Projecting Yellow Media

Because of my work situation I am faced with a limited amount of time to analyze my investments.This precipitates the need for efficiency and a focus on the questions that matter most.

Thus I spend a good deal of time thinking before I spend any time analyzing. This is particularly true when I am just introducing myself to an opportunity. I think about how I can distill it down to one or two questions that I can focus on. Rather than taking the approach that I need to understand every aspect of the company (something that I simply don’t have the time to do) I look for the lynch pins and focus on understanding their mechanics in great detail.

To give a few examples; this was my strategy for the mortgage insurers, where I focused strictly on whether or not they would pushed into run-off or bankruptcy by the regulators. With Arkansas Best I focused on what the upside might be if the company negotiates a union contract similar to that of YRC Worldwide. With YRC Worldwide I focused on their leverage to the upside. When I initially bought PHH I focused strictly on the value of Fleet, which allowed me to view the mortgage operations as an upside option.

With Yellow Media, I narrowed it down to two questions. They are:

- When and at what level is the online business going to grow enough to offset the declines in the print business.

- What assumptions should be used to answer question 1

First the Assumptions

The second question must be answered first. Assumptions must be made about future growth, future margins, tax, interest and capital expenditures.

Extrapolating the future growth in the on-line business is tricky because of the divestitures that Yellow Media has made in an attempt to bring the debt down. Thus I have excluded the impact of CanPages, LesPAC, Deal of the Day and YPG USA in the estimates below.

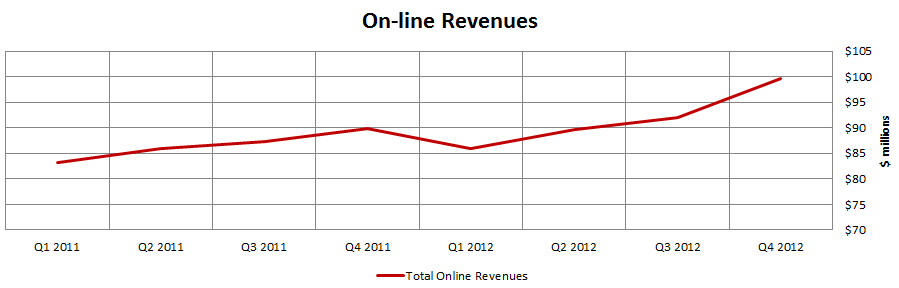

The company said year over year growth in on-line revenue was 15.7% in 2012 though I’m not sure how they calculated that. I calculate 6%.

The company has been growing on-line revenues by converting its print advertising base, and in my opinion success going forward will be determined by how effectively they can continue to do this. If you look at the increasing penetration of print subscribers who are subscribing to on-line or mobile placement, you can see that they are having success so far.

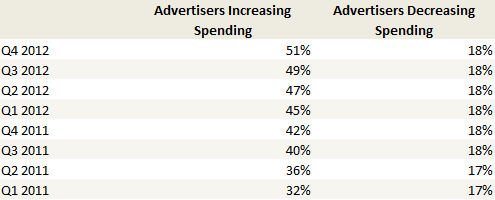

Additionally, the company has been getting more advertisers to increase spending (presumably increases are occurring via the on-line business, not print) while advertisers that have decreased spending has flat-lined (though, as I will describe below, the 18% are likely key customers). This is a sign that existing advertisers are finding value in the products.

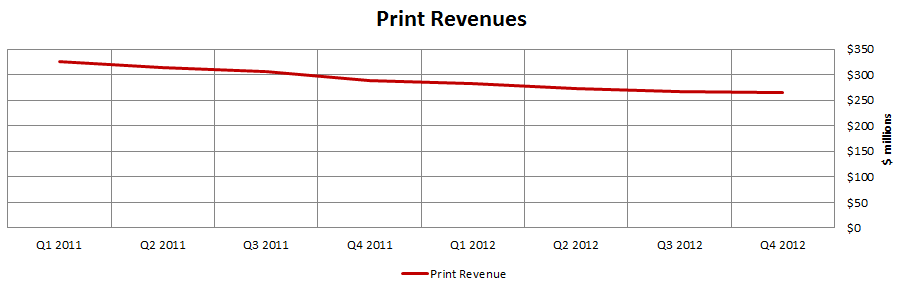

As for the print business, it is in terminal decline. However it does appear to be in a fairly stable and predictable decline. The chart below illustrates the year over year fall in revenue.

The fall in revenue is due to some advertisers choosing not to renew. Only 86-87% of print subscribers have renewed over the last two years.

Based on the above and on the color provided by management, I think that I can put together some conservative assumptions about how growth may look in the future. My rough, baseline estimate is to assume that on-line revenues grow at 6% per year while print revenues decline at 21% per year. This is consistent with on-line growth over 2012 and compares conservatively with the decline of 19% for the print business.

There are a couple of potential positives that could help boost both the print and on-line businesses. Consider the following:

- On the first quarter conference call management pointed out that approximately 82% of their advertisers were exhibiting either stable or increasing spending trends. Only 18% of the advertisers were lowering spending. However those 18% of advertisers were skewed towards large companies whose spending made up about 40% of Yellow Media’s revenue. It was only in 2011 that Yellow Media began to address the deficiencies in their product offerings and focus their sales towards these clients. Its possible that success could slow the revenue declines in print.

- According to comments on the Q3 conference call, in the last year the company put very little investment into their brand prior to the restructuring. It was only post-restructuring that they began to make a more concerted effort to re-establish their brand and relevance in the market. The lull, and the restructuring, has likely had a negative impact on the perception of advertisers and stabilizing that perception would help mitigate revenue declines.

As for gross margins, management has guided that they will decline as the print business declines and is replaced by the on-line business. Guidance is that gross margins will trend to 40% (from its current level of above 50%). I would expect this to occur over the next couple of years and have allowed for this in my model below.

I came up with an interest expense by tallying up the cost of each of the new notes. They add up as follows:

- $800mm of 9.25% senior notes would be $74mm per year

- $100mm of 8% subordinated debentures would be $8mm per year

- $7.5mm of exchangeable debentures, presumably at 8% would be $0.6mm per year

Summing these items up, total interest would be $82.6mm per year. Note that this compares to interest costs of $148mm per year before the restructuring.

I didn’t put a lot of effort into coming up with a depreciation and amortization number because I am mostly concerned with cash earnings. I just went with $100 million each year going forward, which is around the same level it was on 2012.

As for taxes, the company says that they expect to pay $60 million in cash taxes in 2013 and $80 million in 2014. Subsequent to that it doesn’t appear that there is a significant deferred tax asset so I have assumed 27% tax rate after 2014.

When is the on-line business going to begin to stabilize overall operations?

With those assumptions at hand, I came up with a rough model that projects how earnings and cash flow would develop over time. This is shown below.

The results are a bit ridiculous when looked at on a per share basis. There are about 28 million shares outstanding. I am estimating pro-forma free cash flow of $243 million for 2013, which is about $8.60 per share. I would expect them to have fully paid off their senior debt (of around $800 million) sometime in 2017. By 2018 growth in the online business is offsetting declines from the print business and free cash flow of around $4 per share.

If anything approaching this scenario plays out, I don’t really see how this stock stays at these levels.

Now I understand that there are many risks to this model. Margins may end up being below 40%, the online business may fail, or the print business declines may accelerate. All of those things need to be watched closely for as this certainly isn’t the sort of business where you rest easy and wait for your assumptions to play out. But there is also a lot of room for error when your estimate is calculating free cash flow as a per share basis that exceeds the current share price.

One thing I will say is that I am not entirely sold on their product line. I’ve spent some time playing with the websites (I have not downloaded the mobile apps yet) and in my opinion is that they are ok. I can see the value in Redflagdeals.com, the forums on the site seem busy enough, and the flyers section is handy, but I didn’t see a lot of local businesses advertising deals, it was mostly chains. The flagship Yellowpages.ca site is solid (I’ve used that site to find local businesses for years now) and provides the basic business search that you expect from a yellow pages offering. I found the Canpages.ca site a bit difficult to navigate (it kept setting my location to Toronto, which is not where I live), and the success I had finding a business really seemed to depend what I was looking for; some topics seem well populated while others are sparse. The one thing that would make the CanPages site more useful would be reviews, and that seems to be where gigpark.com comes in, but unfortunately, while actually pretty functional, didn’t produce very many recent recommendations.

So it appears they have more work to do. But it may also be that I am not the target audience; I am not a shopper and apart from my investment research I spend very little time on-line (I don’t own a smartphone, which is why I haven’t used the mobile app yet). I would welcome other informed opinions about their product lines.

I originally bought Yellow Media at $7.50 in the middle of February, becoming aware of it after @FamilyOfficeGur piqued my interest with his numerous #phonebook tweets. I thank him for directing me towards the idea. I have continued to add to that position through this week, at as high as $9.25. While I understand the risks, and I understand that this is perhaps not the best business, I have to think it is worth more than the stock is trading for, even now. I also have to wonder whether a private equity firm interested in milking the free cash of the business might become interested in it, or whether a competitor looking for a stronger Canada presence might find it an interesting take-over candidate (it would most certainly be accreditive to earnings for most anyone). At any rate, the potential reward seems to more than offset the risks, and so I have been willing to roll the dice on this one.

It really is a tough call in my opinion how they do. The large debt amount is concerning and I think it will be a race to pay this off while cash flows are high and before they decline. If they can get ahead of the curve on this, they will do well. If not, it will kill them.

The good thing is that their on-line search technology is finally good. It took so long to get this right and was so frustrating to use that I’m sure many people have just given up and use google now. I know that with my 20-something kids, they don’t even think of using canada411. Their mobile app is also good, but I rarely use as google search works as well and sometimes better and is integrated into google maps, so I can get voice directions.

The actually yellow pages book goes right into the recycling at my hose as well (no-one uses that).

I’ve been dealing with some home contractors lately and they do, for the most part, still use yellow pages. But they all ask now how you found them to see where they should be spending their money and they seem to be trying to judge how much to spend on their web site versus yellow pages. They generally seem to think yellow pages are OK, but expensive.

One idea would be to try and talk to some business owners and get their opinion on use yellow pages. My sample was small and I didn’t drill into details like how long they planned to use them. I think this is the key as these are the people that need to see the value in order to continue to use them.

Anyhow, thanks for the thorough analysis – you do great work. Good luck with this stock!

Thanks for all the feedback and first hand experience with the company. I mentioned in another comment that I could see benefit from buying homestars, it doesn’t seem like Yellow Media has anything that fills that niche and homestars is a useful site. See my other response for how I am weighing the longer term questions about the business.

Great analysis and thoughts. I enjoy your review of the online offerings and I think your assumptions are all pretty valid. Our firm holds YLWDF (US OTC version) across client accounts and we built our position in February. The emotional responses I get from it are certainly interesting, however, when I ask clients who uses the print Yellow Pages, about 1 in 4 respond that they still do. Generally they are older, however, when I delve into their usage, they use the print Yellow Pages to buy-not browse. I am located in the U.S., so there may be a difference there, however, there is still a demographic that uses the print version.

Our view is that management burnt the previous shareholders so bad in the recap, and it is likely that current debtholders don’t want to hold the equity (except for some control to protect their debt), that there is no natural constituency to hold the stock.

While I’m sure you chose not to include information on the debt covenants to keep your point straightforward, a significant factor in our decision to build a postion was that the firm is required to paydown debt with their significant free cash flow.

Thanks – all good points. The point about the customers being older is true and another problem that potentially haunts them long term. I think that the reason the stock is as low as it is has a lot to do with your point about the shareholder base. At least that is my hope, that the price has been influenced to some degree by forced selling and as these sellers dry up (hopefully that has happened) the stock settles at a level somewhat higher.

That’s a well-written and thoughtful post. Two comments and a question:

1) Be aware that the “% of advertisers increasing spending” is actually “% of RENEWING advertisers increasing spending.” If you break down the distribution, it would appear that even the number of advertisers who are increasing and stable churns at 3-5k advertisers per quarter. Not to say it’s not a good metric, but it can be a little misleading. Certainly, the absolute number of accounts increasing spending has increased, although that increase has been decelerating.

Ironically, if you use the revenue breakdown they give to determine what % of the revenue base is increasing/stable, you actually get a declining number (because of the churn).

2) The key with this company is watching the client renewal and % online placement rate. Unfortunately, it appears the renewal rate is accelerating (not by much) and the % online placement rate is decelerating (not by much). The fear is that the low hanging digital fruits among the advertiser base have been picked and that online penetration will slow substantially.

3) Reasonable take on the major products. Do you have an opinion on the ‘digital services’ business that 6% of advertisers are subscribing to (SEO, SEM, website creation)? They appear distinctly overpriced and of seemingly little value.

Trying not to sound too negative. You’ll probably do well with this trade, and if it works out as hoped, substantially well. There’s just a lot of moving parts here and given the leverage, seemingly little room for error. It’s seductive to slap an 11% growth rate/20% decline rate on something and call it a day, but the numbers require much more nuance.

That should read “it appears the DECLINE in the renewal rate is accelerating (not by much)” if that wasn’t clear.

Thanks for each of the points, they are certainly valid.

With respect to SEO, SEM and websites, these don’t seem like great businesses to me either but I got the impression from the Q3 call that they are growing businesses. There was a discussion about margins on that call and in the discussion management said they were guiding to 40% margins in part because they are ahead of plan with SEO/SEM and those are low margin businesses. So not great about the low margins but good that they are doing well. I believe they said they were #1 in SEM and #3 in SEO in Canada on the Q1 call. With websites, I would like to know what kind of margins they are getting for the high-end websites and who their customers are now. Again on the Q1 CC they suggested they have some pretty large Canadian retailers like Futureshop and Best Buy in their mix (this is how I interpreted the comment anyways) and if they are running those kind of websites they might be doing ok with that business. They made a point of distinguishing that they were less interested in the smaller $100 or $250 websites and instead wanted the big ones.

More generally, I live in Canada, and in my opinion the thing they are missing is the marketing of their name. They need to get some commercials out on CTV, CBC, Global, get some billboards out downtown and engage people that Yellow Pages is back and its different and you should go to yellowpages.ca the next time you need something local. You see libraries doing that – explaining that you should check them out because they are more than just print books. Yellow Pages is a trusted brand name here in Canada, keep in mind there is and always has been one yellow pages in Canada, and its not like there is a competitor that is considered THE PLACE to go for local content on the web, I mean when I think of where I go to find consolidate Canadian local content I draw a blank out side of niche sites, like homestars.ca (which I think it would be a good thing for yellowpages to either buy or copy quickly because that is an extremely useful home reno site that I have used myself).

I agree that there are lots of moving parts and the projections I made could be off wildly in the long run. I admittedly find it difficult to wrap my head around how this business model plays out in the long run. You are right to be wary. But with the risk of sounding too opportunistic, I don’t think I need to see all the conclusions through to fruition to make a profit here. The stock is not covered by very many analysts (two I think?), the stock is hated by everyone who owned it prior to the restructuring, and the cash that the company should generate over the next few quarters should be substantial. When you add to that what appears to be an improving economy and a return of some animal spirits among investors willing to take risks, I think you have a set-up for a nice run. Pretty soon you get an article in the Globe or Post talking about the rise from the dead of phone books and you are off to the races.

The answer to the question I posed in the post (at what point will on-line compensate for print) is as important as a guide to perceptions as it is as a guide to the eventual reality. When investors begin to look at the stock again, and as analysts begin to cover it, they are going to want to see a promised land out there, some day in the future, when the on-line business is thriving and the print business declines have subsided. So I wanted to make sure that promised land was there and that it was appealing. Whether that day comes is anybody’s guess, I mean who knows what the world looks like in 2018, and like I said in the post and like you said in your comment, we just need to watch the numbers closely and see how they evolve. But I don’t believe I really need to answer the long run question to make money in this stock over the next 6-12 months. I just need to be ahead of the change in perceptions of others, which I think I am in this case.

what’s your take on this article? http://www.theglobeandmail.com/globe-investor/how-did-marc-tellier-last-this-long-at-yellow-media/article10235065/?cmpid=rss1

looks like nothing has changed at Yellow Media.

I read the article in addition to the premium one where they gave an investment opinion. I didn’t really learn much from either.

I’m not sure about comment nothing has changed? The CEO who has made some bad acquisition decisions has left and that is a major change. They also have a new board of directors, which is probably related to why Tellier is gone. Whether these changes are for the better we’ll have to see how things play out.

Right. I was referring to the fact that the board is still completely influenced by him and using every loophole to unjustly reward him. It’s like nothing has changed and I’m not sure if I’d want to invest alongside a board like that going forward.

I see. Fair enough. I guess I don’t see this as that big of a deal; it doesn’t influence my personal decision about the company as the valuation thesis I outlined in still intact. But I can understand how others might take a more principled stance.

There are some other businesses similar to Yellow Media that have uncertainty/terminal decline/headwinds facing them and are ripe for opportunities. For instance, have you looked at SPMD?

might you have recent information, and/or concerns about management’s apparent lack of common stock holdings? the annual report is indicating zero for all with the exception of a very small 1000 share plus holding by one director.

I don’t have concerns but its not something I have followed closely. Given the restructuring is only ~4 months old I wouldn’t expect a large share holding by anyone but the former creditors.

thank you – as you must know, Canaccord is saying ‘buy’, but difficult to imagine them recommending anything else. May I ask if you have a position in the warrants – and if not why?

but please do check what the warrants have done in comparison to the stock in the past couple of weeks…

I haven’t had time to investigate the warrants that thoroughly. Thoughts?

Perhaps best summarized on page 17:

Click to access Warrant%20Indenture%20(SEDAR%20Version).pdf

thanks

also a nice decision mapping chart here, this one applying to the purchase of MannKind stock/ warrants: http://seekingalpha.com/article/1070101-3-ways-to-trade-mannkind-given-2013-will-be-a-huge-success-or-a-complete-failure