Week 88: Take-off (MTG, RDN, MBI, PKI, NTI, IMH, WD)

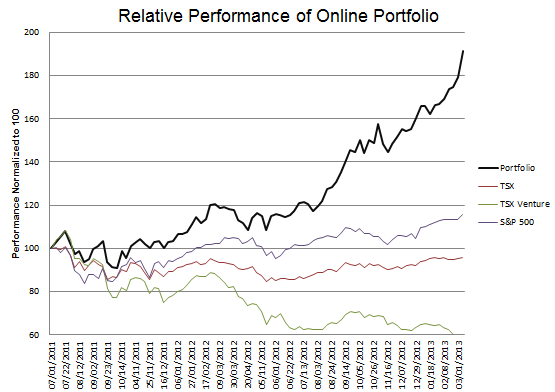

Portfolio Performance

See the end of the post for Portfolio Composition and weekly trades.

A week of Significant Gains from RDN, MTG, MBIA

The last seven days have been extremely good ones for my portfolio. This has been primarily due to the price appreciation of MGIC, Radian Group and MBIA. As regards MGIC and Radian, I have written so much about these two names, done so much work trying to understand the business (and trying to understand how other people were trying to understand the business), that it is quite rewarding to see it play out the way that it has.

It is amazing to me that MGIC has more than doubled (from a $2.40 low to a $6.10 high) during 5 days when the only notable disclosure was that the company had the ability to raise capital. Someone with an interest in market psychology should really write a piece on MGIC – you could call it the Existential Security.

I reduced my position in both Radian and MGIC by a little more than half during the early part of this week. My sales of MGIC occurred around $5.20 while those with Radian were at a little over $10. I don’t have plans on selling any more of either.

I sold the positions down because they were getting very large (particularly in the case of MGIC) and because my thesis, that these companies would be able to survive, has now played out. What is going to drive the stocks going forward is the long-term potential of the mortgage insurance business and how well each company can capitalize on it.

When you consider all of the work I have done on these two companies, it may be somewhat surprising that I have not spent more time looking at the long term potential of the business. But I have been focused on the question of survival because up until now that has been the only question that mattered. With both companies now having raised capital that has changed. The question switches to the level of new business and the profitability of that business.

While I haven’t had time to look closely at what earnings might look like post-capital raise, on a purely qualitative basis I do like where they stand. Consider the following. The insurance business is a difficult one to get into. There are a couple of potential competitors that have been moving towards writing new business but it has taken them over a year to get one to the point where it is able to. The old-guard competition is all either in run-off, bankrupt or trying to wind down the business.

Meanwhile the new business being written is some of the best ever on multiple fronts. The expected returns are around 20%. The loans being underwritten are being done so with extremely tight standards; the potential exists that losses may be substantially less than the historical trends. And if interest rates begin to rise, the monthly premium business (where the MI collects insurance over the life of the loan) could end up generating income for far longer than has typically been the case (in this sense the MI business is kind of an anti-refinancing boom play).

This all sounds quite bullish, and yet I sold a significant amount of both stocks. Why? Well the run up has been tremendous. Remember I was buying MGIC at 60 cents, and Radian at $2.50. My position size has become huge because of the gains. It simply wouldn’t be prudent management to hold both stocks in the size I had them.

Another factor is that I need to take a step back and regroup my perspective. It may seem like an odd thing to say, but I find that I am best served by stepping away from stocks I have had large positions in after a time, because my judgment becomes clouded by the close scrutiny. I begin to become to caught up in price levels and my own history with the name and lose sight of what is truly going on.

I will say however, that if there is a substantial correction in either name, say to below $4 for MGIC or $7 for Radian, I won’t hesitate to add the positions back.

As for MBIA (MBI)…

We finally, and I do mean finally, got a ruling from Judge Kapnick on the Article 78 ruling. I remember back in August how I hoped the ruling would be out before 3rd quarter results. A bit of wishful thinking there.

But at least when the ruling finally came, it was in favor of MBIA. The Judge upheld the transformation, which would allow the structured finance division to be effectively cornered off from the resources of the public insurance division and, importantly for us shareholders, put what is in my opinion a floor valuation on MBIA of about $18 (which is what the public finance division, National, is worth).

Christian Herzeca, who has done yeoman work on MBIA that rivals the work of any analyst, put out an excellent summary of the ruling here.

I added to my position because, as Christian says, even with the appending appeal the chance that the transformation is not allowed to proceed is now quite remote. The ruling has been described by most as being air-tight, and Kapnick is not known for having her rulings overturned in appeals (it has only happened twice in 5 years).

I do, however, have some remaining questions that keep me from adding further. First, how long can Bank of America drag on this appeal process. Bank of America’s intent has from the start seemed to be to buy time, so almost as important as the decision is the time remaining before the issue can be put to bed for good.

Second, the structured financing wing, MBIA Corp, is facing a liquidity crunch. While MBIA Corp has statutory capital of $1.5 billion, they only have about $300 million in short term liquidity that is available to pay immediate claims (its interesting that this is exactly the opposite situation that MGIC was having, as they had more than sufficient claims paying resources but their statutory capital number appeared light). The company said on the fourth quarter conference call that they expected losses from their insured CMBS to exceed that amount either later in 2013, or 2014 at the latest.

(Note that an interesting complication in the tangled web of Bank of America and MBIA is that the CMBS portfolios on the precipice of default are actually held by Countrywide (which is of course owned by Bank of America), and in the event of default at MBIA Corp these portfolios would take a back seat to many of the insurance wings other debts before being paid out.)

Earlier this year MBIA Inc amended its unsecured holding company debt so that in an event of a default at the insurance company (MBIA Corp) those notes could not be accelerated. On the fourth quarter call the company said that all that remains at the holding company is about $1 billion of guaranteed investment contracts that would be able to be accelerated in the event of default at MBIA Corp. But they pointed out that these contracts are secured by “high quality and highly liquid assets” and so it is remote that the holders would accelerate them. Therefore the holding company and the public insurance division should be protected regardless of what happens at MBIA Corp.

So I feel comfortable with my position. The worst case scenario seems to be that a settlement with Bank of America can’t be reached, that MBIA Corp is seized by the regulators and that the value of MBIA becomes the value of National and whatever residual can be eventually extracted from MBIA Corp. The preferable, and still to me the more likely scenario, is a settlement with Bank of America that unlocks additional value at MBIA Corp. On with the waiting game!

Adding to Nexstar (NXST), Hovnanian (HOV), and Yellow Pages (Y.to)

I decided to add this last night as a stand-alone post. It can be accessed here.

Selling Parkland Fuel (PKI.to)

Parkland Fuel continued in the tradition of its predecessor Avenex by becoming a bit of a debacle for me.

I bought Parkland Fuel after Avenex sold to them the asset for which I had bought Avenex for, Elbow River Marketing, which is a liquids transportation business well positioned to take advantage of the excess crude volumes in Western Canada. But I simply didn’t do the due diligence on Parkland that I should have. I bought the stock because I liked the price that they paid for Elbow River (less than 5x EBITDA) and it was a somewhat material acquisition for the company (it looked to increase the company’s EBITDA by about 10%). But I didn’t look that closely at the rest of the company, which caused me to miss some key considerations.

In particular, I did not recognize just how dependent the commercial segment of their business is on industrial and oil and gas activity in Canada (something that has been lagging of late, particularly the oil and gas side). I also did o’t understand that a material portion of their earnings have been derived from a refinery profit sharing agreement with Suncor which will terminate at the end of 2013.

Of course I learned of all this information late into the night after the fourth quarter earnings release and after the stock had been plummeted some 12% that day. While the nature of my predicament (limited time, unlimited questions) necessitates that I cannot understand every crumb of every company I invest in, I cannot afford to miss such large bites. Its inexcusable and I paid for it with a 12% loss. Selling at pretty much the bottom was icing on the cake, but I will not apologize for that. When I am wrong, I am wrong, and the only thing to do is cut my loss and move on. I have found no luck timing for a bounce when I need out of a position.

Gold Stock Bet

I added to a number of gold stocks. To Atna, to Esperenza and to OceanaGold. I took the largest position in OceanaGold, which inexplicably fell to $2.30 during the worst of the panic a few weeks ago. I’ve written enough about OceanaGold and their growth from Didipio so I am not going to repeat the story here. Suffice to say that after the listening to the Q4 conference call and reviewing the financials I am comfortable with the position (I think that the delays at Didipio are not anything to be worried about longer term).

I initiated a position in Esperenza just before the deal with Silver Standard and then again after it was announced. The second purchase was a bit ill-timed as I added at $1.30 and the stock subsequently fell to below $1.10. What led me to add was that the financing from Silver Standard gives Esperenza much needed development capital at a reasonable price, and the La Bolsa project, which is a low CAPEX, near term production story that they received from Silver Standard, could move Esperenza relatively quickly from the advanced exploration bucket to the small producer bucket. I just remember the move in Argonaut Gold when they went through a similar transformation with El Castillo and I think that may be a template for what will happen with Esperenza.

I also thought it interesting that gold did not correct further on Friday when the jobs number came out. It is my suspicion that once the shorter term speculative money is out of gold (something that may be almost complete) the longer term money will keep gold from falling too far. Demand will continue from India, China, Russia and all the other countries looking to diversify from currencies inflicted with the printing disease. I wrote about the subject in this post, where I made the following observation:

I was a little surprised by was by just how much India and China mean to the market. I mean for all practical purposes, India and China are the market.

I think there is far too much emphasis put on the western world demand for gold, and far too little put on the impact of demand from India and China. While we fret about the next move of the Federal Reserve and what that will mean to fast money ETF investors, the real story here is the emerging wealth of the emerging markets and the consistent flow of money from them into gold.

Out of Northern Tier

I traded out of Northern Tier because A. I felt I owned too many stocks to keep track of, B. I was gaming the timing of a correction in the market, and C. I still don’t really understand the timeline of pipeline reversals and additions and thus have some trepidation as to when spreads are going to flip and head south.

Unfortunately, my timing was impeccably bad and the stock subsequently made a dramatic move up from where I sold it (around $27) to $31. I shouldn’t complain. I made a quick 15% on the stock and that’s great. But perhaps I should have listened more closely to my own reasoning before jumping the gun. From my Week 85 post.

Given the regulatory environment here in Canada I think there is a better chance that Northern Tier receives wide spreads for longer than Alon Energy Partners does. But we shall see. I am more than aware that this is probably a short-term phenomenon that won’t last forever. Therefore I am keeping my position in Northern Tier reasonably small so that I can get out quickly when the cycle turns.

In the heat of the moment I didn’t follow this advice and the stock is up another $4 since I sold it. It is a sometimes good idea to lock in gains but it is a much better idea to think through the decision carefully to make sure you are not leaving too much on the table. My decision in this case was made rather suddenly, basically the thought: “I should really take some profits, now where can I take them from?” was the extent of it, and for that simplicity I was penalized.

PHH (PHH) and Impact Mortgage (IMH) – Gain on Sale reductions

Another move I made was to get out (at least for the moment) of PHH Corp and slightly reduce my position in Impac Mortgage. On the general topic of the origination business there is not much that hasn’t already been said. I remain concerned about origination volumes and gain on sale margins, and I want to limit my exposure to a more conservative position.

The results at Impac weren’t as good as I had hoped, but I didn’t think they were as bad as the stock drop led on. The company earned 92 cents per share from continuing operations, which was less than the 3rd quarter. The drop was due to the mark to market value of the origination pipeline. The pipeline dropped from the end of Q3 to the end of Q4 and as part of the origination accounting Impac records the fair value of the interest rate locks and hedges of that pipeline. Because of the decline in pipeline size, the mark of those items to market generated a $5.2 million loss in the quarter (about 70c per share) that weighed on the results from the mortgage segment.

The bigger question is what growth will look like going forward. I had been hoping that Impac would continue to show growth in volumes in Q4 due to market share increases but the volumes expected for Q1 suggest that their growth is slowing along with everyone else. I suspect that the market had hoped that Impac would show above average growth and was disappointed when they did not. The company said volumes were going to be down ~20% in Q1 and then suggested that competitors are down maybe 15%. That is what I think has hurt the stock. I had to reduce slightly to follow my own rules. I always reduce when a stock is working against my thesis.

Some positive news is that Q1 should bring an increase in pipeline size and the associated mark to market gains. Some other positive news came on the conference call (from SeekingAlpha). While the company did not do a great job communicating the information, it appears that there is potential to expand their Real Estate Service segment to become loss mitigation experts for other servicers. Below is the relevant clip from the call with my underlining of the sentence that really caught my attention (my underline)

Seven years ago, we looked around and what we’re going to do. And we saw a huge void left in the market place by the services. There was Bank of America that the GMAC and we get up on ourselves to begin modifying loans and starts selling the loans, et cetera. And in that being business and it became very, very successful. And as result, during the clarifying bit of money continues to earn a significant amount of money, but we also said that as the portfolio improves [those revenues will decline].

…Now with the transfer of servicing and I don’t know if you understand this but bank of America GMAC were sub services or servicing a lot of our loans in the – sold their portfolio or attempting to sell it and they’re moving to other services. And those are the services are taking look at the results that we have achieved and saying, or maybe what will do is higher impact to continue managed the portfolio or perhaps there’s a more business there to continue the loss mitigation services for other servicers, because quite frankly, necessity is some other invention, we became very good at loan modification short sales, loss protection, we became experts at it. And we are currently offer those services to others, so that’s what I mean to tell.

I was also hoping that Impac would describe their progress on the commercial real estate side but unfortunately there was no mention made. I think there is a real opportunity here, which leads me to my next investment….

New Position in Walker Dunlop (WD)

I added a significant position in the commercial real estate originator Walker Dunlop this week. This post is beginning to get extremely long so I am going to limit my comments on this one for the moment. To be brief: Basically Walker Dunlop is the commercial equivalent of Nationstar. What interests me is that the company is cheap, has a portfolio of servicing rights that will likely prove to be worth more than they are currently valued, and is involved with the commercial mortgage business.

The company made the following general comment about the commercial mortgage business in their press release, which is originally what caught my attention:

The Mortgage Bankers Association estimates 14% annual growth in commercial / multifamily loan originations until 2015, and with almost $2 trillion of commercial real estate loans maturing over the next 5 years, our market opportunity has never been greater.

The sensitivity of the commercial origination business to rate changes and refinancings is much more muted than the residential business, while the sensitivity to improving economic activity is more important. I think that is a promising combination. And like Nationstar, Walker Dunlop has Fortress backing so that leaves opportunity for interesting deals.

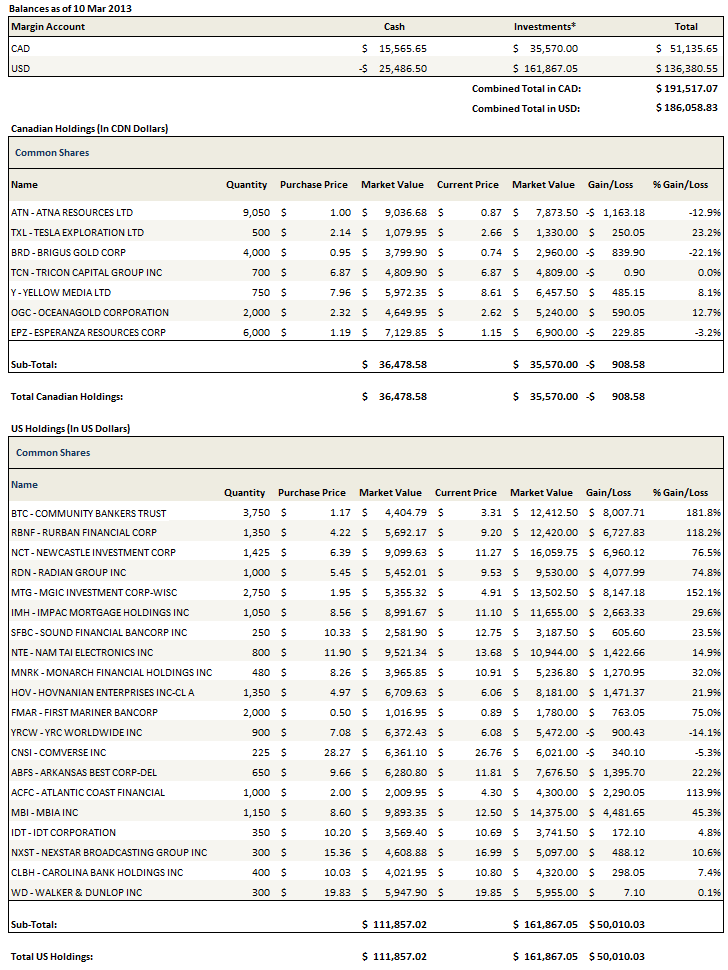

Portfolio Composition

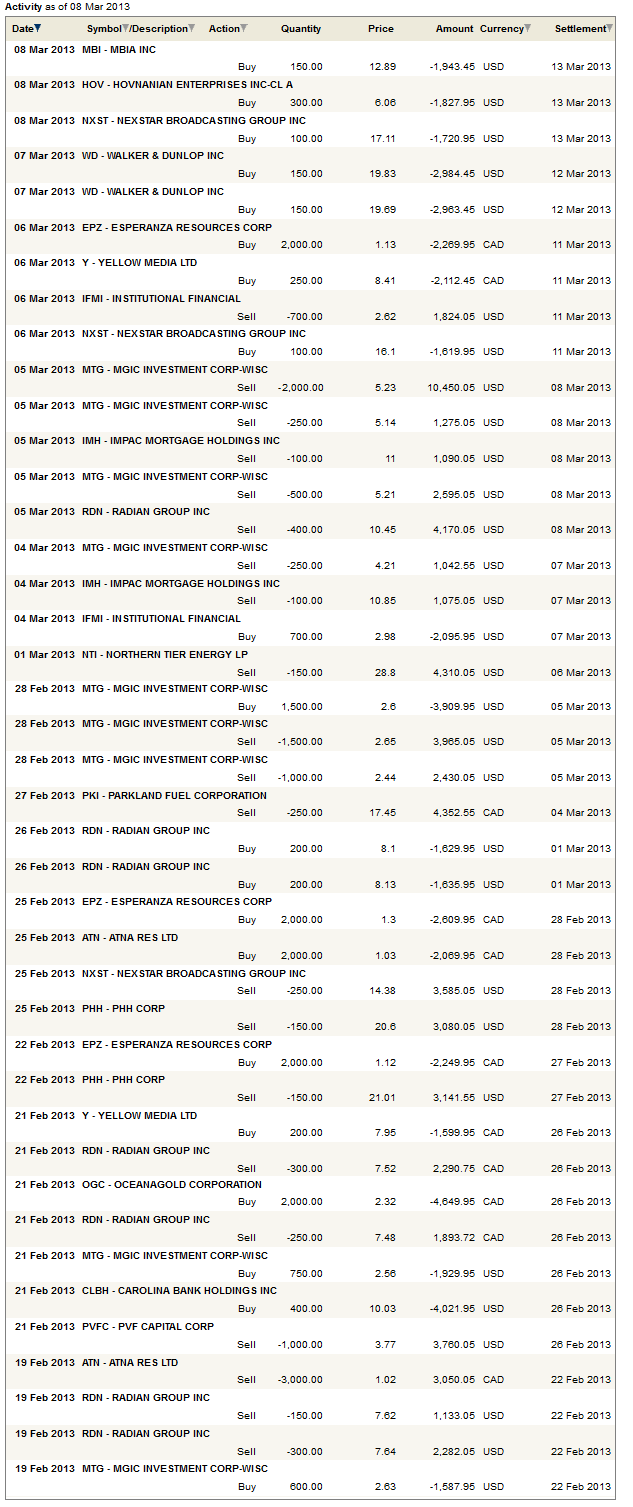

To see the last three weeks of trades, click here.

{kind=link}

Seems that you are reducing number of positions. What are your current favorite names with the highest conviction. Thanks.

IMH will still grow their volumes YoY just not QoQ. We saw in total 93% growth for 2012 (2.4B from 885MM). Management has already given us their expected originations in the 1Q at 650 (vs 365 a year ago). Also, warehouse lines are growing over time. If there were any constraints before, that should help alleviate those constraints. While I am not looking for growth like 2012-2011, I think it is pretty conservative to say that originations will grow again in 2013.

Maybe you already had a large position and sold some, however I am happy to get a second shot as my initial position from 10 was small. Additional earnings reports (and the forward guidance) has gotten me much more comfortable with IMH being undervalued.

My reduction really has little to do with my assessment of the companies prospects. You have to keep in mind that my position in IMH was extremely large and the stock is very illiquid – it was just prudent risk management to reduce it down to the size of a position that I can exit in a few days if I have to. And for no other reason than that these are uncertain times – if something truly untoward begins to unfold, I don’t want to be caught in positions that I can’t get out of. I’ve had that happen before and it is not a good space to be in.

Thanks for responding. I suspected that it was just reducing an already large position. I remember seeing your purchase price much lower. Actually, I first came across your blog after I heard about IMH from a friend and happened to find your blog while searching for more details about some questions I had.