative plays (a case could be made that it is this behavior that has benefited Radian and MGIC),

The difference between this round of quantitative easing and the previous ones is that this time around its open-ended. So while in past incarnations investors have shied away from the more highly levered players because of the concern that they be left standing when the music stopped, the Federal Reserve has made it quite clear that this time the printing will continue until it is no longer needed. This seems to me to be an invitation to take on positions in longer duration stories.

Adding to Nexstar, Hovnanian, and Yellow Pages

In the spirit of this new idea, in the last few weeks I added to some leveraged names that have been working for me. Hovnanian has a market capitalization of $800 million (common only), negative common equity and debt of over $1.5 billion. Yellow Pages has $900 million of debt and debentures versus $240 million market capitalization. Nexstar has a market capitalization of $500 million, negative common equity and debt of $613 million.

In the case of Nexstar and Yellow Pages, both companies are generating significant free cash flow.

Nexstar posted $29 million of free cash flow in the fourth quarter. Estimates of free cash flow for 2013 are in the neighborhood of $3 per share, followed by $4 in 2014 (with the increase being partly due to advertising revenues from the political cycle). I think that with an improving US economy, a refresh in the auto-replacement cycle (car ads make up an amazing 26% of all advertising on television, something I just learned and was surprised by), and continued growth in re-transmission revenue that Nexstar gets paid from cable providers who carry their stations (note that this is a source of significant growth for Nexstar and probably deserves a post in its own right to explain properly).

I originally bought a half position in Nexstar at $15, bought the other half position at $14.30 and then again this week at $17.

As for Yellow Pages, I did some work on the stock back in early February, stepped through the 2012 numbers. When I backed-out the one time charges associated with the restructuring I estimated that the company netted about $285 million in free cash flow in 2012. With roughly 28 million shares outstanding that works out to a rather insane $10 per share (the stock is trading at $8.50 right now).

The catch of course is that the company’s primary source of cash (phone books) is declining at a significant rate. Yet when I model out cash flow generation in 2013 and 2014, mitigating a 20% decline in phone book revenues with a 5% increase from the on-line and mobile businesses, and assuming a gross margins decline from the current 50% level to 40% by 2015, I still see cash flow generation of $250 million in 2013 and $200 million in 2014.

While its difficult to predict at what level free cash flow will eventually stabilize at (it won’t occur for a few years and depends on how successful the company is in growing their on-line brand), I suspect it will still be in the high double digits. By that time the cash flow generated in the interim will have been used to pay off most or all of the company’s debt, and the result should be a significantly higher share price. I also note with interest that Kyle Bass has taken a large position in the US yellow pages companies, Dex One and SuperMedia (two more stocks I need to look at when I find the time).

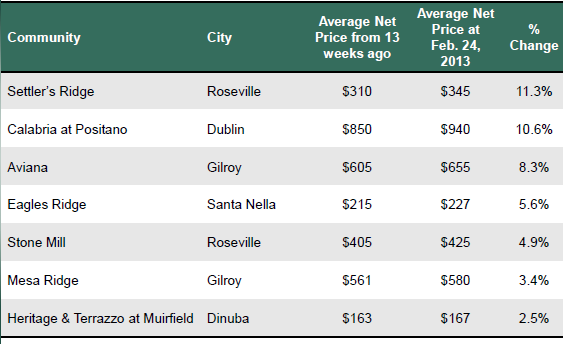

I also added a small amount to my position in Hovnanian after listening to the company’s first quarter conference call on Friday. The home building business seems to be progressing well. The company provided the following table of price increases occurring in Northern California over the past 13 weeks. Northern California was one of the hardest hit markets during the crash and is also an area where Hovnanian holds a lot of undeveloped, mothballed land.

While Hovnanian has a negative book value of about $480 million, its worth pointing out that they have written down to 20% undeveloped land that previously had a carrying value of $600 million. In addition the company has another $900 million in net operating losses that they have written off completely against a valuation allowance, but that would quickly come back on-balance sheet once the company can demonstrate profitability on a sustainable basis.

Also interesting with Hovnanian are the preferred shares, which were pointed out to me by a fellow on twitter that goes by the moniker @adoxen. He recommended I take a look, which I did, and I can see the opportunity. I might write up something more substantial on them once I’ve had time to finish working through the numbers on them.

A couple questions on YLO. Why do you think they’re setting expectations for debt-paydown at the minimum of 100m in 2013 if they may generate 200m, which would imply a 150m paydown? Do you have an opinion on the value proposition of YLO’s digital platform for customers vs the competitive environment?

I don’t think the conversation about the cash sweep on the CC was terribly clear. I mean like you said the $100mm is the minimum – the one analyst pointed that out and then they agreed they could pay more, but that they could also pay less, and then they said yeah just go with $100mm. The spirit of the exchange did not sound as much like a confirmation of guidance to me as it sounded like they weren’t prepared to make any further projection. It also seems that there is a reserve that is going to go into the calculation and they said this was “significant”. I can’t find any reference to this reserve in the indenture filings (tell me if you find it) but I wonder whether its a CAPEX reserve, they suggested it would be for expenses anticipated over the next period and so if it was that could be the extra $50mm right there.

Coming up with an FCF number above $200mm is not difficult. I mean if you go to the company’s own Q4 supplemental disclosure they point out themselves that mean EBITDA estimates for 2013 is about $435mm… you can do the math on interest costs, and they said CAPEX was going to be $50mm to $55mm for the year.

As for the business going forward, well I guess that is the question we will have to watch. I’m not going to try to project it. Its going to depend on how well management is able to leverage the existing relationships and existing on-line platform into future growth in advertisers. I think the best I can do right now is conclude they’ve done a pretty good job so far. And the stock price doesn’t seem to reflect that.

Look at the definition of Excess Cash Flow in the indenture. They’re allowed to withhold CF for major one time payments. Perhaps they’re required to spend 50m+ to purchasing the 70% stake in 411.ca?

Also, I’ll note those estimates in the supplement are analyst estimates, not company guidance, and I think they’re are only two analysts following. Given the dispersion in outcomes, I’d say those estimates are likely unreliable (in either direction, mind you).

You don’t need to project the future business to know whether or not they’re product is competitive in the marketplace today. How does the website offering compare to Google Places? What is the value-add of listing on Yellowpages.ca to an advertiser? Etc.

Sounds like you have an opinion on how their products stack-up against the competition. I’d love to hear it.

Also I wasn’t suggesting it was company guidance. That’s why I said mean estimate.

I do. But I’ve said too much already 😉

This is an interesting idea. I think Fidelity High Leverage (something like that) and the stocks in JNK holdings are good ideas. I put together the latter here:

http://finance.yahoo.com/quotes/highdebt-jnkholdings,S,HCA,CZR,cpn,CYH,LYB,CCO,DISH,ETE,CLWR,LINE,TDG,CNX,RAI,FSL,BTU,WYNN,BEAV,HD,WCRX,NRG,FDP,LVLT,FTR,NLSN,WIN,GRFS,NXPI,AES,CIT,LTD,WPX

Just a warning on DEXO and SPMD, when backed out of there EBITDA margins using linear regression with management projections for their print and and online segments, their print segment has healthy looking margins of 47-50%, but their online segment has EBITDA margins of around 3-7%, this compares to 47% for Yellow Media. I don’t really know why this is (maybe because yellow has a monopoly in Canada and isn’t pricing for growth) but if you look into these companies and find something different it would be great if you let me know.

I haven’t looked at either DEXO or SPMD very closely but Yellow has guided to 40% margins over the long run. Sounds like it would be worth understanding what the difference is due to though. Thoughts anyone?